Equity LifeStyle Properties (ELS) Valuation Check After First Quarter 2026 Dividend Update

Equity LifeStyle Properties, Inc. ELS | 63.99 | +1.15% |

Equity LifeStyle Properties (ELS) has declared a first quarter 2026 dividend of $0.5425 per common share, equivalent to $2.17 on an annualized basis, with payment scheduled for April 10 to shareholders of record on March 27.

At a share price of US$65.95, Equity LifeStyle Properties has seen a 10.30% year to date share price return and a 21.11% total shareholder return over five years. The recent dividend update helps frame current momentum as steady rather than explosive.

If this income update has you thinking about other opportunities, it might be a good moment to broaden your search with our 22 top founder-led companies.

With the stock at US$65.95, an indicated annual dividend of US$2.17, a value score of 2, and an estimated 20% intrinsic discount, you might ask: is ELS quietly undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 4.8% Undervalued

With Equity LifeStyle Properties last closing at $65.95 against a narrative fair value of about $69.26, the current price sits slightly below that central view and sets up an interesting backdrop for what is driving the gap.

The combination of an aging U.S. population and a persistent housing affordability crisis continues to drive demand for manufactured home and RV communities, supporting above-average occupancy levels (94%+ in the MH portfolio) and enabling stable long-term rent growth; this trend is likely to positively impact both revenue and net operating income (NOI) growth over the coming years.

Ongoing investment in new home inventory and site development, especially in high-growth, supply-constrained Sunbelt markets (Florida, Arizona, California), positions the company to capture incremental revenue from population in-migration and resilient demand for affordable, low-maintenance housing; this helps drive mid

Curious how steady occupancy, measured rent growth, margin assumptions and a specific earnings multiple all connect to that fair value estimate? The narrative describes the growth run rate, profit profile and discount rate that need to align for $69.26 to make sense. The numbers behind that view are more precise than the current share price suggests.

Result: Fair Value of $69.26 (UNDERVALUED)

However, that narrative can unravel if weather related costs in Florida, California and Arizona climb faster than expected, or if RV and marina occupancy remains under pressure.

Another Way To Look At ELS

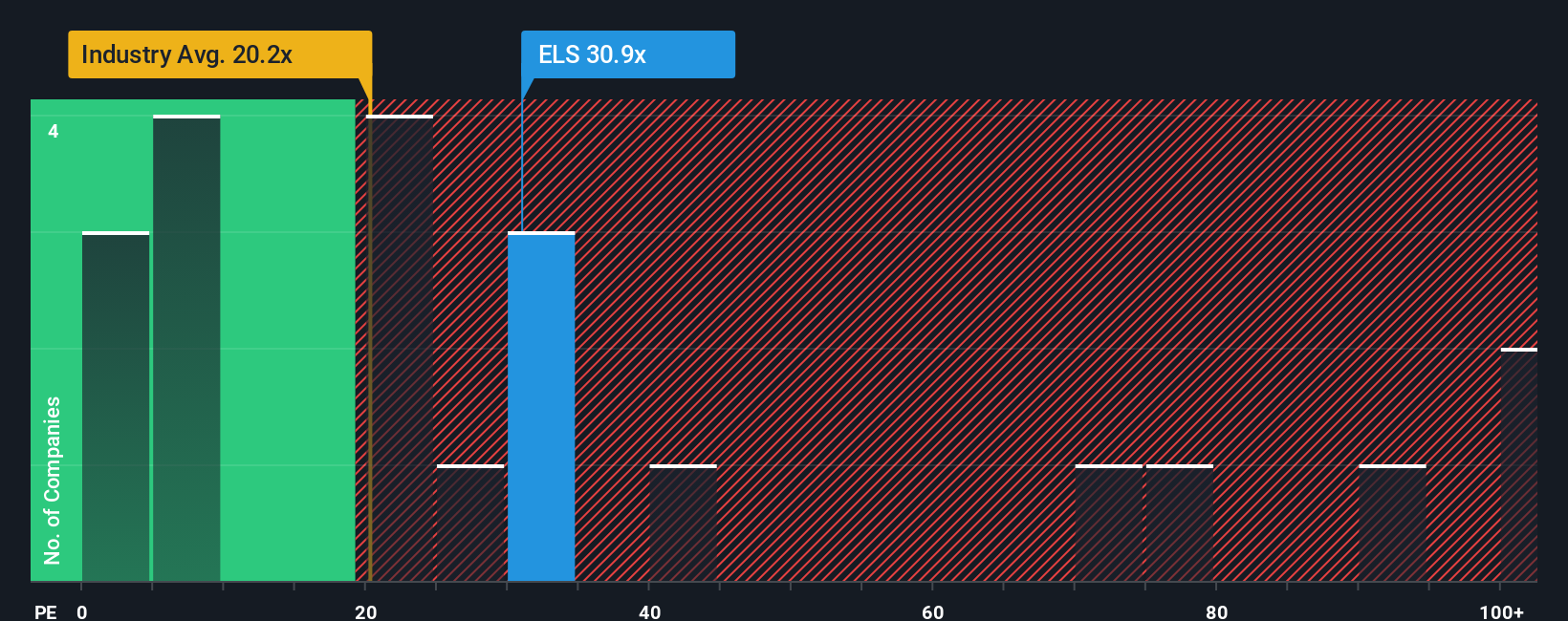

While the SWS DCF model suggests ELS at $65.95 is trading below an estimated future cash flow value of $82.44, the picture gets more complicated when you look at the P/E. At 33.1x, it sits above the peer average of 30.3x, the sector at 26.7x, and even its own 32.6x fair ratio. This points to some valuation stretch and raises a key question: is this a margin of safety, or a premium you are paying for comfort and consistency?

Build Your Own Equity LifeStyle Properties Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a complete view in just a few minutes with Do it your way.

A great starting point for your Equity LifeStyle Properties research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you stop with one company, you risk missing some of the most interesting opportunities our tools are already lining up for you.

- Spot potential mispricings early by scanning our 51 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect them.

- Lock in more predictable income streams by reviewing our 13 dividend fortresses that focus on higher yielding payouts.

- Sleep easier at night by checking our 85 resilient stocks with low risk scores that score well on balance sheet strength and risk factors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.