Dividend Powerhouses 3% Plus Yield Three Stocks With Hidden Strengths

Paychex, Inc. PAYX | 0.00 |

With central banks tightening policy, energy markets swinging and inflation pressures still in focus, many investors are looking for portfolio anchors that can provide income while keeping risk in check. That is where high quality dividend stocks with 3%+ yields and reliable payout histories can help. The Dividend Powerhouses (3%+ Yield) screener focuses on companies offering more than a 5% yield that is covered by earnings, growing and relatively stable, which can be appealing when bond yields and rate expectations are moving around. Below, three stocks from this screener will be highlighted and broken down in plain English.

Intesa Sanpaolo (BIT:ISP)

Overview: Intesa Sanpaolo is one of Italy’s largest banking groups, providing everyday banking, corporate lending, investment banking, insurance, asset management and private banking services across Italy and parts of Europe, the Middle East and North Africa. It serves a wide range of clients from retail customers and small businesses to large corporates, public institutions and high net worth individuals.

Operations: Intesa Sanpaolo generates most of its revenue from its Territorial Bank segment at about €10.9b, followed by IMI Corporate & Investment Banking at about €4.8b and International Banks at about €3.2b, with additional contributions from Private Banking (€3.5b), Insurance (€1.8b), Asset Management (€1.1b) and Corporate Centre (€0.7b).

Market Cap: €106.6b

For dividend focused investors, Intesa Sanpaolo stands out as a large, diversified bank that is leaning into fee rich areas such as wealth management, insurance and digital services while maintaining high net profit margins around 36.8%. The story is not without risks, including heavy exposure to the Italian economy, rising fintech competition and tighter regulation, and its dividend track record is described as unstable, so payout reliability deserves attention. At the same time, experienced governance, strong capital generation and analyst expectations for earnings and cash flows are among the factors some investors consider when evaluating whether Intesa Sanpaolo could remain a meaningful income and total return candidate within a dividend portfolio, especially for those who understand the trade off between its strengths and these structural risks.

Intesa Sanpaolo’s high margins and push into fee rich businesses can look compelling, but the headline yield only tells part of the story. Before you lean on it as a core income anchor, review the 4 key rewards and 2 important warning signs

Paychex (PAYX)

Overview: Paychex provides payroll, HR, benefits and insurance services that help small and mid sized businesses handle everything from paying staff and filing payroll taxes to managing retirement plans and health coverage. The company’s platform aims to simplify compliance and people management so business owners can focus more on running and growing their operations.

Operations: Paychex generates its revenue primarily from Staffing & Outsourcing Services, which contribute about US$6.3b.

