Dorman Stock And 2 U.S. Manufacturing Picks for a Tariff Driven Supply Chain Shift

Dorman Products, Inc. DORM | 0.00 |

Potential U.S. tariffs on Canadian goods and tighter rules on forced labour are putting a spotlight on where companies source and build their products. For investors, that creates both risk and opportunity, as supply chains tied to Canada could face higher costs while more U.S. domestic manufacturing becomes relatively more attractive. This article looks at how that backdrop connects to three stocks from a U.S. Domestic Manufacturing Stocks screener that appear exposed to this news. You will see how each company might be positioned, and why some investors may see reasons to pay closer attention now.

ZJK Industrial (ZJK)

Overview: ZJK Industrial is a Shenzhen based manufacturer of precision fasteners and metal parts, supplying screws, bolts, CNC machined parts, SMT and PVD products used in sectors such as new energy vehicles, smartphones, wearables, drones and 5G equipment across China, the U.S. and other markets.

Operations: ZJK Industrial generates about US$56.1 million in revenue from metal fasteners and related products, with most sales coming from China (US$32.45 million), followed by Taiwan (US$16.48 million) and smaller contributions from Singapore, America and other regions.

Market Cap: US$124.1 million

Investors looking at U.S. focused manufacturing themes may find ZJK Industrial interesting because it combines exposure to end markets such as AI servers, industrial robotics and EVs with a relatively low P/E of 12.2x and an 18.2% net margin. Earnings growth has been very strong recently, and recent product launches in higher value fasteners for automated production lines indicate demand for more precise components. At the same time, volatility, high non cash earnings and an inexperienced board underline that this is not a low risk stock. With the company currently underperforming the broader U.S. market despite strong recent financials, the gap between its potential and its current share price story is what may catch investors' attention.

Strong recent earnings, an 18.2% net margin and a 12.2x P/E suggest ZJK Industrial might not be priced for its full story yet. The 4 key rewards and 2 important warning signs (1 is major!) could reveal what the current share price might be missing.

Dorman Products (DORM)

Overview: Dorman Products supplies replacement and upgrade auto parts for cars, trucks and specialty vehicles, selling everything from engine and undercar components to electronics and hardware through major aftermarket retailers, distributors and dealers in the U.S. and abroad.

Operations: Dorman Products generates about US$1.71b of revenue from Light Duty parts, US$238.7m from Heavy Duty and US$205.7m from Specialty Vehicle products, with roughly US$1.99b of total sales coming from the United States and US$160.5m from other markets.

Market Cap: US$4.17b

Dorman Products sits at the intersection of an aging U.S. vehicle fleet, recurring demand for essential replacement parts and a global trade system where tariffs can reshape cost and competitive pressures. The company’s focus on aftermarket parts that drivers need to keep vehicles on the road, plus a pipeline of higher margin proprietary parts, helps support earnings quality even as net margins and ROE are modest and last year’s earnings declined 11.3%. Recent debt refinancing and share buybacks suggest management is confident about cash flow, yet reliance on external borrowing and ongoing tariff uncertainty remain important watchpoints. With potential U.S. tariffs lifting the relative appeal of domestically focused suppliers, the key consideration is how much of that potential is already reflected in Dorman’s share price story.

Dorman Products appears to be a steady operator whose earnings dip, modest margins and recent refinancing may be masking something more interesting in its story. The analysis report for Dorman Products could show what the tariff and cash flow puzzle is really pointing to next.

TriMas (TRS)

Overview: TriMas is a U.S. based manufacturer that supplies dispensing and closure packaging, as well as steel gas cylinders, to consumer, industrial, aerospace and defense customers worldwide through brands such as Rieke, Rapak and Norris Cylinder.

Operations: TriMas generates most of its revenue from Packaging at about US$547.1 million, with Specialty Products contributing around US$114.4 million.

