Does Starboard’s Governance Push at Flowserve (FLS) Reveal a Deeper Shift in Capital Priorities?

Flowserve Corporation FLS | 0.00 |

- On May 28, 2026, Starboard Value LP disclosed a letter to Flowserve’s board criticizing execution, citing significant underperformance, and pledging to hold leadership accountable while engaging constructively.

- Alongside this pressure, Flowserve has recently streamlined its board, rejected a shareholder proposal on stock repurchases, affirmed its US$0.22 quarterly dividend, and seen a long‑serving director depart, signaling a period of intensified governance scrutiny.

- With Starboard’s activism now in focus, we’ll examine how this fresh governance pressure may reshape Flowserve’s investment narrative and execution priorities.

This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

Flowserve Investment Narrative Recap

To own Flowserve today, you need to believe that its core flow management business can convert industrial and energy demand into durable earnings, while improving execution in weaker segments like FCD. The Starboard Value letter heightens scrutiny on those execution gaps and near term project delivery, but it does not by itself change the key near term catalyst: Flowserve’s ability to turn its backlog into profitable growth. The biggest immediate risk remains uneven project timing and margin pressure on large engineered orders.

Among the recent announcements, the reduction of the board from eleven to nine directors stands out alongside Starboard’s involvement. A smaller board, coupled with the departure of an 18 year director and the arrival of a new member with financial expertise, could matter for how aggressively management tackles margin issues, capital allocation, and the integration challenges that have weighed on segment performance and short term earnings momentum.

Yet beneath the governance headlines, investors should be aware that project delays and tighter bidding could still...

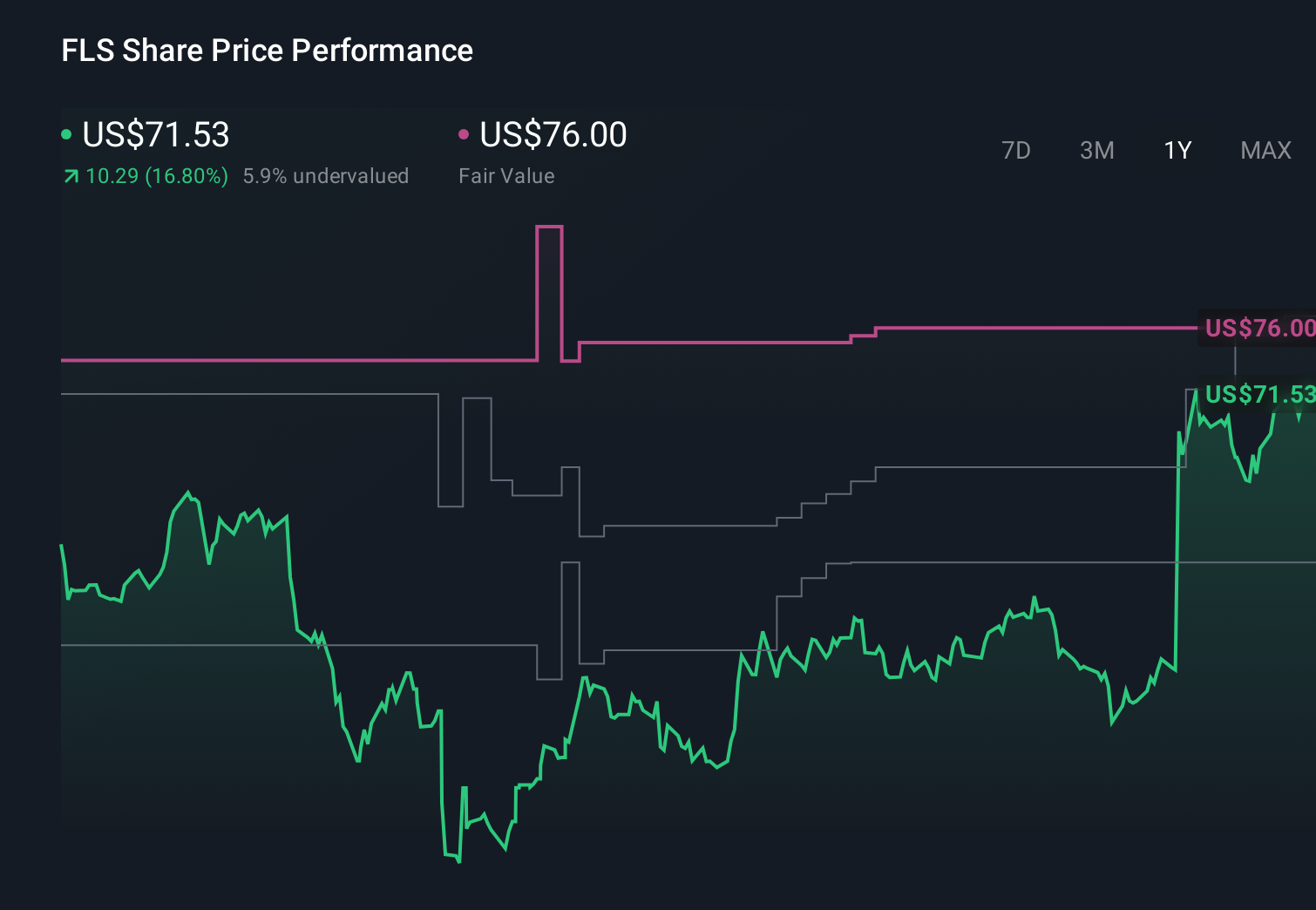

Flowserve's narrative projects $5.6 billion revenue and $660.0 million earnings by 2029. This requires 5.5% yearly revenue growth and about a $313.8 million earnings increase from $346.2 million today.

Uncover how Flowserve's forecasts yield a $94.80 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenue of about US$5.5 billion and earnings of roughly US$691 million by 2029, and their view of tariff and supply chain risks is much harsher, so this new activist pressure may push you to weigh those downside scenarios against more optimistic stories still in the market.

Explore 5 other fair value estimates on Flowserve - why the stock might be worth as much as 40% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Flowserve research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Flowserve research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flowserve's overall financial health at a glance.

No Opportunity In Flowserve?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.