Does Insider Selling and ARK’s Exit Reshape the Bull Case for Iridium Communications (IRDM)?

Iridium Communications Inc. IRDM | 0.00 |

- In recent days, Iridium Communications has come under pressure as insider share sales and ARK Investment Management’s sizeable divestment heightened concerns about its valuation and the implications of its planned Aireon stake acquisition financing.

- This combination of insider selling, institutional repositioning, and added balance sheet risk from the Aireon deal is prompting investors to reassess how resilient Iridium’s long-term growth and capital return ambitions really are.

- We’ll now examine how insider selling and ARK’s exit interact with Iridium’s existing investment thesis and risk profile for investors.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Iridium Communications Investment Narrative Recap

To own Iridium, you have to believe its niche satellite network, IoT, and PNT services can keep generating attractive cash flows despite slower service revenue guidance and mounting competition. The recent insider sales, ARK’s divestment, and concerns around Aireon financing mainly sharpen the focus on valuation and balance sheet flexibility rather than changing the core thesis. Near term, the biggest swing factor is how smoothly Iridium executes the Aireon deal while managing leverage and protecting its dividend and buyback capacity.

The most relevant recent announcement here is Iridium’s plan to acquire the remaining Aireon stake for US$366.7 million, partly through a one year zero interest loan secured by Aireon equity. This structure adds debt and integration risk at a time when investors are already questioning how much upside is left in the stock after a strong run. How well Iridium absorbs Aireon, while keeping service revenue growth and capital returns on track, now sits at the heart of the catalyst debate.

Yet beneath the excitement over Aireon, a less obvious risk that investors should be aware of is how uneven PNT adoption could interact with...

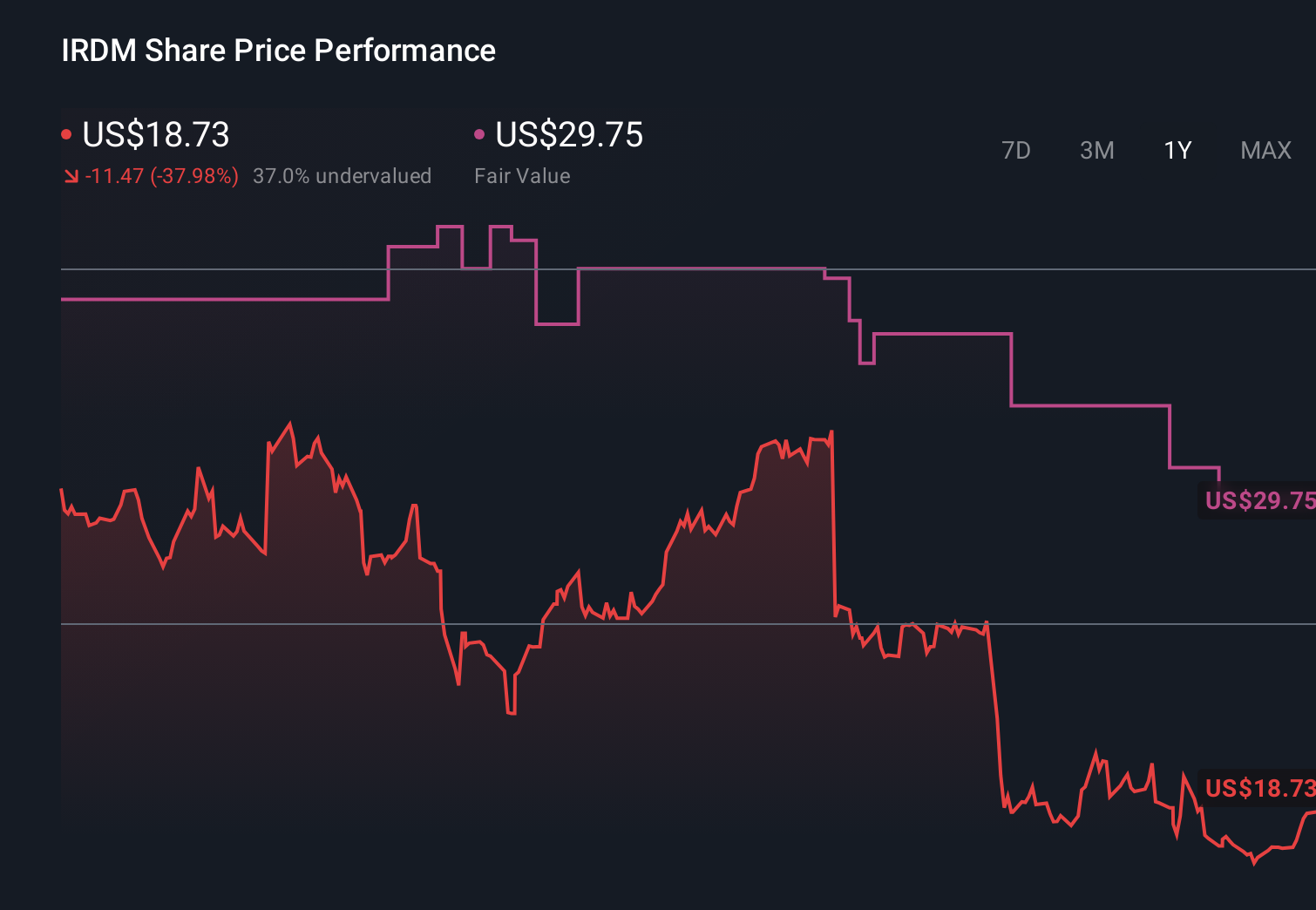

Iridium Communications' narrative projects $931.3 million revenue and $189.9 million earnings by 2029. This requires 2.2% yearly revenue growth and about a $75.5 million earnings increase from $114.4 million today.

Uncover how Iridium Communications' forecasts yield a $30.38 fair value, a 36% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts once projected Iridium earning about US$211.2 million by 2029, yet today’s concerns over Aireon financing and competitive pressure show how quickly that upbeat story could be challenged or reshaped.

Explore 8 other fair value estimates on Iridium Communications - why the stock might be worth less than half the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Iridium Communications research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Iridium Communications research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Iridium Communications' overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.