Market Cap: US$1.50b

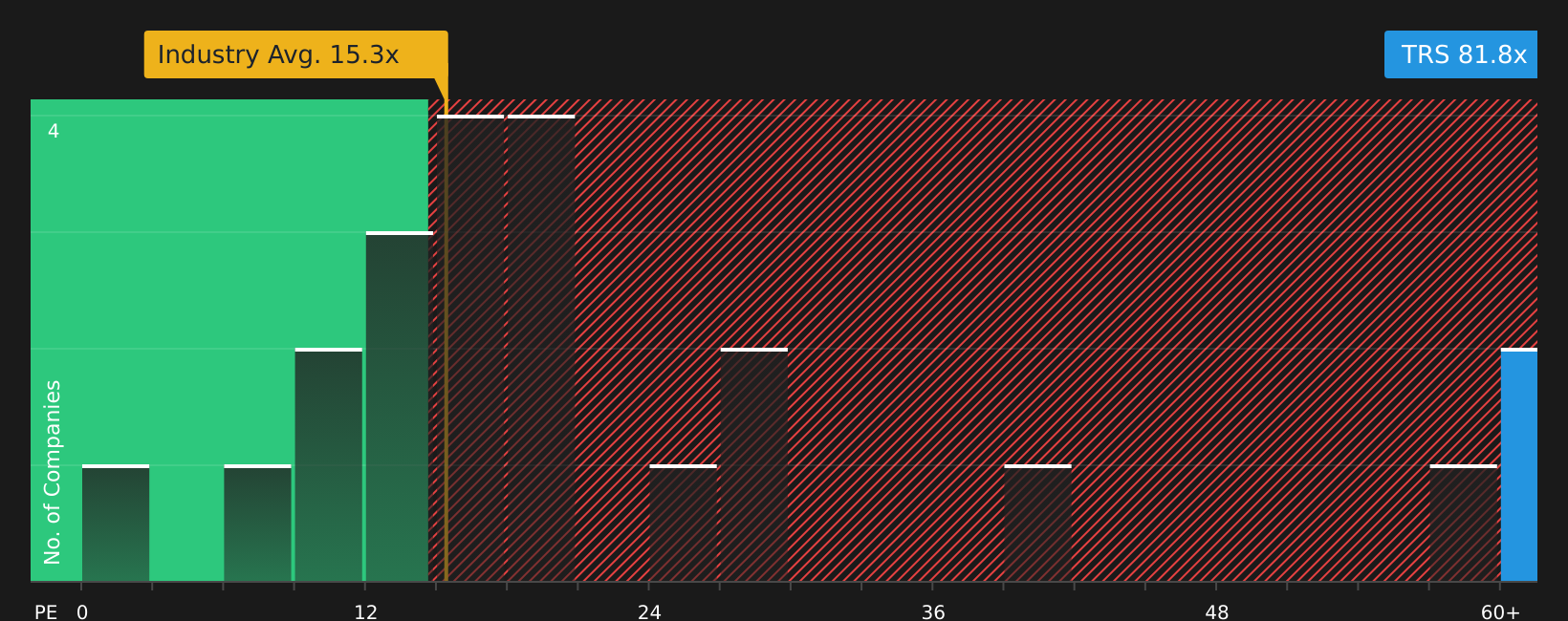

TriMas stands out in this U.S. Domestic Manufacturing Stocks screener because it links a largely U.S. oriented industrial footprint to packaging and gas cylinder products that are used across everyday consumer and industrial applications. This comes at a time when tariffs on imported goods and forced labour rules are pushing buyers to reassess where and how they source. The company is working on margin improvement through automation and integration of past acquisitions, is running an active buyback and dividend program, and management is already repositioning supply chains to limit tariff exposure. At the same time, a very high P/E, reliance on external borrowing and exposure to changing tariff policies and cyclical end markets mean investors need to look closely at what is driving the recent earnings jump and whether today’s valuation fully reflects the risks in the story.

TriMas’ high P/E, active buybacks and repositioned supply chains suggest that the current valuation story may be missing a key angle. The 3 key rewards and 2 important warning signs could surface the one risk reward twist that really matters next.

The three stocks in this article are just a starting point, and the full U.S. Domestic Manufacturing Stocks screener surfaces 32 more U.S. focused manufacturers that may have equally compelling stories tied to tariffs, supply chains and domestic production. Use Simply Wall St to identify and analyze the specific catalysts, financial traits and risk profiles that matter to you so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If Dorman Products or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh stock ideas can gain momentum quickly, and the best entry points often get caught by early movers. Tap into under the radar opportunities before the crowd and act now.

- Spot potential early breakouts in smaller companies with solid balance sheets by scanning the curated 18 high quality undiscovered gems while they are still flying under most investors’ radars.

- Position ahead of possible shifts in energy and infrastructure by tracking curated 89 nuclear energy infrastructure stocks that could move as sentiment changes, while the best entries are still on offer.

- Ride long term compounding income by reviewing a hand picked 9 dividend fortresses list that focuses on consistency and resilience before yields start dropping toward the crowd’s favorites.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.