Energy Transfer (ET) Stock May Trade At A Discount On Debt Refinancing

Energy Transfer LP ET | 0.00 |

Energy Transfer stock has delivered very strong 5 year returns, yet the current valuation picture is more nuanced, with solid recent gains sitting alongside a mixed set of broader value checks.

- Energy Transfer has returned 201.6% over the past 5 years, putting long term holders well ahead and raising the question of how much upside is already reflected in the price.

- Recent refinancing moves and a favorable Texas court judgment can support views of healthier cash flows, while investors still face risks around large project execution and regulatory challenges that may affect how the stock is priced.

- The broader valuation framework is mixed, with Energy Transfer screening as undervalued on earnings multiples but scoring 4 out of 6 on value checks. This points to a company that is not a straightforward bargain or an obvious overpricing story.

The issue now is whether Energy Transfer's strong run and recent balance sheet developments leave enough valuation headroom for new capital going into the stock.

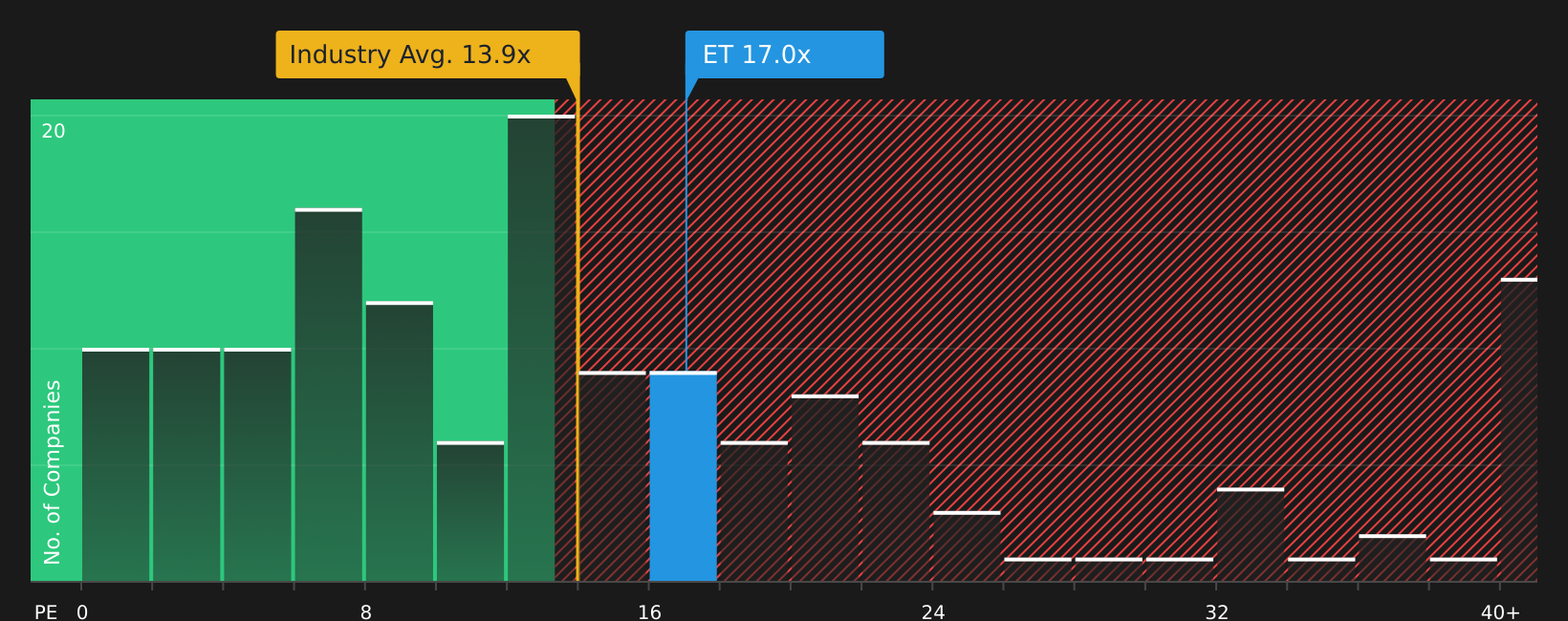

Does Energy Transfer Look Undervalued on Earnings?

The P/E ratio suits Energy Transfer because earnings are a key driver for how investors typically look at pipeline and midstream businesses. On this measure, Energy Transfer trades on a P/E of 16.9x, which sits below the peer average of 19.2x and above the broader oil and gas industry average of 13.7x. That places the stock between the sector and closer pipeline peers, suggesting investors are paying a moderate earnings multiple for the company.

The fair P/E ratio implied by the model is 25.7x. The current 16.9x level is well under that tailored benchmark that incorporates Energy Transfer's size, risk profile and industry positioning. Because the recent subordinated notes refinancing and Winter Storm Uri court win have focused attention on cash flows and balance sheet structure, the gap between the current and fair multiple stands out even more.

On the P/E measure, Energy Transfer stock currently screens as undervalued relative to the earnings multiple the model suggests investors might typically pay.

The Energy Transfer Narrative: What Would Justify Today's Price?

Simply Wall St Narratives take the valuation puzzle around Energy Transfer and spell out which assumptions on future growth, margins and earnings would need to hold for the stock to be worth substantially more or less than it is today. They sit on the company’s Community page. Each Narrative links a fair value estimate to a specific storyline about Energy Transfer's potential catalysts and key risks, so you can track over time which version of events is actually unfolding.

If you have a number driven view on whether Energy Transfer's recent refinancing and Winter Storm Uri court win ultimately justify today's price, consider sharing a Narrative so the Simply Wall St community can see how your thesis holds up as new results and news arrive.

Do you think there's more to the story for Energy Transfer? Head over to our Community to see what others are saying!

The Bottom Line

Energy Transfer looks undervalued on its current P/E against a tailored earnings multiple, but the broader checks are only mixed, not overwhelmingly supportive. That leaves the stock in a middle ground where the valuation gap may appeal to some, yet is balanced by ongoing project and regulatory risks that could justify a discount. For investors, the key question from here is whether Energy Transfer can deliver the cash flow resilience and execution needed to warrant a higher multiple, or whether the present pricing already reflects those uncertainties appropriately.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.