Entergy (ETR) Stock Could Be 9% Undervalued as $40b Investment Plan Comes Into Focus

Entergy Corporation ETR | 0.00 |

Entergy (ETR) continues to draw investor attention after recent share price moves, prompting a closer look at how its current valuation aligns with fundamentals such as revenue, net income and longer term total return performance.

Over the past year, Entergy’s share price return has been strong and the 1 year total shareholder return of 37.9% and 5 year total shareholder return of 159.4% indicate sustained momentum. This frames today’s US$111.11 level within a longer running re rating by the market.

If Entergy’s recent moves have you thinking about where electricity infrastructure fits in your portfolio, this is a good moment to scan the 34 power grid technology and infrastructure stocks for ideas beyond a single utility stock.

So with Entergy now at about US$111.11 after strong recent total returns, are investors still getting in at a reasonable price based on current revenues and earnings, or is the stock already reflecting much of its potential from here?

Most Popular Narrative: 9% Undervalued

Entergy’s most followed narrative points to a fair value of about $121.88, which sits above the recent $111.11 share price and frames the current debate around how much future earnings power is already reflected.

Capital investment of $40 billion over four years (with an expanded pipeline for renewables, grid modernization, and resilience upgrades) is expected to grow the company's rate base and support above-average EPS and earnings growth for several years.

Read the complete narrative. Read the complete narrative.

Want to see what sits behind that number? The narrative leans heavily on compounding revenue, rising margins, and a future earnings multiple more often associated with faster growth sectors.

Result: Fair Value of $121.88 (UNDERVALUED)

However, Entergy’s heavy capital needs and concentration in the Gulf South, with exposure to extreme weather and regulatory decisions, could challenge the current undervalued narrative.

Another View on Entergy’s Valuation

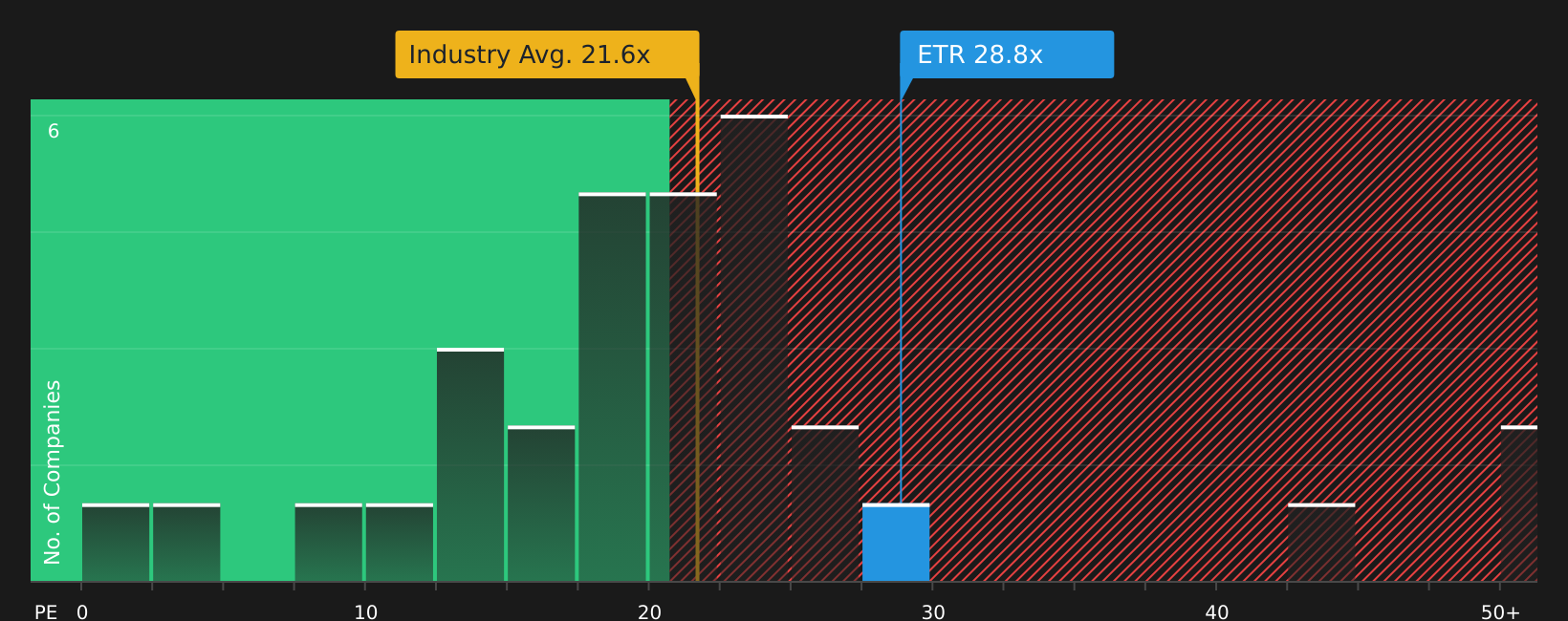

While the prevailing Entergy story leans on a fair value of about $121.88 and an undervalued label, the current P/E of 28.5x tells a different story. It sits well above the US Electric Utilities industry at 21.4x and a fair ratio of 26.6x, which points to limited margin for error if expectations slip.

For context on how this compares with broader valuation work, and what the current pricing gap might mean for risk, see what the numbers say about this price in our valuation breakdown. See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mixed sentiment on Entergy has you on the fence, this is the time to weigh the upside against the concerns and decide where you stand. Start by reviewing the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Entergy?

If Entergy has sharpened your focus on opportunities in utilities and beyond, do not stop here. Broaden your watchlist and pressure test your next moves.

- Target potential mispriced opportunities by scanning the 45 high quality undervalued stocks that combine solid fundamentals with room for sentiment to shift.

- Strengthen the income side of your portfolio by reviewing the 8 dividend fortresses that pair higher yields with an emphasis on resilience.

- Reduce portfolio stress by focusing on the 66 resilient stocks with low risk scores that score well on financial stability and risk metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.