Ecolab (ECL) Stock Looks Pricey On Cash Flow And Earnings

Ecolab Inc. ECL | 0.00 |

Ecolab stock has delivered a 59.4% gain over the past three years, yet current checks suggest investors are paying a premium, with both the market multiples and a Discounted Cash Flow (DCF) intrinsic value estimate pointing to the shares trading above their estimated worth.

- A 59.4% return over three years puts Ecolab firmly in the group of stocks where valuation can matter more than ever to future returns.

- Recent attention on Ecolab's push into AI cooling and high-tech water solutions may support expectations for higher long term cash flows, while the risk is that paying up today leaves less room if that growth or profitability path is slower or more uneven than hoped.

- Ecolab scores 0 out of 6 on the broader valuation checks, which leans expensive rather than reading as a clear bargain.

For investors, the debate is whether Ecolab's quality and growth plans justify paying above the current intrinsic value estimate suggested by the Discounted Cash Flow (DCF) work and earnings multiples.

Does Ecolab Look Pricey on Cash Flow?

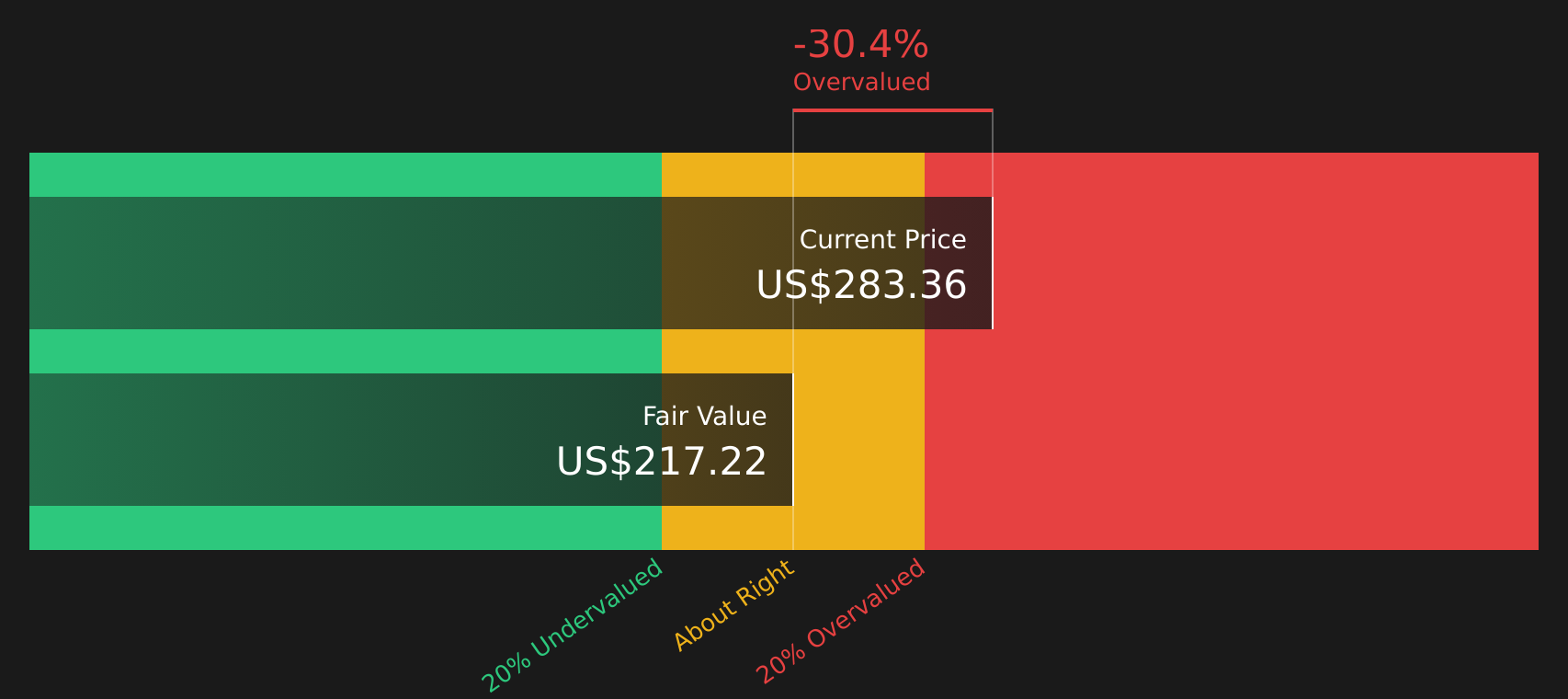

The Discounted Cash Flow (DCF) approach here uses Ecolab’s projected cash generation to estimate what the stock could be worth. In this model, Ecolab is treated as a business with growing free cash flows, starting from last twelve month free cash flow of about $2.0b and stepping up gradually over the coming decade.

Those cash flow projections translate into an estimated intrinsic value of about $217 per share. Compared with the current share price, that implies the stock trades around 30.4% above this DCF estimate, so on these assumptions Ecolab screens as overvalued rather than cheap. Despite the recently completed $4.75b CoolIT acquisition giving Ecolab a larger footprint in AI cooling and high tech water services, the market price already sits well ahead of what this cash flow model supports.

On the DCF numbers used here, Ecolab stock currently looks overvalued relative to its estimated intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests Ecolab may be overvalued by 30.4%. Discover 44 high quality undervalued stocks or create your own screener to find better value opportunities.

