Edwards Lifesciences (EW) Margin Decline Underscores Valuation Concerns Against Bullish Growth Narratives

Edwards Lifesciences Corporation EW | 80.08 | +0.73% |

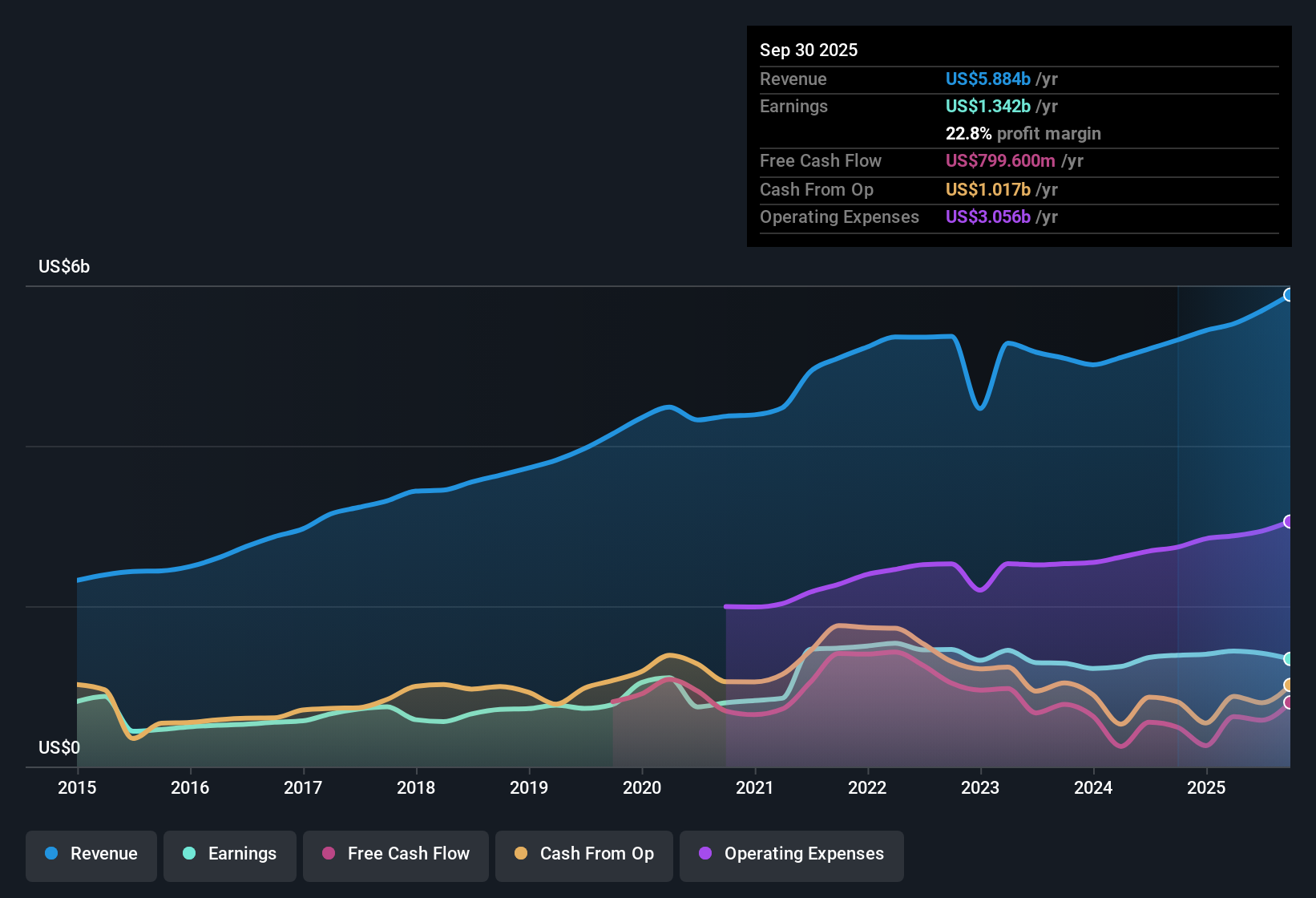

Edwards Lifesciences (EW) posted annual earnings growth averaging 4.6% over the past five years, but the most recent period saw negative earnings growth and profit margins dip to 22.8% from 26.1% a year earlier. While earnings are projected to grow at 11.5% annually and revenue at 8.9% per year going forward, both lag behind the broader US market’s anticipated growth. Investors are weighing these slower trends and tightening margins against the company’s premium valuation and reputation for high-quality earnings, with shares trading just below their estimated fair value at $82.45.

See our full analysis for Edwards Lifesciences.Next, we’ll break down how these financial results align with the dominant narratives at Simply Wall St. We will also examine where the numbers might challenge conventional wisdom.

Premium Valuation Versus Industry Peers

- Edwards Lifesciences trades at a Price-to-Earnings ratio of 36.1x, well above both its peer group average of 31x and the overall US Medical Equipment industry at 27.7x. This premium occurs even though its projected earnings and revenue growth rates are slower than the broader market.

- Analysts' consensus view points out a tension: the share price of $82.45 is just below its DCF fair value of $83.56, suggesting limited upside despite the premium multiples.

- The consensus narrative notes that with analysts setting a price target of 92.50, expectations for growth and profitability are already largely factored into the current valuation.

- There is little margin for error. Slower growth or additional margin pressure could make the stock’s premium valuation appear stretched if future operational targets are not met.

Profit Margins Narrow Amid Rising Costs

- Net profit margins have shrunk from 26.1% to 22.8% over the past year, a notable contraction that places pressure on the company's operating leverage as expenses and competition rise.

- The consensus narrative highlights that operational efficiency and product innovation, such as the launch of Sapien M3 in Europe and continued investment in surgical technologies, are central to Edwards’ efforts to hold margins steady going forward.

- Bears emphasize that ongoing tariffs and the JenaValve acquisition could further dilute EPS by $0.05 to $0.10. This reinforces concern that margin protection will be an uphill battle.

- Consensus expects profit margins to decline further, from 24.8% today to 23.7% within three years. This raises the stakes for cost control and revenue growth to offset margin risks.

Strategic Launches Drive Revenue Opportunities

- Edwards Lifesciences’ upcoming product rollouts, like the early TAVR indication approval and the EVOQUE tricuspid valve launch, are projected as key drivers for future revenue growth and expanded market share in the cardiovascular space.

- Consensus narrative recognizes that approval for the TAVR expansion and global surgical technology adoption could unlock multi-year growth, but also underscores that actual advances in sales will require both regulatory approval and competitive execution.

- What is surprising is that international competition, especially in Japan, and the pace of regulatory changes create a genuine risk of delayed market capture or lower-than-expected revenue in these new segments.

- Solid execution remains critical. Any setback in launches or slower-than-anticipated guideline updates could push out anticipated growth drivers and challenge the bullish growth case.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Edwards Lifesciences on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do the figures spark a different take? Bring your outlook to life in just a few minutes and shape a unique view. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Edwards Lifesciences.

Explore Alternatives

Despite its innovation and premium market position, Edwards Lifesciences faces slowing growth, narrowing profit margins, and elevated valuation multiples. These factors limit its upside potential.

If you want companies with better value opportunities and stronger upside potential, focus on those identified as undervalued based on fundamentals like these 830 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.