Does Vulcan’s Shift Toward Aggregates and Key Corridors Reshape the Bull Case for VMC?

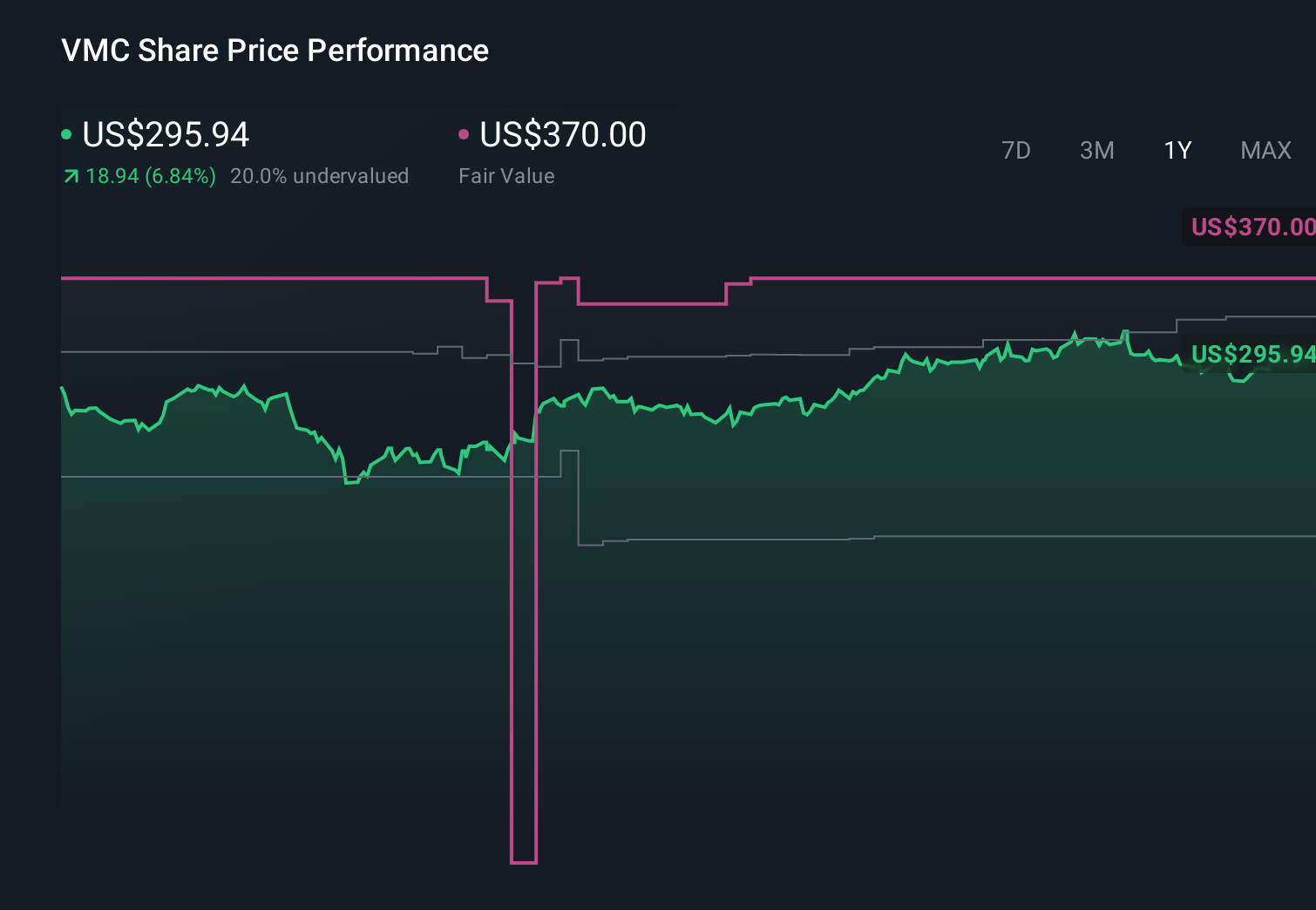

Vulcan Materials Company VMC | 0.00 |

- Vulcan Materials has completed the sale of its California ready-mixed concrete operations while acquiring Brannan Sand & Gravel’s southern Colorado and Dallas–Fort Worth assets, including a rail-linked aggregate quarry with long-term reserves and a new Texas distribution yard.

- This portfolio reshaping underscores Vulcan’s focus on an aggregates-led model, tightening its control over key reserves and distribution corridors rather than downstream concrete production.

- We’ll now examine how Vulcan’s shift toward aggregates and enhanced distribution through the Brannan acquisition may influence its broader investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

Vulcan Materials Investment Narrative Recap

To own Vulcan Materials, you need to believe in steady demand for construction aggregates and the company’s ability to turn that into consistent cash generation. The Brannan Sand & Gravel acquisition and California concrete exit reinforce an aggregates focused model, but do not materially change the near term reliance on public infrastructure funding as the key catalyst or the risk from weather and project delays in core Sunbelt markets.

Among recent developments, Vulcan’s Q1 2026 results stand out in this context. The company reported US$1,755.9 million in sales and US$165.5 million in net income, while continuing to invest in M&A and buybacks. The Brannan assets fit into that ongoing capital deployment story, potentially affecting how investors weigh the trade off between growth, execution risk and Vulcan’s already elevated earnings multiple.

But against that, investors should also be aware that...

Vulcan Materials' narrative projects $9.6 billion revenue and $1.7 billion earnings by 2029. This requires 6.0% yearly revenue growth and about a $0.6 billion earnings increase from $1.1 billion today.

Uncover how Vulcan Materials' forecasts yield a $328.81 fair value, a 21% upside to its current price.

Exploring Other Perspectives

The most pessimistic analysts were already assuming only 3.9 percent annual revenue growth to about US$9.0 billion, even before this deal, and they worry that stricter environmental rules could make the kind of rail linked quarry expansion Vulcan just bought meaningfully harder to repeat over time.

Explore 4 other fair value estimates on Vulcan Materials - why the stock might be worth 20% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vulcan Materials research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.