Has Ecolab Run Too Far on Earnings?

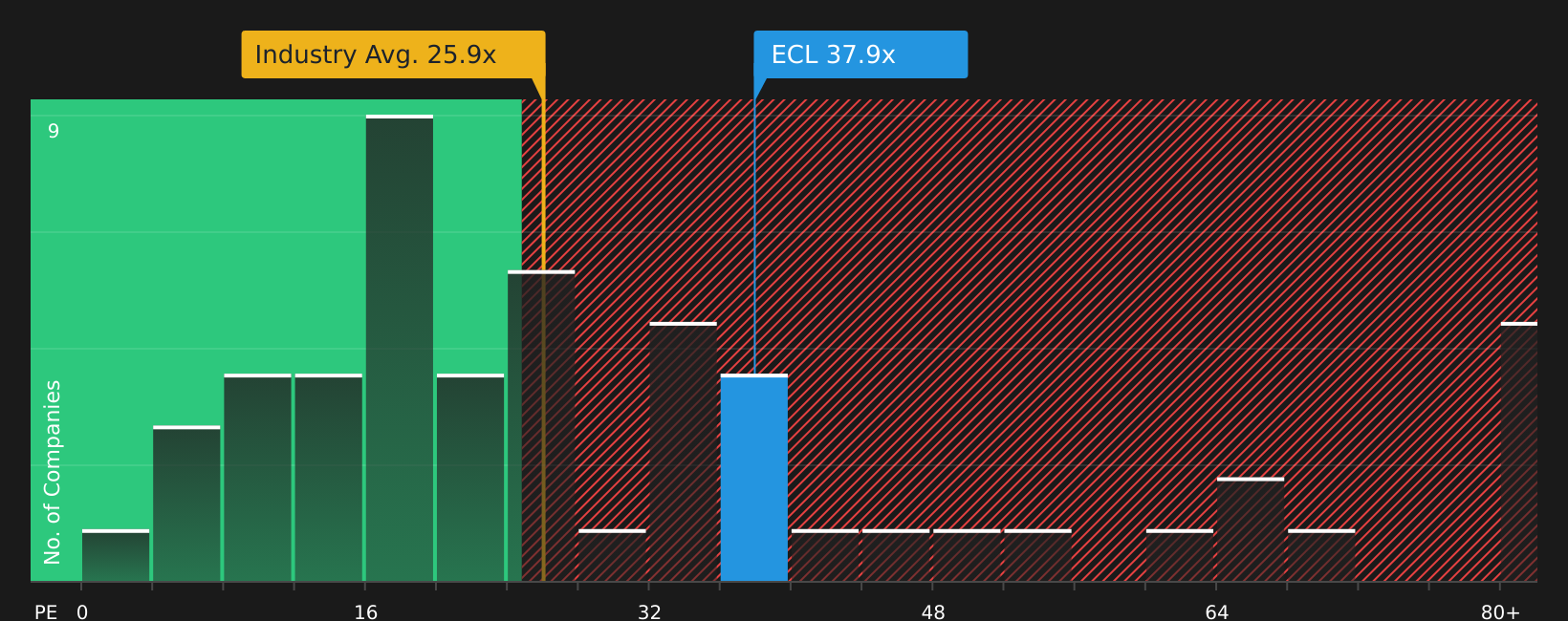

P/E is a useful lens for Ecolab because earnings are a key focus for investors in established, cash generative businesses. On this measure, Ecolab trades on a P/E of about 37.9x, which sits meaningfully above both the Chemicals industry average of roughly 25.7x and the peer group average of about 24.6x. That alone suggests the market is assigning Ecolab a clear premium relative to many comparable stocks.

A more tailored yardstick, the modelled fair P/E ratio of about 23.9x, incorporates factors such as Ecolab’s growth profile, margins, scale and risk. Set against that fair multiple, the current 37.9x implies investors are paying a substantial premium for the company’s earnings, even after accounting for those fundamentals. The result is a valuation that appears to price in significant optimism around Ecolab’s business plans and execution.

On the P/E multiple, Ecolab stock currently appears overvalued, with the market pricing its earnings well above what this framework suggests is reasonable.

The Ecolab Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Ecolab aim to connect the current valuation puzzle with the underlying expectations driving it, by spelling out what would need to happen to Ecolab's growth, margins and earnings for the stock to be worth meaningfully more or less than today. Rather than relying on a single multiple or model output, each Narrative lays out its own fair value assumptions so you can compare them with Ecolab's actual results as they come through.

Use this moment to add your voice to the Simply Wall St community with a clear, number driven narrative on Ecolab, including a view on whether the CoolIT acquisition and AI cooling push ultimately justify today’s valuation.

Set out your case now so you can track how it holds up as Ecolab’s results and execution on its high tech ambitions unfold over time.

Do you think there's more to the story for Ecolab? Head over to our Community to see what others are saying!

The Bottom Line

For Ecolab, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple view point to an overvalued stock, and the broader checks also sit at the weaker end. That leaves little margin for error if growth, profitability or synergies from areas like AI cooling progress more slowly or unevenly than hoped. The key question from here is whether Ecolab can deliver enough durable cash flow growth to justify today’s premium, or whether the valuation eventually has to settle closer to its intrinsic value estimate and fair P/E range.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.