Emerson Electric (EMR) Valuation Check After Raised Guidance And Solid Q2 2026 Results

Emerson Electric Co. EMR | 0.00 |

Why Emerson Electric’s latest quarter matters for shareholders

Emerson Electric (EMR) just posted second quarter 2026 results and updated guidance, giving you fresh information on how its automation focused business is performing and what management expects for the rest of the year.

Emerson Electric’s latest earnings, guidance update, Board refresh, and dividend affirmation have all landed against a share price of $141.09, with a 1-year total shareholder return of 27.64% and a 5-year total shareholder return of 64.04%. The 90-day share price return shows a decline of 10.35% in contrast to a 30-day share price return of 4.79%, suggesting momentum has cooled recently after stronger long term gains.

If you are looking beyond industrial automation and want to see what else is moving, this could be a good moment to scan 36 power grid technology and infrastructure stocks

With the stock at $141.09 after a strong multi year run and Emerson guiding to mid single digit sales growth and higher EPS, the key question is whether this represents an attractive entry point or whether markets are already pricing in future growth.

Most Popular Narrative: 14.2% Undervalued

Emerson Electric’s most followed narrative pegs fair value at $164.51 per share, above the latest close at $141.09, anchoring a valuation built on detailed long term forecasts.

The accelerating adoption of digital automation and artificial intelligence solutions in global industrial markets is fueling strong demand for Emerson's advanced software platforms and AI-enabled products, such as Ovation 4.0 and Nigel AI adviser, which is resulting in robust order growth and positions the company for sustained revenue expansion. Large-scale investments in power generation, LNG, and life sciences driven by rising energy security concerns, electrification, and sustainability initiatives, are driving significant greenfield and modernization projects, particularly in regions like North America, Asia, and the Middle East; this is visible in sharply higher orders and is expected to continue supporting revenue and earnings growth over the coming years.

Want to see what kind of earnings path and margin profile sits behind that valuation gap? The narrative leans heavily on recurring software, higher profitability, and a richer earnings base a few years out. The exact assumptions are spelled out in the full model, including how fast revenue needs to compound and where profitability has to settle for the fair value to line up.

Result: Fair Value of $164.51 (UNDERVALUED)

However, you also need to factor in risks like softer demand in Europe and China, as well as any bumps integrating software acquisitions, which could challenge this undervaluation story.

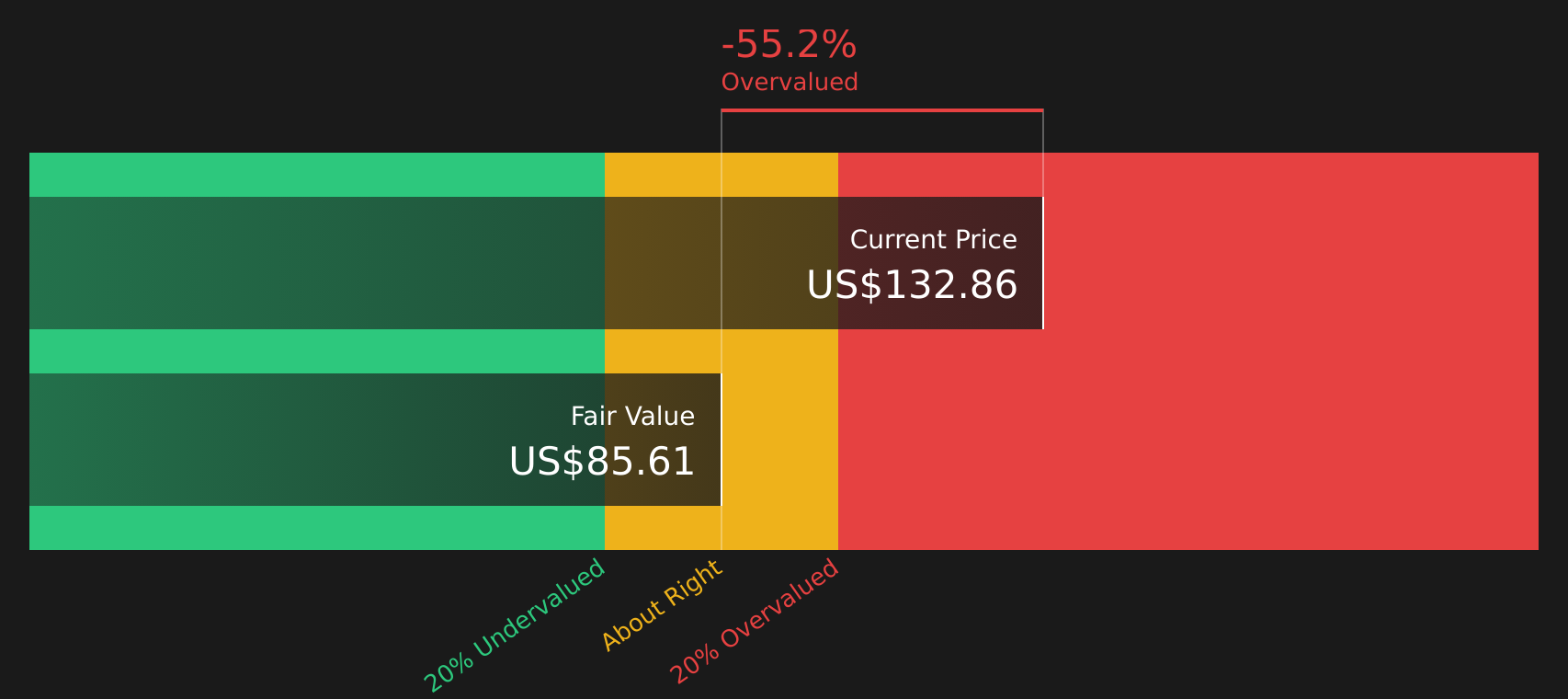

Another angle on value

While the narrative fair value of $164.51 points to a 14.2% undervaluation, our DCF model paints a very different picture. On that cash flow view, Emerson Electric’s estimated value sits at $86.20, which makes the current $141.09 share price look expensive. Which framework do you trust more for your own thesis?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Emerson Electric for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment, this is a good time to check the underlying data yourself and decide where you stand. To weigh the upside against the downside in a clear, structured way, start by reviewing the 5 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Emerson Electric is on your radar, this is the moment to broaden your watchlist and line up the next set of opportunities before others do.

- Target strong value potential by reviewing companies that screen as 51 high quality undervalued stocks and see which ones fit your return and risk preferences.

- Prioritise resilience by focusing on businesses highlighted in the 72 resilient stocks with low risk scores so you can keep volatility in check while staying invested.

- Hunt for future standouts using the screener containing 23 high quality undiscovered gems and spot quality ideas that may not yet be widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.