Does MasTec’s Record Backlog And Raised 2026 Outlook Reshape The Bull Case For MTZ?

MasTec, Inc. MTZ | 0.00 |

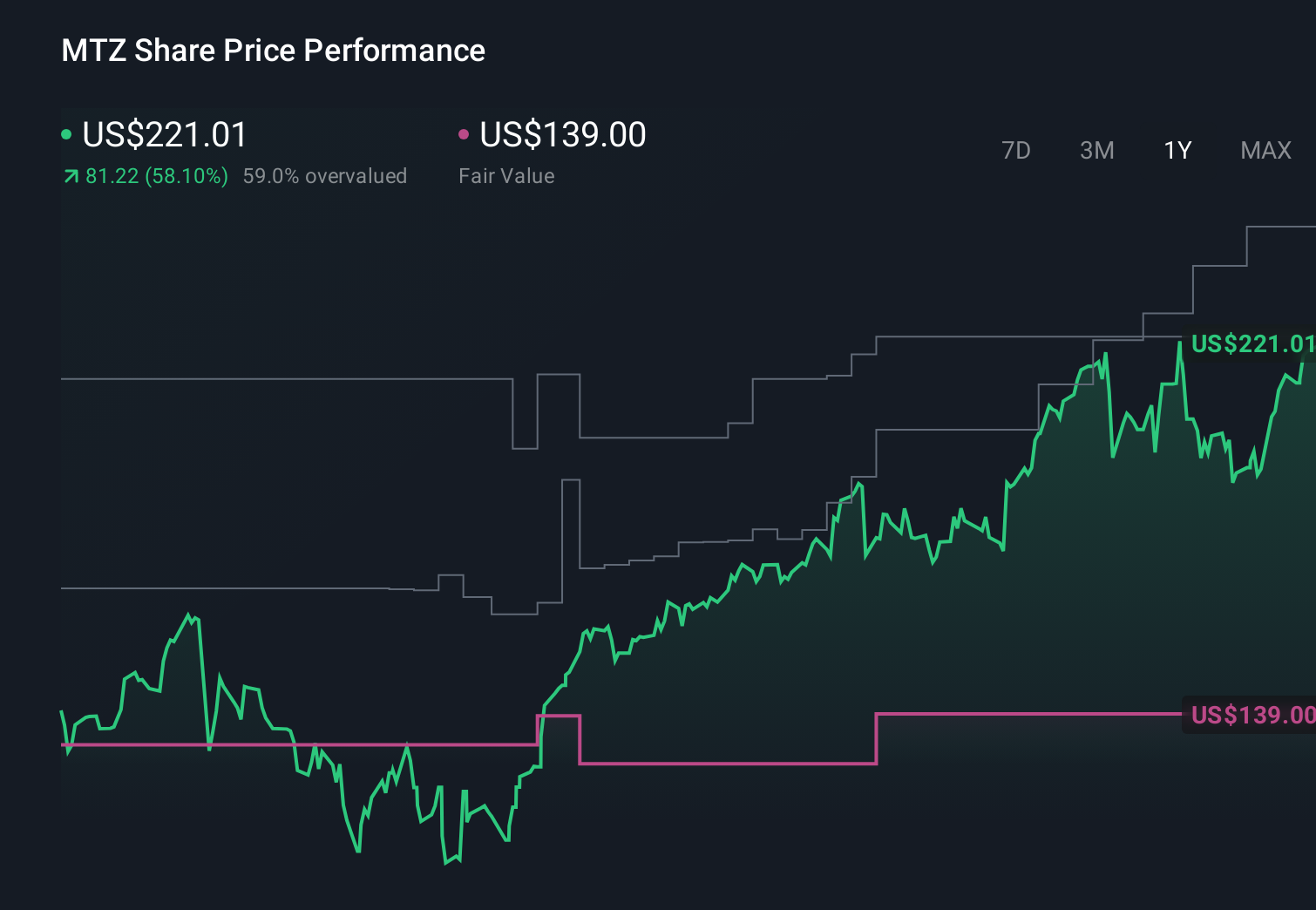

- MasTec recently reported its strongest-ever first quarter, with revenues up 34%, adjusted EPS rising very sharply year over year, and a record US$20.30 billion backlog that led management to raise full‑year 2026 guidance for revenue, adjusted EBITDA, and EPS.

- Beyond the headline growth, the company’s 1.4x book‑to‑bill ratio and 28% year‑over‑year increase in its 18‑month backlog underline broad-based, longer‑term demand across Clean Energy, Infrastructure, and Pipeline projects.

- We’ll now examine how MasTec’s raised 2026 guidance and expanding backlog could influence the company’s previously outlined investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

MasTec Investment Narrative Recap

To own MasTec, you have to believe its record US$20.30 billion backlog will convert into profitable work without major execution or customer‑driven surprises. The big near term catalyst is how effectively MasTec can translate its expanded 18‑month backlog into higher margins. The most important risk is that cost overruns, delays, or project cancellations could turn that backlog into lower than expected earnings. The latest results make this backlog story more credible, but they do not remove that execution risk.

Among recent announcements, the raised 2026 guidance to US$17.50 billion in revenue and US$6.77 in GAAP diluted EPS stands out as most relevant. It ties directly to the strong Q1 performance and backlog growth, reinforcing the idea that MasTec’s multi year build out in Clean Energy, Infrastructure, and Pipeline is starting to show through in earnings. At the same time, it raises the bar for future delivery at a moment when project timing and labor availability still matter a lot.

Yet against this strong quarter, investors should be aware of how sensitive MasTec’s thesis is to any slowdown or disruption in its largest projects...

MasTec's narrative projects $20.3 billion revenue and $880.9 million earnings by 2029.

Uncover how MasTec's forecasts yield a $348.72 fair value, a 9% downside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenue of about US$21.6 billion and earnings of roughly US$848.8 million by 2029, and worrying that project timing or policy shifts could make those targets hard to reach. This new backlog and guidance could prompt them to revisit those views, but it also highlights how widely opinions can differ, so you should look at several competing narratives before deciding how comfortable you are with MasTec’s risk and reward profile.

Explore 6 other fair value estimates on MasTec - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MasTec research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MasTec research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MasTec's overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.