Does Strong Q1 EPS Momentum Alter the Profit-Quality Bull Case For W. R. Berkley (WRB)?

W. R. Berkley Corporation WRB | 65.99 | +1.09% |

- In April 2026, W. R. Berkley reported its fiscal Q1 results, with analysts having anticipated earnings of US$1.14 per share, implying 12.9% year-on-year growth and building on a recent pattern of meeting or beating expectations in three of the last four quarters.

- This track record of earnings delivery, combined with analyst projections for continued EPS expansion in coming years, has become a key focus for investors watching how consistently the insurer can convert its specialty underwriting strength into profit growth.

- We’ll now examine how this anticipated double-digit Q1 earnings growth shapes W. R. Berkley’s investment narrative and earnings resilience.

This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

W. R. Berkley Investment Narrative Recap

To own W. R. Berkley, you generally need to believe its specialty focus and underwriting discipline can support steady earnings, even as competition and inflation test margins. The anticipated US$1.14 Q1 2026 EPS, up 12.9% year-on-year, reinforces the near term earnings resilience story, but does not fundamentally change the key short term catalyst, which is sustaining underwriting profitability, or the biggest risk, which remains pressure on pricing discipline in property and reinsurance.

Recent capital returns help frame this earnings outlook. The regular dividend, lifted in 2025 to an annualized US$0.36 per share plus a US$0.50 special payout, and the enlarged 25,000,000 share repurchase authorization, show W. R. Berkley returning cash while still funding growth. How effectively the company balances these cash outflows with reinvestment behind specialty lines and digital initiatives will be crucial if the expected Q1 earnings strength is to translate into longer term compounding.

But while earnings look resilient today, investors should also be aware that...

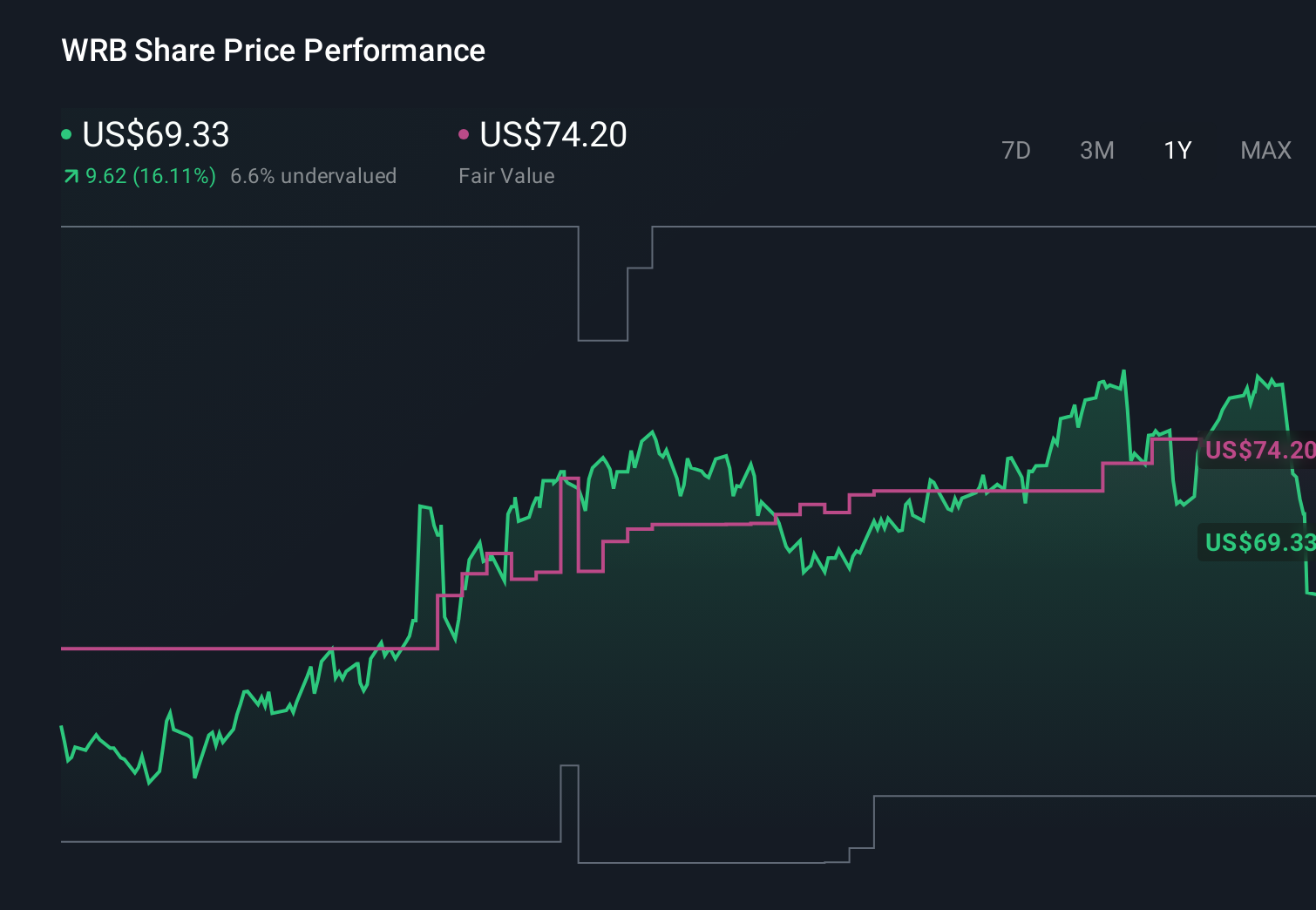

W. R. Berkley's narrative projects $14.3 billion revenue and $2.0 billion earnings by 2028. This is based on revenue remaining flat at a 0.0% yearly change and an earnings increase of about $0.2 billion from $1.8 billion today.

Uncover how W. R. Berkley's forecasts yield a $68.33 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Some analysts see more upside, expecting earnings of about US$2.3 billion by 2028, yet rising catastrophe losses and inflation could leave that optimism looking overstretched.

Explore 3 other fair value estimates on W. R. Berkley - why the stock might be worth as much as 95% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free W. R. Berkley research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. R. Berkley's overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 25 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.