Do Atlantic Union Bankshares' (AUB) Richer Dividends Hint at Strength or Limited Reinvestment Ambition?

Atlantic Union Bankshares Corporation AUB | 0.00 |

- Recent coverage has highlighted Atlantic Union Bankshares as an appealing dividend stock, citing a yield above its industry average, a record of multiple dividend increases over the past five years, and expectations for higher earnings in the coming fiscal year.

- An additional point drawing investor attention is the company’s favorable Zacks Rank of #2 (Buy), which aligns with its income-focused profile and reinforces perceptions of resilience in its shareholder return policy.

- We’ll now examine how Atlantic Union Bankshares’ stronger income appeal, underscored by its above-industry dividend yield, influences the existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 50 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Atlantic Union Bankshares Investment Narrative Recap

To own Atlantic Union Bankshares, you need to be comfortable with a Mid Atlantic focused bank that leans into traditional lending and steady shareholder returns. The latest dividend focused coverage and favorable Zacks Rank support the near term income story, but do not materially change the key catalyst, which remains management’s ability to grow earnings while managing credit quality. The biggest risk still lies in its geographic concentration and exposure to localized economic slowdowns.

The most relevant recent announcement in this context is the board’s authorization of up to US$250,000,000 in share repurchases through May 2027, which sits alongside a history of regular dividend affirmations and increases. Together, these capital return actions reinforce the income narrative highlighted by the news, while also increasing the importance of Atlantic Union’s execution on earnings guidance and integration of recent acquisitions to support both the dividend and buybacks over time.

Yet investors should also be aware that a concentrated Mid Atlantic footprint could leave results vulnerable if...

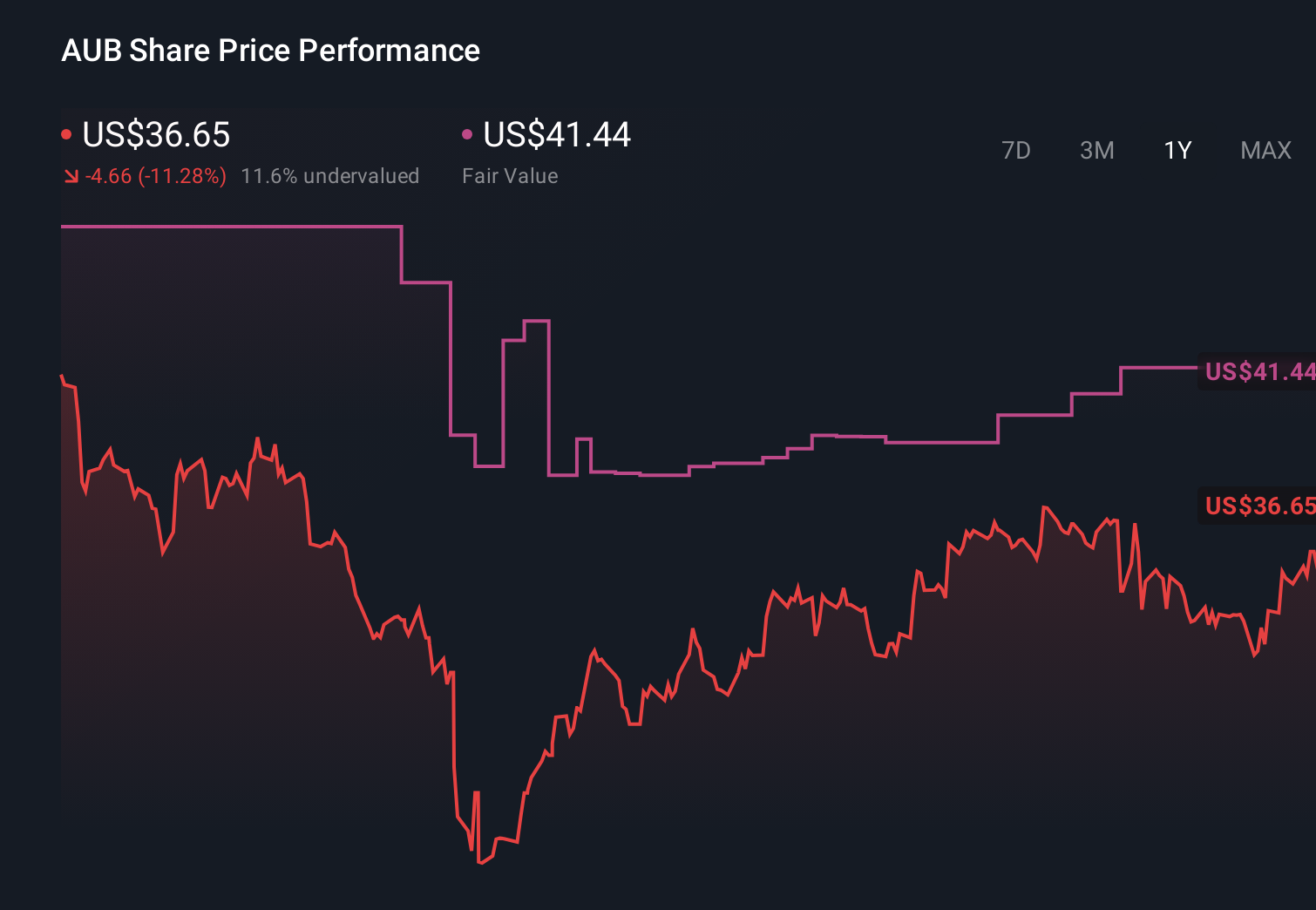

Atlantic Union Bankshares’ narrative projects $1.8 billion revenue and $709.8 million earnings by 2029.

Uncover how Atlantic Union Bankshares' forecasts yield a $44.25 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community value Atlantic Union Bankshares between US$30.79 and US$59.94, reflecting a wide spread in expectations. Against this backdrop, the bank’s reliance on traditional banking in the face of fintech competition is a key factor that could influence how those differing views on its long term performance ultimately play out.

Explore 4 other fair value estimates on Atlantic Union Bankshares - why the stock might be worth as much as 44% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Atlantic Union Bankshares research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Atlantic Union Bankshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Atlantic Union Bankshares' overall financial health at a glance.

No Opportunity In Atlantic Union Bankshares?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 43 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.