DuPont de Nemours (DD) Pulls Back, Is The Stock Still Trading Above Fair Value?

E. I. du Pont de Nemours and Company DD | 0.00 |

Recent trading in DuPont de Nemours (DD) has drawn attention after the stock declined 4.1% over the past week and 5.5% over the past month, despite strong 1 year and multi year total returns.

At a share price of $137.22, DuPont de Nemours has given up some recent momentum, with the share price down 4.1% over 7 days and 5.5% over 30 days. However, its 1 year and multi year total shareholder returns remain strong, suggesting recent weakness may reflect a shift in short term sentiment rather than a reversal of the broader story.

If this recent pullback has you looking beyond DuPont de Nemours, it could be a good moment to scan other industrial and materials plays using the 20 top founder-led companies

So with DuPont de Nemours trading at $137.22 alongside an indicated discount to some valuation estimates, is this recent pullback opening a genuine buying opportunity, or is the market already pricing in much of its future growth?

Most Popular Narrative: 114.4% Overvalued

Compared to the last close at $137.22, the most followed narrative pegs DuPont de Nemours at a fair value of $64.00, implying a steep premium in the current price and a lot of expectation built into the story.

DuPont's strengthened balance sheet, exceptional cash generation, and operational discipline following recent divestitures and settlements create dry powder for both aggressive strategic acquisitions and meaningful buybacks, with a structural uplift to earnings per share and potential for positive revisions to capital return targets.

Want to understand why this narrative supports such a gap to today’s share price? The core assumptions hinge on ambitious revenue expansion, sharply higher margins, and a much richer earnings profile. Curious which performance milestones would need to fall into place for DuPont de Nemours to justify that $64.00 fair value and the implied future earnings multiple baked into this view? The full narrative lays out each step in that growth blueprint in detail.

Result: Fair Value of $64.00 (OVERVALUED)

However, this upbeat DuPont de Nemours narrative still faces real pressure from PFAS related litigation and higher ESG compliance costs, which could squeeze future profitability.

Another View: DCF Signals A Very Different Picture

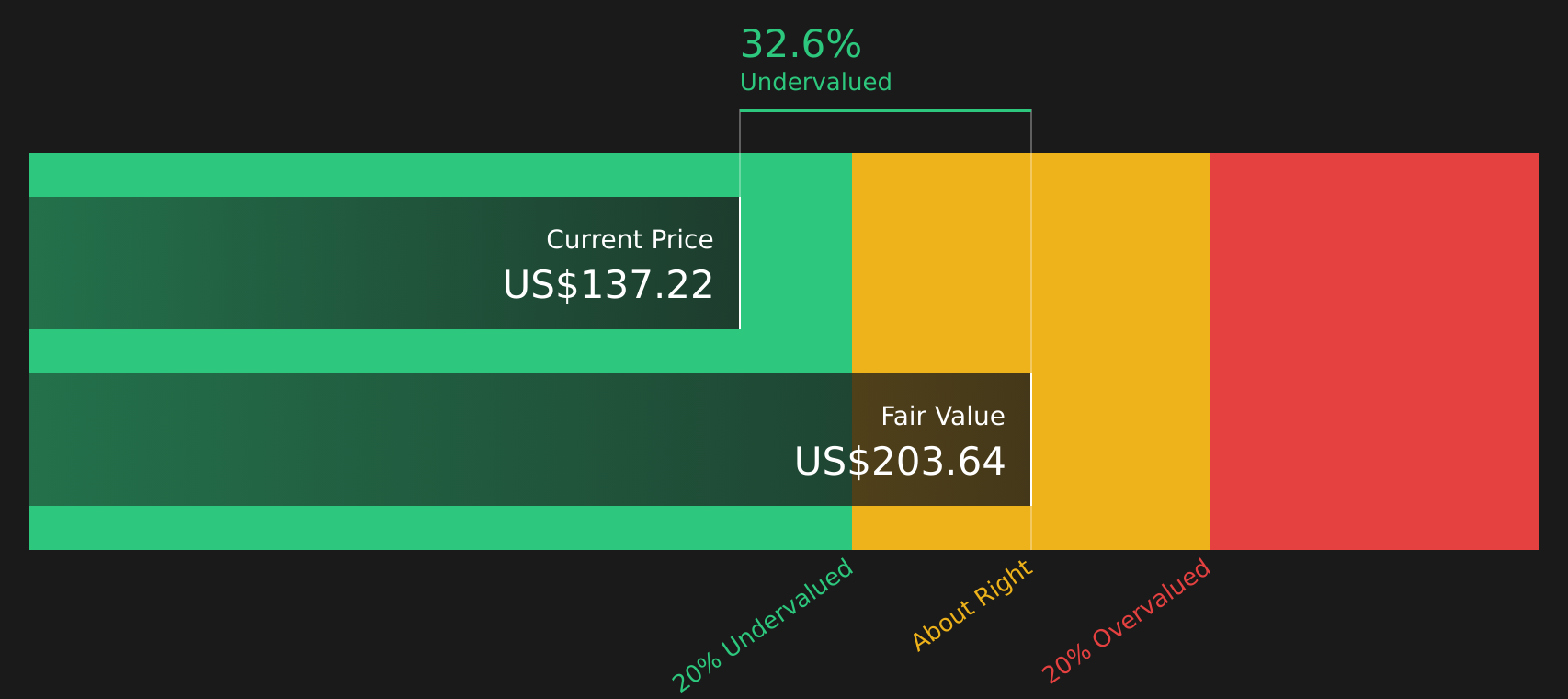

While the narrative driven fair value of $64.00 suggests DuPont de Nemours is 114.4% overvalued, the Simply Wall St DCF model paints nearly the opposite picture. With the stock at $137.22 and a future cash flow value estimate of $203.64, the model points to a 32.6% discount. Which lens do you trust more when cash flows and sentiment disagree so sharply?

To understand how those cash flow assumptions are built and what would need to change for the gap to close, take a closer look at the SWS DCF model using the Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out DuPont de Nemours for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on DuPont de Nemours clearly split between risk and reward, it makes sense to move quickly and weigh the 4 key rewards and 2 important warning signs.

Looking for more investment ideas beyond DuPont de Nemours?

If the split views on DuPont de Nemours have you thinking about diversification, now is the time to scan fresh ideas before the next move passes you by.

- Target reliable income streams by reviewing 8 dividend fortresses that focus on companies offering higher yields with an emphasis on consistency.

- Refresh your watchlist with screener containing 19 high quality undiscovered gems that highlight lesser known companies backed by solid fundamentals.

- Dial back portfolio risk by checking 71 resilient stocks with low risk scores designed to surface companies with more resilient profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.