Does StoneCo's (STNE) One-Time Dividend and New Directors Hint At A Shift In Capital Discipline?

StoneCo Ltd. STNE | 0.00 |

- StoneCo Ltd. previously announced that shareholders approved the election of Marcelo Kopel and Pedro Zinner as directors at the April 23, 2026 annual general meeting, and earlier authorized an extraordinary cash dividend of US$2.53 per share, or about ZAR 3.08 billions based on March 31 shares outstanding, payable on May 4, 2026.

- The combination of fresh board appointments and a one-time dividend return of excess capital highlights how StoneCo is actively reshaping its governance and capital allocation approach ahead of its mid-May earnings release.

- We’ll now examine how this extraordinary cash dividend decision may affect StoneCo’s existing investment narrative around capital returns and earnings quality.

Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

StoneCo Investment Narrative Recap

To own StoneCo, you need to believe in its ability to compound value from MSMB payments and financial services, while managing credit risk and competition. The extraordinary US$2.53 per share dividend looks more like a balance sheet event than a change to the near term earnings catalyst around the upcoming May results, or to the key risk that weaker TPV trends and higher provisions could pressure margins.

The extraordinary dividend announcement is the clearest recent signal for investors to weigh right now. Returning about ZAR 3.08 billion in cash comes on top of sizeable past buybacks, and puts capital returns at the center of the short term story around earnings quality, balance sheet resilience and how much room StoneCo has to keep investing while still rewarding shareholders.

Yet while capital returns look appealing today, investors should also be aware that...

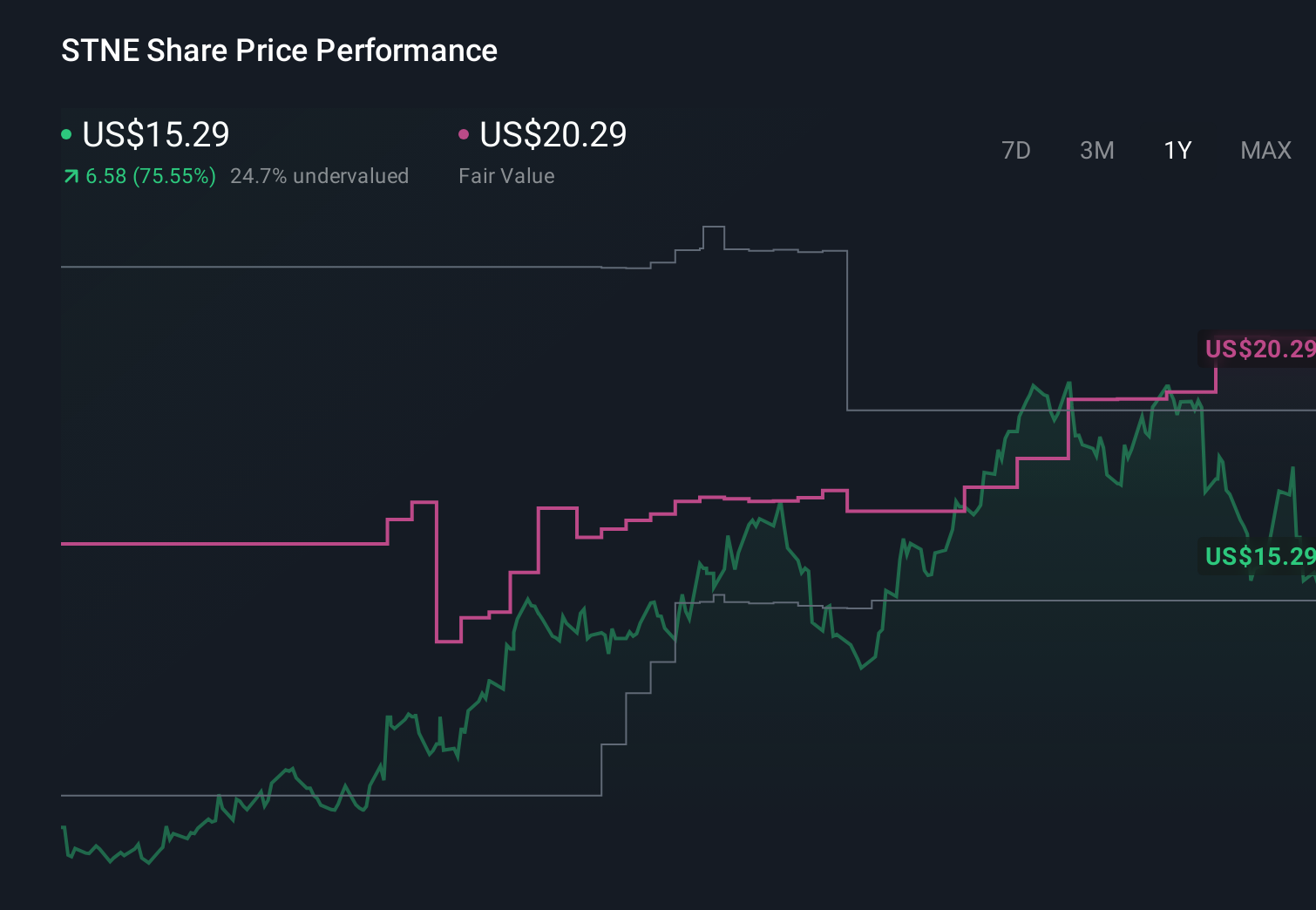

StoneCo's narrative projects R$17.4 billion revenue and R$5.0 billion earnings by 2028. This requires 8.2% yearly revenue growth and an earnings increase of about R$6.3 billion from R$-1.3 billion today.

Uncover how StoneCo's forecasts yield a $20.29 fair value, a 69% upside to its current price.

Exploring Other Perspectives

The most optimistic analysts were already modeling earnings of about R$5.4 billion by 2029, but if rising competition and PIX adoption bite harder than expected, that path could look very different, so it is worth comparing how your own view lines up with both the bullish and more cautious cases.

Explore 9 other fair value estimates on StoneCo - why the stock might be worth over 4x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your StoneCo research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free StoneCo research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate StoneCo's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.