Market Cap: US$35.0b

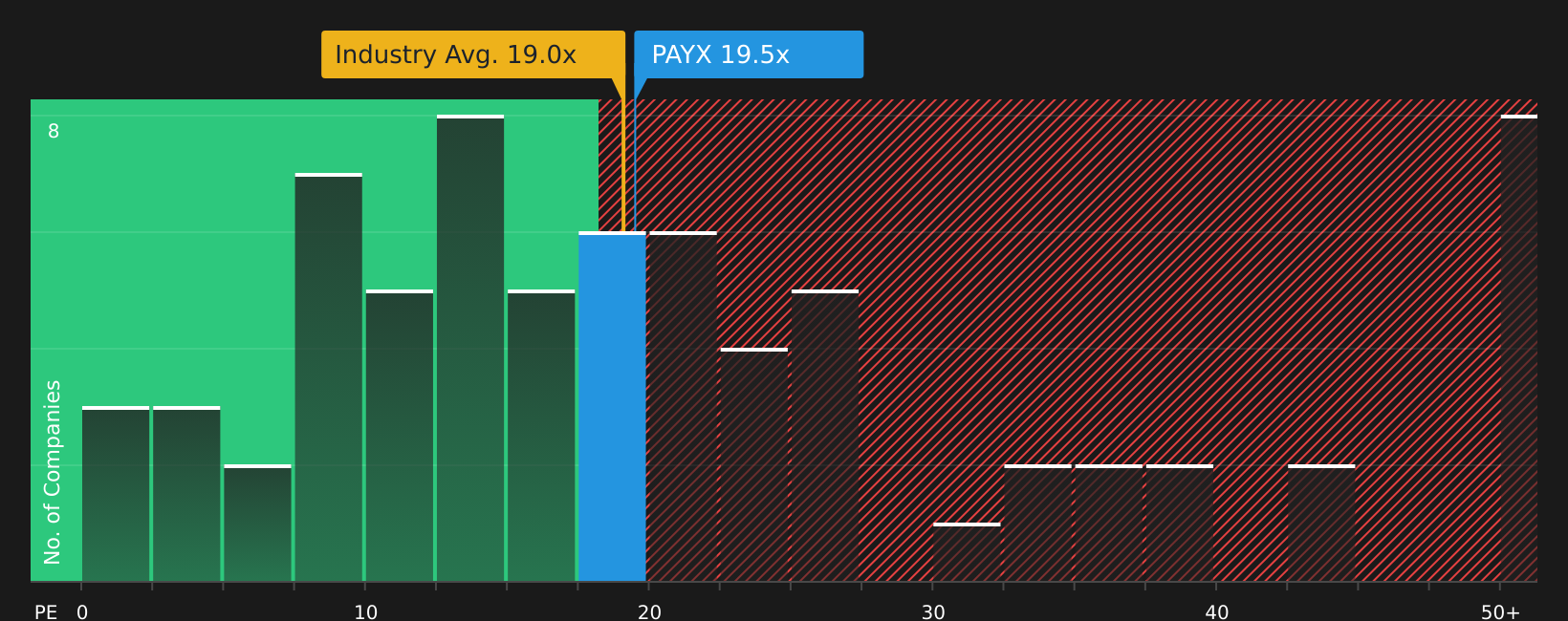

Investors looking at dividend income and recurring cash flows may find Paychex interesting because it combines human capital management services with AI tools like its HR Copilot and WISE AI platform, plus the pending Paycor acquisition that could widen its customer base and create cost synergies. At the same time, the stock carries real trade offs, including high debt, a dividend that is not fully covered by earnings and pressure on margins, even though net profit margins are currently around 25.8%. If you want to understand how the 4.4% yield, valuation signals and the Paycor integration risk all fit together, there is more to unpack in the detailed breakdown that follows.

Paychex’s 4.4% yield, AI tools and the Paycor deal hint at a story where income and growth could be pulling in different directions, and the full picture only comes into focus in the analysis report for Paychex

Global Ship Lease (GSL)

Overview: Global Ship Lease, Inc. owns a fleet of mid sized and smaller containerships and charters them out on fixed rate contracts to major container shipping companies worldwide. This gives it exposure to global trade volumes through contracted shipping capacity rather than operating its own liner services.

Operations: Global Ship Lease generates about US$757.0m in revenue from transportation and shipping activities.

Market Cap: US$1.4b

Global Ship Lease stands out for dividend investors because it combines long term, fixed rate charters with a focused fleet of mid sized and smaller ships, which currently benefit from tight supply and a sizeable contracted revenue backlog of about US$1.73b with 100% cover for 2026 and around 86% for 2027. That revenue visibility, high margins and a Ba2/BB+ credit profile are set against real risks, including expected declines in earnings and revenue, potential pressure on charter rates if trade routes normalize, heavy capital commitments for its US$917m newbuild program and an unstable dividend track record. If you want to understand whether Global Ship Lease’s low P/E, capital returns and fleet renewal justify those trade offs, the full story goes further than headline yield and backlog alone.

Global Ship Lease’s contracted backlog and fleet renewal create a story that looks more resilient than its headline yield suggests, and the real tension between income, P/E and future charter risk shows up in the 4 key rewards and 3 important warning signs (1 is major!).

The three dividend stocks covered here are just a starting point, and the full Dividend Powerhouses screen on Simply Wall St currently flags 1,911 more companies with income profiles and narratives that can be just as compelling as the ones outlined above through the Dividend Powerhouses (3%+ Yield) screener. Use Simply Wall St to identify and analyze the specific catalysts, dividend safety checks and business stories that matter most to you so you can focus on the highest conviction opportunities for your own watchlist and portfolio.

Take Control of Your Investment Journey

If Paychex or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh ideas move first, and the strongest breakouts, quiet momentum shifts and stocks flying under the radar for now can get caught quickly. Review these curated lists and consider your options in a timely way.

- Spot resilient operators with room to breathe by scanning a curated list of solid balance sheet and fundamentals (414 results) that can help you avoid stretched balance sheets while it still matters.

- Track accelerating themes in automation and AI by following companies in the hand picked 31 robotics and automation stocks before short-term momentum becomes more widely noticed.

- Monitor long term infrastructure themes by reviewing the focused 34 power grid technology and infrastructure stocks while these stories are still dropping in under most investors’ radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.