Encaleret NDA, Acoramidis Progress, and Buyback Could Be A Game Changer For BridgeBio (BBIO)

BridgeBio Pharma BBIO | 0.00 |

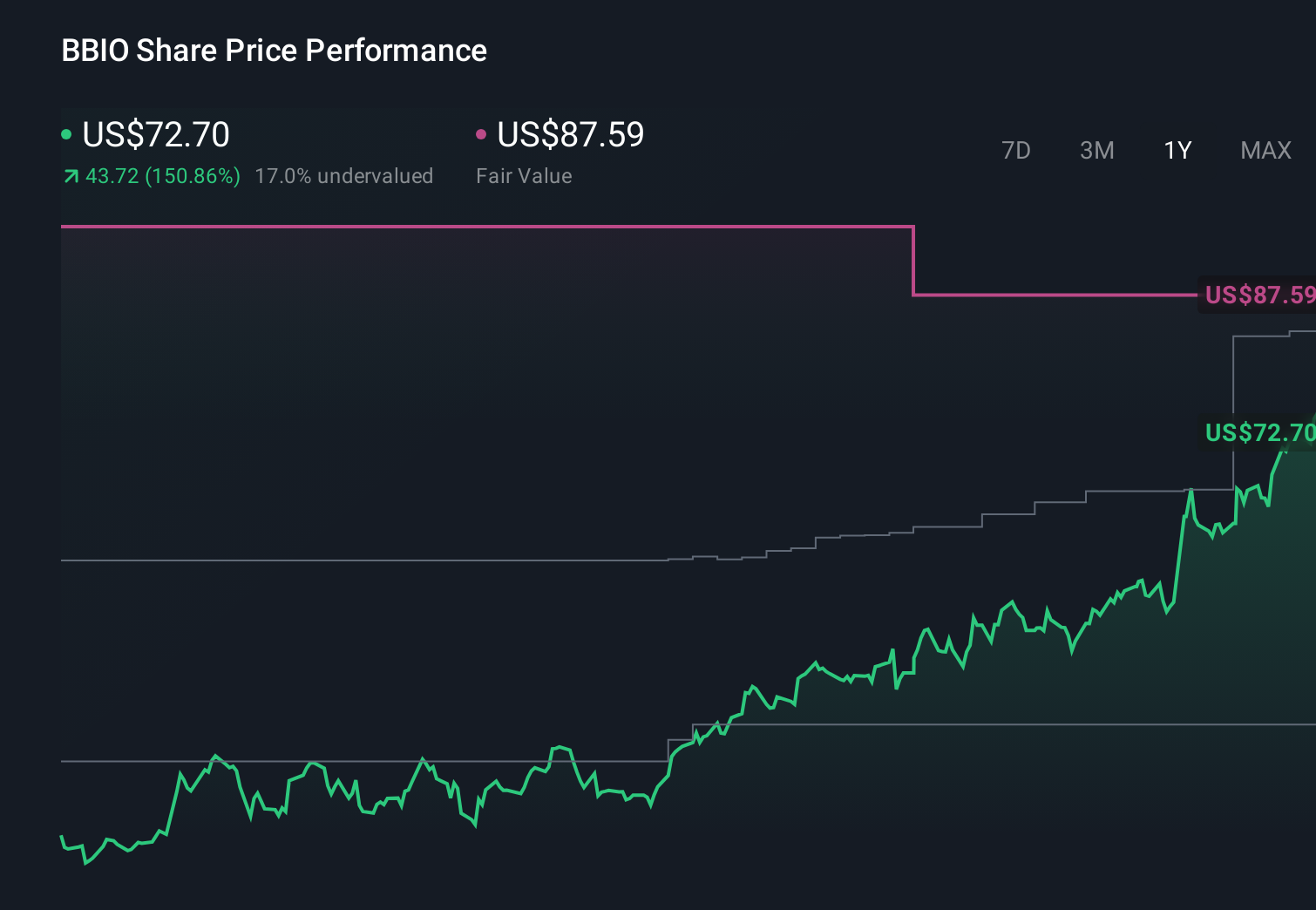

- In early May 2026, BridgeBio Pharma reported strong new clinical and regulatory progress, including FDA submission of encaleret for ADH1 and additional Phase 3 data for acoramidis (Attruby/BEYONTTRA) in transthyretin amyloid cardiomyopathy, alongside higher quarterly revenue and a newly authorized US$500,000,000 share repurchase program.

- The combination of compelling late-stage trial readouts, expanding global approvals for acoramidis, and an NDA for encaleret underscores BridgeBio’s push to convert its rare disease pipeline into multiple commercial products over the next few years.

- We’ll now examine how the encaleret NDA and encaleret’s Phase 3 success may reshape BridgeBio’s investment narrative and future revenue mix.

Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

BridgeBio Pharma Investment Narrative Recap

To own BridgeBio, you really need to believe that Attruby can support the business while a broader rare disease portfolio, led by encaleret, matures into multiple approved products. Right now, the key near term catalyst is execution on Attruby’s global launch, while the biggest risk is that heavy R&D and commercial spending keeps net losses high and increases the chance of future dilution. The encaleret NDA meaningfully supports diversification but does not remove this financing risk.

Among the recent announcements, the NDA filing for encaleret in ADH1 is most relevant. Positive Phase 3 CALIBRATE results, with 76% of encaleret patients reaching both serum and urine calcium targets versus 4% on conventional therapy, reinforce BridgeBio’s effort to reduce dependence on Attruby over time. If regulators approve encaleret on this dataset, it could become an additional rare disease revenue stream alongside other late stage programs now approaching regulatory milestones.

Yet behind the strong data, investors should be aware that persistent losses and possible future equity raises could still...

BridgeBio Pharma's narrative projects $2.4 billion revenue and $758.3 million earnings by 2029.

Uncover how BridgeBio Pharma's forecasts yield a $100.89 fair value, a 45% upside to its current price.

Exploring Other Perspectives

While the consensus sees strong upside from Attruby and encaleret, the most pessimistic analysts expected about US$1.1 billion revenue by 2028 and still no profitability, reminding you that opinions differ and this new encaleret news could shift both the bullish and bearish cases.

Explore 9 other fair value estimates on BridgeBio Pharma - why the stock might be worth less than half the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your BridgeBio Pharma research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free BridgeBio Pharma research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BridgeBio Pharma's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.