Duolingo (DUOL) Moves Into Value Indexes As Its Valuation Debate Heats Up

Duolingo, Inc. DUOL | 0.00 |

Duolingo (DUOL) has been reclassified across several Russell indexes, moving out of multiple growth benchmarks and into a group of value indexes, including the Russell 1000 Value and Russell 3000 Value.

Recent trading suggests momentum in Duolingo is rebuilding, with a 1 day share price return of 3.15% and a 90 day share price return of 34.72%. This is occurring even though the year to date share price return is down 26.50% and the 1 year total shareholder return is down 67.28%. This backdrop helps explain why some investors may now be reassessing the stock as it shifts into value oriented indexes.

If Duolingo’s reclassification has you rethinking your watchlist, this could be a good moment to broaden your view with resilient digital and tech driven education peers using the 20 top founder-led companies

After Duolingo’s sharp reset, recent gains and a shift into value indexes put the spotlight on one issue: does the balance of risk and potential reward still lean toward buyers at today’s price?

Most Popular Narrative: 13.3% Overvalued

Against Duolingo's last close at $129.72, the most followed narrative anchors fair value at $114.49, framing today’s price as meaningfully above that mark.

Duolingo just crossed $1 billion in revenue and delivered a 367% surge in net earnings, yet the stock trades at a trailing P/E of just 11x. For a market-leading EdTech platform with 50 million daily active users, that’s a number you’d normally associate with a slow-moving industrial company, not one of the most recognisable consumer brands on the planet.

Want to see what kind of revenue path and profit margins sit behind that fair value line, and how they tie into future earnings multiples? The full narrative lays out the growth, the cash generation, and the assumptions that pull that $114.49 figure together in a way the share price alone does not.

Result: Fair Value of $114.49 (OVERVALUED)

However, Duolingo’s Vision 2026 spending plans and increasing AI competition could compress margins or slow user growth, putting pressure on both earnings expectations and today’s valuation story.

Another View on Duolingo’s Value

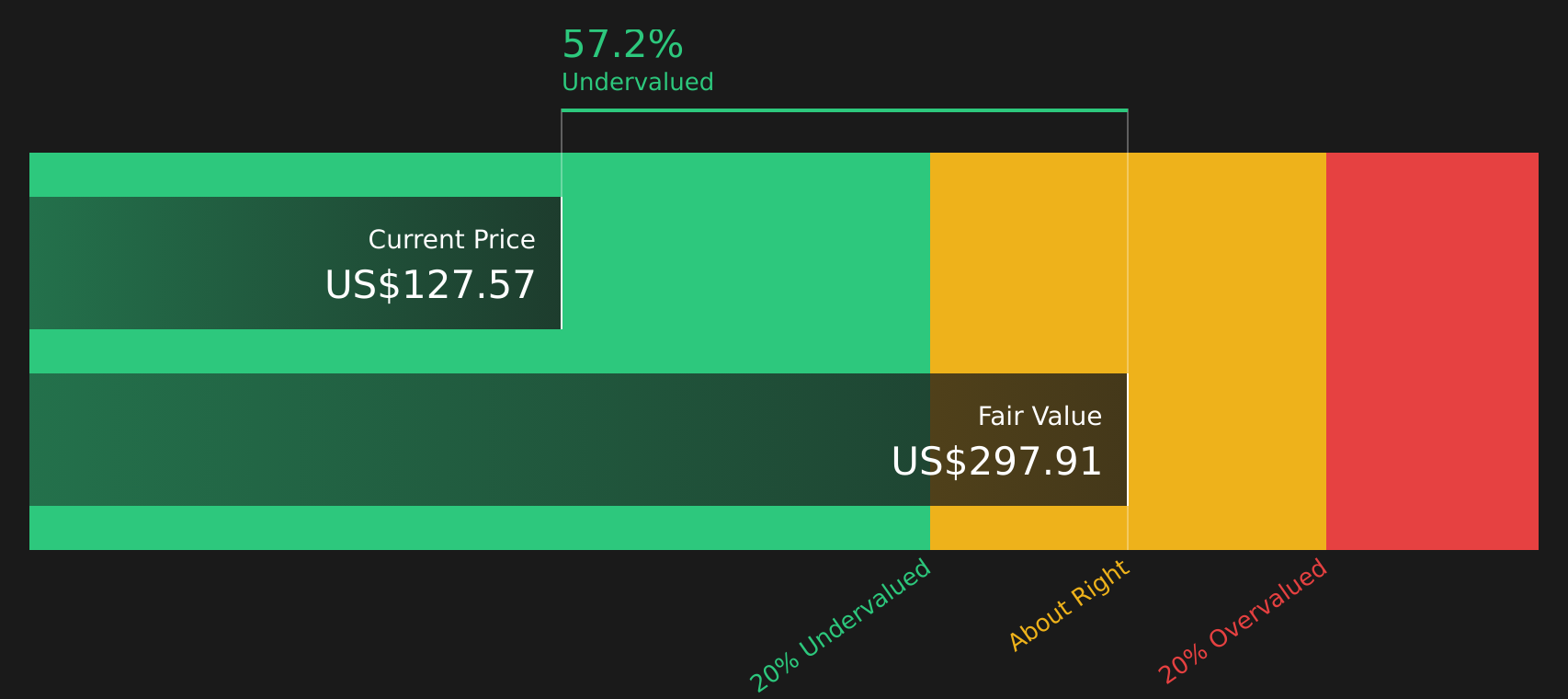

The user narrative frames Duolingo as 13.3% overvalued at $129.72 versus a $114.49 fair value. Our DCF model points in the opposite direction, with Duolingo trading at $129.72 compared with an estimated future cash flow value of $295.27, which suggests the stock is materially undervalued. Which story do you think better fits how Duolingo actually turns cash into long term value?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Duolingo for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the split views on Duolingo’s value leave you unconvinced either way, take a closer look at the data now and shape your own stance with the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Duolingo?

If Duolingo has sharpened your interest in fresh opportunities, do not stop here. Use curated screeners to spot other stocks that could fit your approach.

- Target long term compounding potential by reviewing companies that combine quality fundamentals with attractive prices through the 41 high quality undervalued stocks

- Prioritise staying power by scanning companies with stronger balance sheets and fundamentals using the solid balance sheet and fundamentals stocks screener (47 results)

- Hunt for tomorrow’s potential standouts before they hit the spotlight by checking the screener containing 18 high quality undiscovered gems

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.