DuPont De Nemours (DD) Stock Could Be 16.4% Undervalued Based On Analyst Targets

E. I. du Pont de Nemours and Company DD | 0.00 |

DuPont de Nemours (DD) is back in focus after investors revisited the stock following its recent share price moves, prompting a closer look at how its returns line up with current fundamentals.

At a share price of $47.71, DuPont de Nemours has seen its short term momentum cool slightly with a 1 day share price return that declined 0.50%. However, its 90 day share price return of 12.42% and 1 year total shareholder return of 73.77% point to stronger underlying interest and a solid longer term outcome for investors who have held the stock through recent volatility.

If DuPont de Nemours has you reassessing the materials sector, this can be a good moment to widen your search with a curated list of 20 top founder-led companies

With DuPont de Nemours trading at $47.71 and indicators such as its intrinsic discount and gap to analyst targets in play, the key question is whether this stock still trades below fair value or if the market is already pricing in future growth.

Most Popular Narrative: 16.4% Undervalued

On the latest numbers, the most followed narrative sees DuPont de Nemours' fair value at $57.07 versus the $47.71 share price. This frames a discount that rests heavily on future earnings power and margin improvement.

The analysts have a consensus price target of $57.07 for DuPont de Nemours based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $64.0, and the most bearish reporting a price target of just $52.0.

Curious what sits behind that higher fair value for DuPont de Nemours? The narrative leans on a step change in earnings, firmer margins and a future valuation multiple. This assumes the business mix looks very different to today.

Result: Fair Value of $57.07 (UNDERVALUED)

However, this DuPont de Nemours narrative could be upset if PFAS related legal costs bite harder than expected, or if portfolio changes leave the business less diversified.

Another View: DuPont de Nemours Through Earnings Multiples

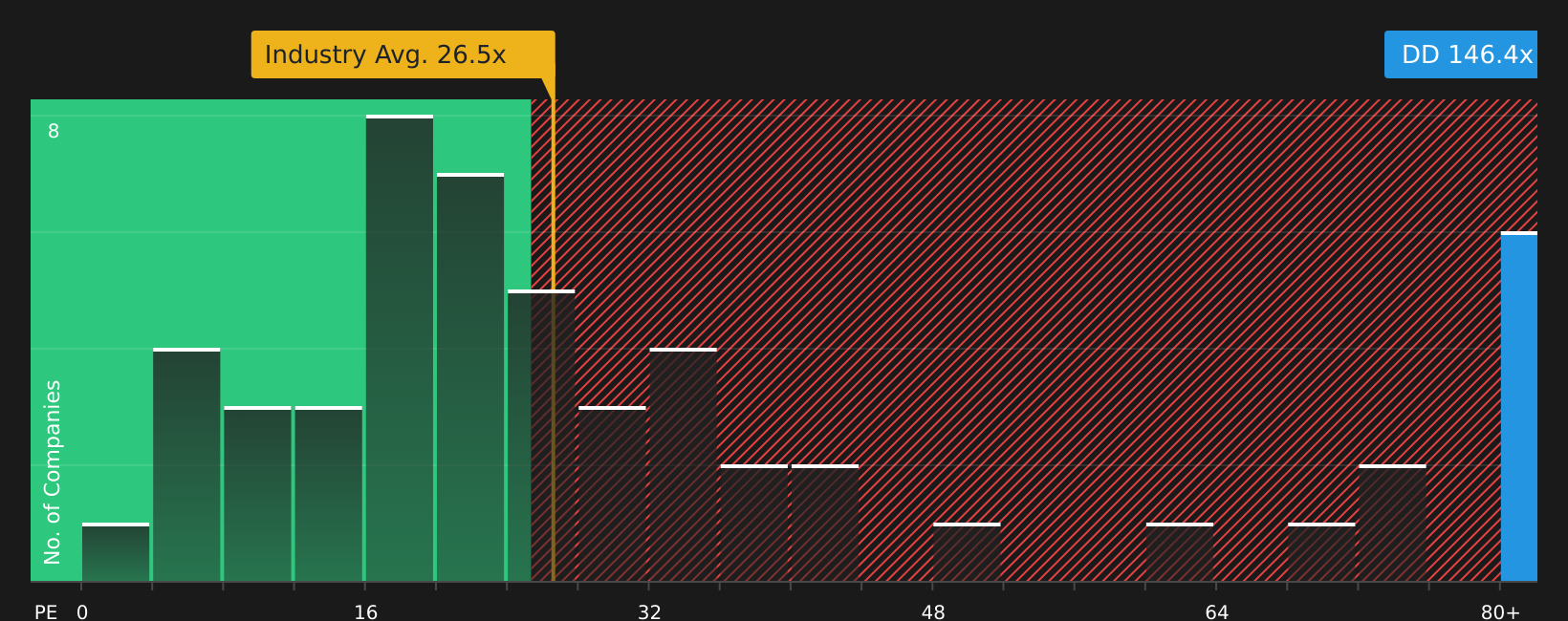

There is a catch with DuPont de Nemours trading below some fair value estimates. On a P/E basis, the stock sits at 146.4x compared with 26.6x for the US Chemicals industry and a fair ratio of 31.2x, which points to a rich earnings multiple that could compress if expectations cool.

For investors, that spread means a lot of future earnings strength is already reflected in the current P/E, so the question is whether you are comfortable paying this kind of premium for DuPont de Nemours today or prefer to look for a lower multiple entry point.

Next Steps

With both risks and rewards in play for DuPont de Nemours, this is a moment to move quickly, review the key data, and judge for yourself using the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond DuPont de Nemours?

If DuPont de Nemours has sharpened your focus on quality and valuation, do not stop here. Broaden your watchlist now using targeted stock ideas that fit your style.

- Prioritize resilience and steadier portfolios by scanning 66 resilient stocks with low risk scores that score well on downside protection and overall risk metrics.

- Hunt for quality at a discount by reviewing 45 high quality undervalued stocks that pair solid fundamentals with prices that sit below their assessed worth.

- Spot future standouts early by working through a screener containing 20 high quality undiscovered gems before they gain wider market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.