Enterprise Products Partners (EPD) Stock Could Be Below Fair Value As CEO Succession Nears

Enterprise Products Partners L.P. EPD | 0.00 |

Enterprise Products Partners stock has delivered a 118.5% total return over the past 5 years, yet current valuation checks point to a mixed picture rather than an obvious bargain or clear overpricing.

- A 118.5% 5 year return suggests that long term holders have already seen substantial gains, so fresh buyers may be wondering how much upside is still on the table.

- Growth projects in natural gas gathering and processing, alongside a long record of returning cash to unitholders, can support the investment case. At the same time, upcoming leadership changes and the need for ongoing regulatory support for new infrastructure may add risk to how those cash flows are valued.

- Enterprise Products Partners scores 4 out of 6 on Simply Wall St's broader valuation checks. This points to a mixed valuation picture rather than a clear-cut opportunity or obvious excess pricing, see here.

The issue now is whether Enterprise Products Partners' current price fairly reflects its income profile and project pipeline, or if the long run of returns has already captured most of that value.

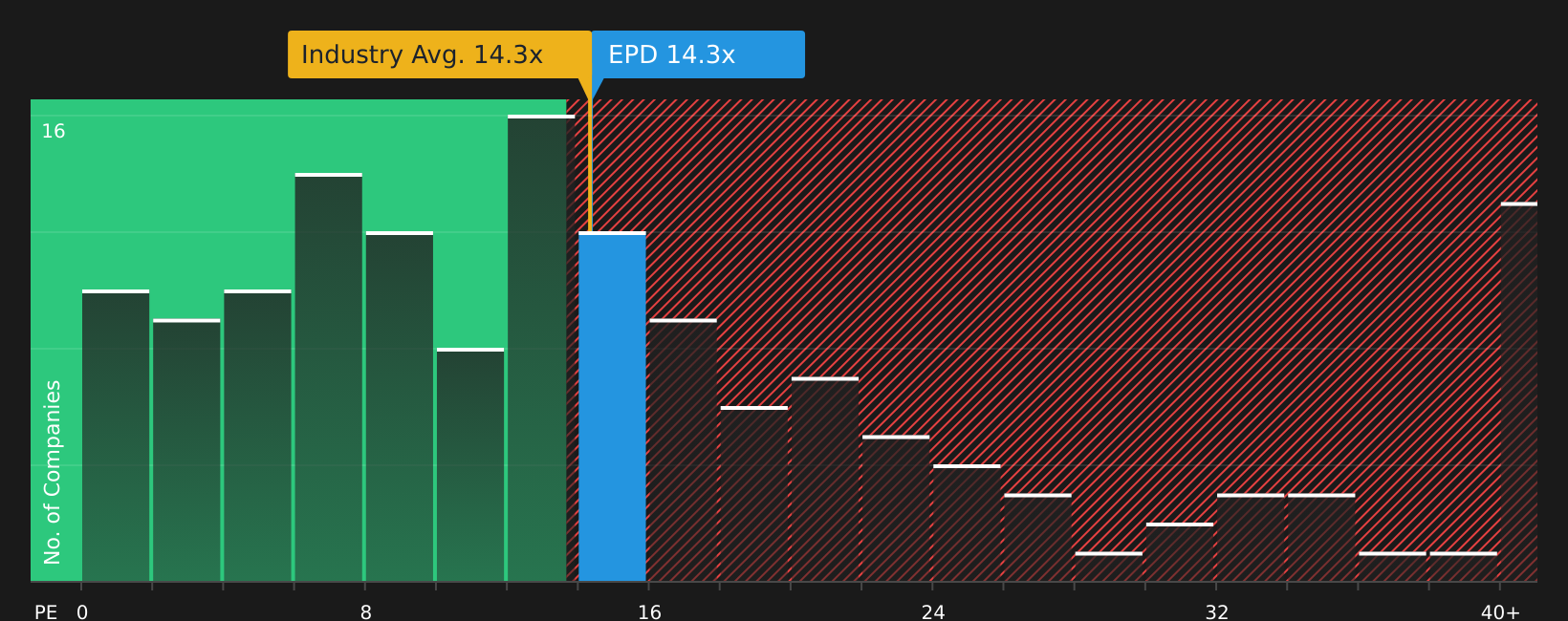

Is Enterprise Products Partners a Bargain on Earnings?

The P/E multiple suits Enterprise Products Partners because investors commonly look at earnings when judging income focused pipeline businesses. Enterprise Products Partners currently trades on a P/E of about 13.6x, slightly above the Oil and Gas sector average of 12.8x but below the broader peer average of 24.0x. This suggests the market is not putting a premium tag on the stock compared with many other energy companies.

The Fair Ratio model, which factors in Enterprise Products Partners' earnings profile, size and risk, points to a P/E of about 23.1x as a more tailored benchmark. That is well above the current 13.6x, implying the units trade at a discount on this earnings based yardstick even after years of steady distributions and a sizable project pipeline.

On the P/E measure, Enterprise Products Partners stock appears undervalued relative to what the tailored Fair Ratio would suggest.

The Enterprise Products Partners Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Enterprise Products Partners are designed to turn that valuation puzzle into clear, testable views about what would need to happen to growth, margins and earnings for the stock to be worth significantly more or less than it is today. They sit on the company’s Community page, and each one links its number to a specific view of how Enterprise Products Partners' growth, profitability and key risks might evolve, giving you a reference point you can revisit as new information comes through.

Share a narrative on Enterprise Products Partners' stock to present a number-driven view of its distribution record, project pipeline and leadership transition, and track how that thesis holds up as new results and capital project updates come through.

Do you think there's more to the story for Enterprise Products Partners? Head over to our Community to see what others are saying!

The Bottom Line

For Enterprise Products Partners, the P/E based signals point to an undervalued stock, yet the broader set of checks is only mixed, not an outright green light. That gap largely comes down to how much weight you put on its earnings multiple versus the execution and regulatory risks tied to future projects. The key question from here is whether the current discount reflects genuine mispricing or is simply the market’s way of pricing those ongoing uncertainties into Enterprise Products Partners’ units.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.