Does WRB’s Selective Underwriting Shift and Buybacks Strategy Change The Bull Case For W. R. Berkley?

W. R. Berkley Corporation WRB | 0.00 |

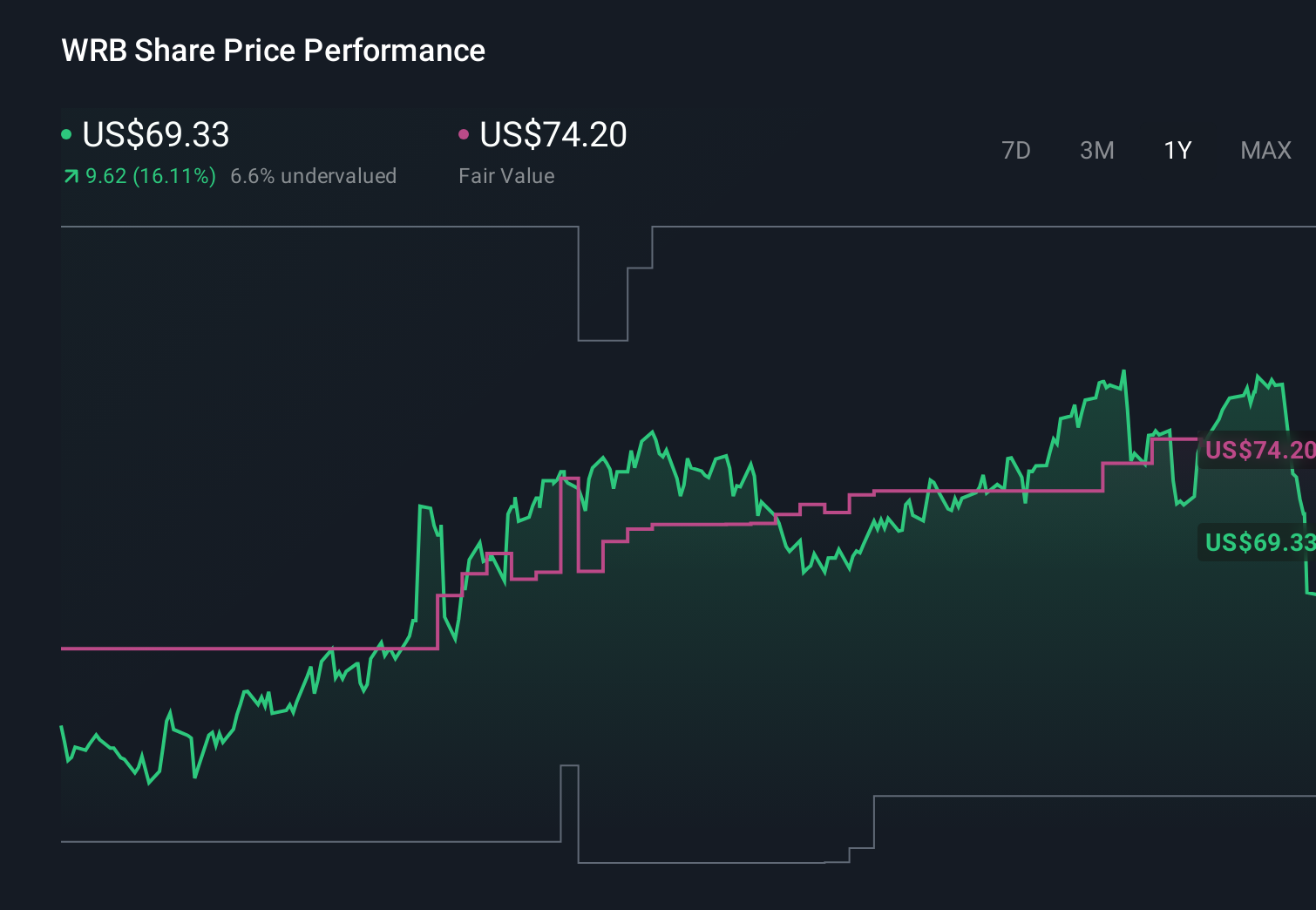

- W. R. Berkley’s first-quarter 2026 results showed revenue of US$3,690.33 million and net income of US$515.22 million, alongside continued buybacks and leadership changes in its oil, gas and environmental units.

- Beyond the headline growth in earnings per share, management’s emphasis on more selective underwriting and capital deployment signals a meaningful adjustment in how the insurer is approaching competition and risk.

- We’ll now explore how this shift toward selective underwriting and balanced growth could influence W. R. Berkley’s existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 18 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

W. R. Berkley Investment Narrative Recap

To own W. R. Berkley, you need to believe it can keep turning disciplined underwriting and investment income into solid, repeatable earnings while managing competition and catastrophe risk. The key short term catalyst is how well this new emphasis on selective growth holds up against rising competitive pressure, particularly from larger national carriers; the recent results and commentary support that focus, but do not materially change the biggest near term risk around potential pricing pressure and underwriting discipline in property and casualty lines.

The first quarter 2026 earnings update is the most relevant piece of recent news here, because it links the financial outcome (US$3,690.33 million of revenue and US$515.22 million of net income) directly to management’s messaging on underwriting selectivity and capital deployment. That combination matters for the current catalyst, as it shows how W. R. Berkley is trying to balance growth, profitability and ongoing capital returns such as buybacks within a more competitive market.

Yet behind the reassuring headline numbers, investors should be aware of growing competitive pressure and the risk that pricing discipline in key lines could...

W. R. Berkley's narrative projects $14.3 billion revenue and $2.0 billion earnings by 2028. This implies 0.0% yearly revenue growth and an earnings increase of about $0.2 billion from $1.8 billion today.

Uncover how W. R. Berkley's forecasts yield a $68.33 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling earnings of about US$2.3 billion by 2028, and Q1’s results could either support that view or expose how sensitive it is to rising catastrophe losses and competitive pressures in property and casualty lines.

Explore 3 other fair value estimates on W. R. Berkley - why the stock might be worth as much as 85% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free W. R. Berkley research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. R. Berkley's overall financial health at a glance.

Curious About Other Options?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 32 companies in the world exploring or producing it. Find the list for free.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.