Does FTAI Aviation’s (FTAI) Engine Repurposing Push Complicate Its Core Aviation Profit Story?

FTAI Aviation Ltd. FTAI | 0.00 |

- In recent days, Artisan Partners’ Artisan Small Cap Fund began exiting its position in FTAI Aviation, citing concerns that the company’s valuation embeds optimistic assumptions about its longer-term opportunities, including the FTAI Power initiative.

- The fund highlighted that FTAI’s effort to repurpose aircraft engines for data center power generation could be a volatile and non-linear profit driver, adding uncertainty to the company’s evolving business mix.

- Next, we’ll examine how Artisan’s valuation concerns and questions around FTAI Power’s profit path may influence FTAI Aviation’s broader investment narrative.

The latest GPUs need a type of rare earth metal called Terbium and there are only 27 companies in the world exploring or producing it. Find the list for free.

FTAI Aviation Investment Narrative Recap

To own FTAI Aviation, you need to believe its core jet engine maintenance and exchange business can keep generating attractive profits, while newer efforts like FTAI Power add optional upside. Artisan Small Cap Fund’s exit on valuation grounds raises questions about how much of that optionality is already priced in, but it does not directly change the near term focus on execution in the core MRE business or the key risk around concentration in legacy engine platforms.

One recent announcement that matters here is FTAI’s expanded revolving credit facility to US$2,025,000,000, with maturity extended to April 2031. This additional financing capacity gives the company more flexibility to invest in engine acquisitions, MRO capabilities, and potentially FTAI Power, which could reinforce near term catalysts around scaling its engine programs while also amplifying execution and capital allocation risks if newer initiatives prove more volatile than expected.

But while the growth story sounds compelling, the concentration risk around legacy engines and evolving power projects is something investors should be aware of...

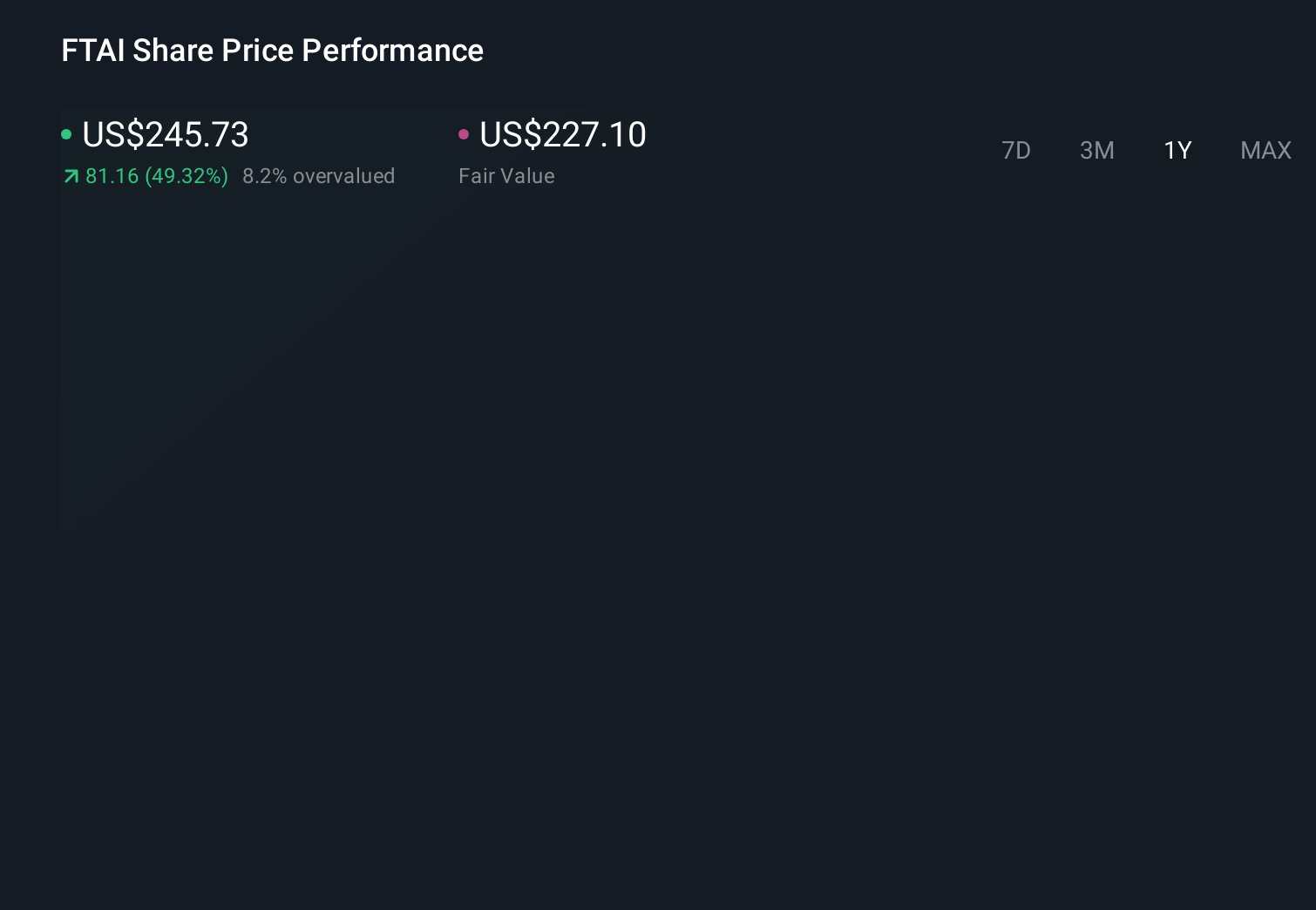

FTAI Aviation's narrative projects $6.6 billion revenue and $1.7 billion earnings by 2029.

Uncover how FTAI Aviation's forecasts yield a $350.60 fair value, a 50% upside to its current price.

Exploring Other Perspectives

The most cautious analysts were already projecting big numbers for FTAI, with revenue near US$4.6 billion and earnings around US$1.3 billion by 2029, yet they still highlighted aggressive expansion and integration risks as reasons for a far more pessimistic narrative than consensus. With Artisan’s valuation concerns now in focus, it is worth asking whether those lower end forecasts might shift further and considering how your own expectations compare with these very different views.

Explore 4 other fair value estimates on FTAI Aviation - why the stock might be worth just $299.10!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your FTAI Aviation research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free FTAI Aviation research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FTAI Aviation's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.