Do Upbeat Analyst Revisions Signal A Shift In PDF Solutions (PDFS) Risk Reward Profile?

PDF Solutions, Inc. PDFS | 0.00 |

- Recently, analyst commentary highlighted PDF Solutions as a strong momentum stock, citing its favorable Zacks Rank and upward earnings estimate revisions as key drivers of investor interest.

- This momentum focus underscores how changes in analyst expectations alone can materially influence sentiment toward a specialized semiconductor software and analytics provider like PDF Solutions.

- We’ll now examine how this fresh momentum, anchored in rising earnings estimates, reshapes PDF Solutions’ existing investment narrative and risk profile.

AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

PDF Solutions Investment Narrative Recap

To own PDF Solutions, you need to believe in its role as a specialized data and analytics provider to increasingly complex semiconductor manufacturing, and in its ability to grow recurring, software-like revenue without eroding margins. The recent momentum-driven analyst upgrades largely reinforce, rather than redefine, the main near term catalyst, which is execution against its growth and SaaS transition targets, while the most immediate risk remains revenue and earnings volatility from customer concentration and geopolitical exposure.

Against this backdrop, the May 2026 follow-on equity offering, which raised about US$201.0 million, is especially relevant. It strengthens PDF Solutions’ balance sheet and complements the expanded US$75 million revolving credit facility, giving the company more flexibility to fund product investment and potential expansion tied to its analytics platforms, even as investors weigh how this added capital and higher share count interact with the current momentum story and existing execution and concentration risks.

Yet while momentum is strong, the growing risk that key customers could internalize analytics or shift to proprietary AI tools is something investors should be aware of...

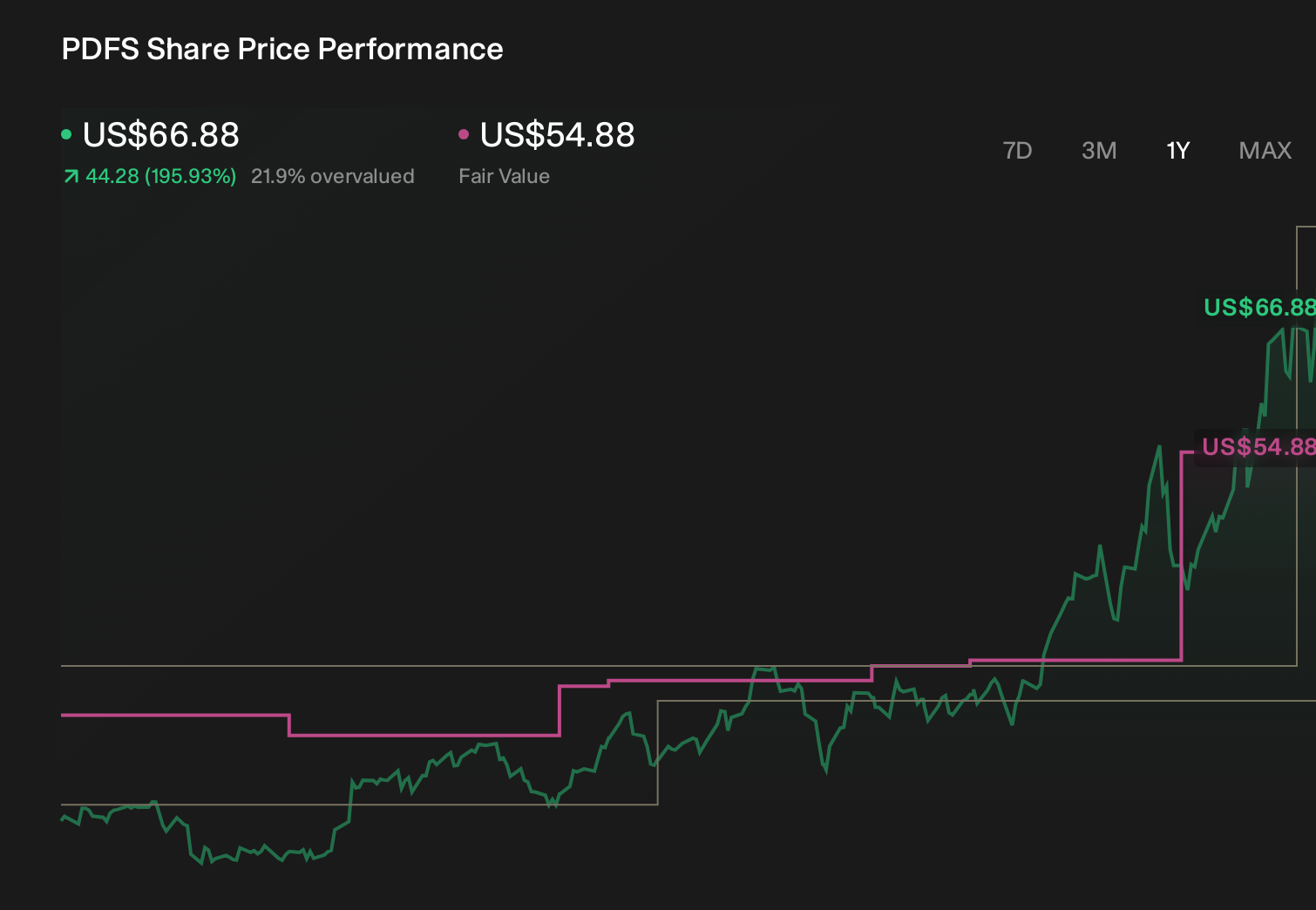

PDF Solutions’ narrative projects $383.7 million revenue and $81.7 million earnings by 2029. This requires 18.4% yearly revenue growth and about a $74.5 million earnings increase from $7.2 million today.

Uncover how PDF Solutions' forecasts yield a $54.50 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts told a very different story, assuming revenue of about US$378.5 million and earnings near US$50.8 million by 2029, which shows how far expectations can diverge as you weigh this new momentum news against concerns like rising data privacy and sovereignty constraints.

Explore 5 other fair value estimates on PDF Solutions - why the stock might be worth as much as 12% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your PDF Solutions research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free PDF Solutions research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PDF Solutions' overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.