DorianG (LPG) Stock Shows A Possible 20% Valuation Gap After Fleet Renewal Moves

Dorian LPG Ltd. LPG | 0.00 |

DorianG (NYSE:LPG) is drawing attention after agreeing to build a new 90,000 cbm very large gas carrier for about US$115 million, while planning to sell three older vessels for roughly US$256 million.

DorianG’s share price has slipped over the past month, with a 30 day share price return of down 13.9%. However, the year to date share price return of 61.6% and 1 year total shareholder return of 75.6% indicate momentum over a longer horizon, as investors weigh this newbuild order and planned vessel sales against changing expectations for earnings risk.

If this kind of fleet reshaping has your attention, it could be a good moment to broaden your view across the shipping space and check out 20 top founder-led companies

So with DorianG’s shares pulling back in the short term but still showing strong returns over the past year, is the current price underestimating the impact of fleet renewal, or is the market already factoring in future growth?

Most Popular Narrative: 20% Overvalued

The most followed valuation narrative currently pegs DorianG’s fair value at about $33.33, which sits below the last close of $39.99. This sets up a clear tension between modelled worth and market pricing.

The future P/E assumption has risen from about 24.27x to roughly 33.05x, which points to a higher multiple being used in the latest fair value work.

Want to see what kind of earnings path has to line up with that richer multiple and higher fair value range? The narrative relies heavily on specific growth, margin and re-rating assumptions that most investors never read past the headline.

Result: Fair Value of $33.33 (OVERVALUED)

However, that story can come under pressure if freight rates soften or if environmental and regulatory costs rise faster than DorianG can offset through operations and fleet renewal.

Another View: DorianG Through the Earnings Multiple Lens

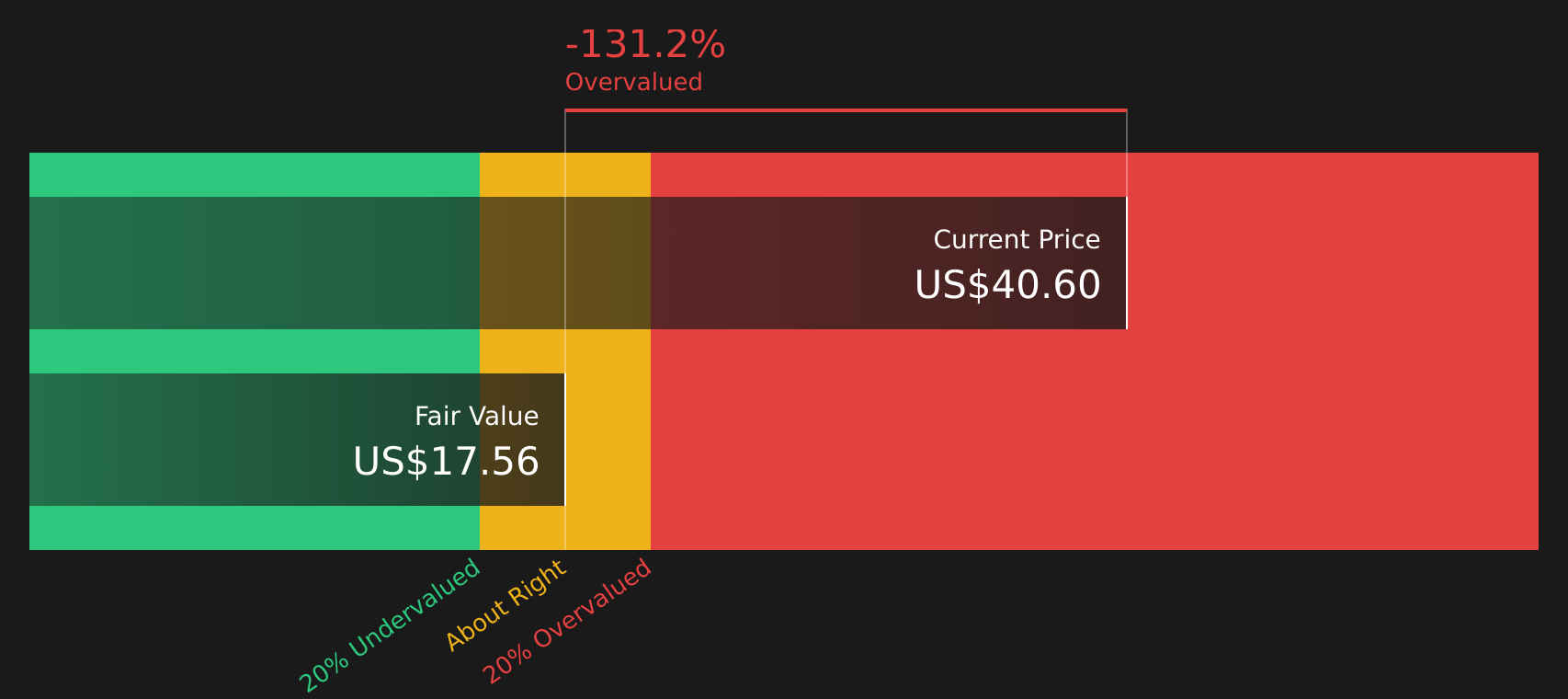

The SWS DCF model flags DorianG as expensive, with the current $39.99 share price sitting above an estimated future cash flow value of $17.56. That is a very different message from the popular 20% overvaluation narrative. Which signal do you trust when assessing risk versus potential upside?

Next Steps

With DorianG showing mixed valuation signals and sentiment divided between risks and rewards, move quickly to review both sides of the story through 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond DorianG?

If DorianG has sharpened your focus on valuation and risk, do not stop here. Use the Simply Wall Street Screener to uncover fresh opportunities that fit your approach.

- Target resilient payers by scanning companies offering strong income potential using the 7 dividend fortresses.

- Hunt for quality at a reasonable price by filtering stocks that combine value with robust fundamentals through the 44 high quality undervalued stocks.

- Spot under-the-radar opportunities before the crowd by running a focused search with the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.