Energy Transfer (ET) Stock Still Looks Discounted On Earnings Value

Energy Transfer LP ET | 0.00 |

Energy Transfer has delivered a very strong 166.2% return over the past 5 years, yet on most basic valuation checks the stock still screens as inexpensive. This raises a clear question about how much of its recent progress is already reflected in the price.

- A 166.2% gain over 5 years suggests Energy Transfer has already rewarded long term holders. Any new position or added exposure therefore rests on whether that momentum can be justified by current and future cash flows.

- Growth projects tied to natural gas and NGL infrastructure can support expectations for steady cash generation, while the heavy capital program required to build and expand those assets may weigh on how investors price the units.

- On Simply Wall St's broader checks, Energy Transfer looks cheap in most areas, with a value score of 5 out of 6 suggesting the valuation leans toward undervalued rather than fully priced in.

For investors, the debate is whether Energy Transfer's strong multi year return and active growth pipeline still leave enough upside in the current valuation to compensate for the ongoing investment and execution risks.

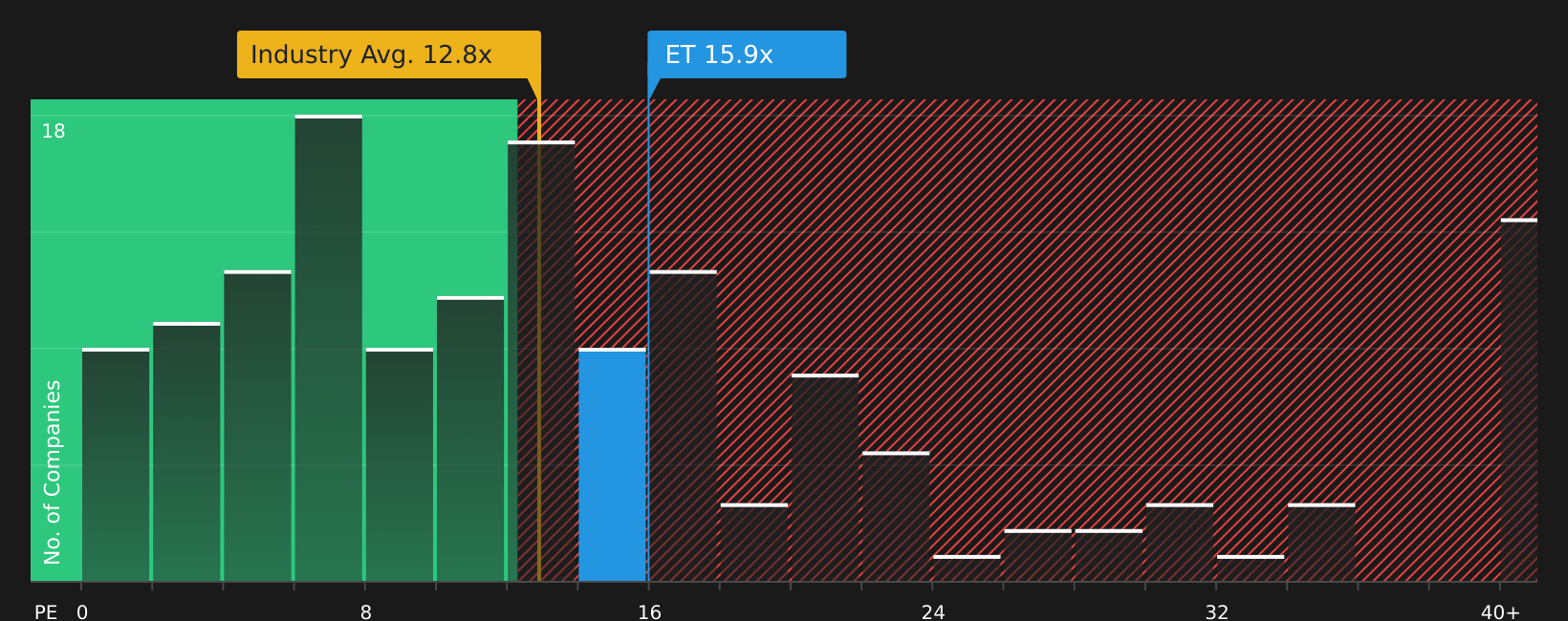

Is Energy Transfer a Bargain on Earnings?

The P/E ratio suits Energy Transfer because earnings remain a core yardstick for a mature, fee based midstream business. Energy Transfer currently trades on a P/E of about 16.0x, below the oil and gas industry average of 12.7x and also below the broader peer average of 18.6x, so the market is not assigning a clear premium or a deep discount versus either reference point.

On Simply Wall St’s model of what investors might typically pay for Energy Transfer given its profile, the fair P/E ratio is around 26.2x, which is materially higher than where the stock trades today. Despite recent project announcements and raised guidance, the current multiple still sits well under that fair ratio. This points to a gap between the earnings price the model suggests and what the market is currently willing to pay.

On the P/E yardstick alone, Energy Transfer stock appears undervalued relative to the earnings multiple implied by the fair ratio model.

The Energy Transfer Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where Energy Transfer's valuation puzzle leaves off by spelling out the specific growth, margin and earnings paths that would need to hold for the stock to be worth materially more or less than today's price, and they sit on the company's Community page. Rather than focusing on a single multiple or model, each narrative lays out the assumptions behind its fair value estimate so you can compare those expectations with Energy Transfer's reported results over time.

Be one of the first voices in the Simply Wall St community to set out a number-driven case on Energy Transfer, including a view on whether its expansion projects and higher guidance really justify where the stock trades today.

Lay out your narrative now and see how your thesis holds up as Energy Transfer's volumes, contracts and cash flows are reported over time.

Do you think there's more to the story for Energy Transfer? Head over to our Community to see what others are saying!

The Bottom Line

Energy Transfer screens as undervalued on earnings multiples, suggesting the current unit price does not fully reflect what the business is already generating today. The high overall value score reinforces that message, but it does not erase the execution and capital intensity questions around its growth projects. For you as an investor, the key issue is whether those projects can sustain solid cash generation without requiring so much reinvestment that the market keeps a lid on the P/E multiple. That tension between apparent value and ongoing capital demands is what will likely decide whether Energy Transfer remains a discount or proves to be a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.