eToro (ETOR) Stock Could Be 29% Overvalued On Cash Flow Doubts

eToro Group Ltd. Class A ETOR | 0.00 |

eToro Group stock is trying to recover from a difficult year, yet the valuation signals are split, with the Excess Returns intrinsic value estimate pointing to a premium price while earnings based multiples still screen as supportive and the overall checks lean expensive.

- Over the past 12 months, eToro Group shares are down 38.6%, which keeps recent gains in perspective for anyone assessing the current price.

- The key support for the valuation case can come from the market's expectations for eToro Group's ability to convert its trading activity into durable cash flows, while any setbacks in profitability or balance sheet strength may quickly weaken that support.

- On Simply Wall St's broader checks, eToro Group only passes 2 of 6 valuation tests, which suggests the stock is not a clear bargain overall despite what the multiples imply. You can see the score detail at 2/6.

The stock's next move may depend on whether the market continues to back the intrinsic value premium implied by the Excess Returns model or sides with the caution signaled by the low value score.

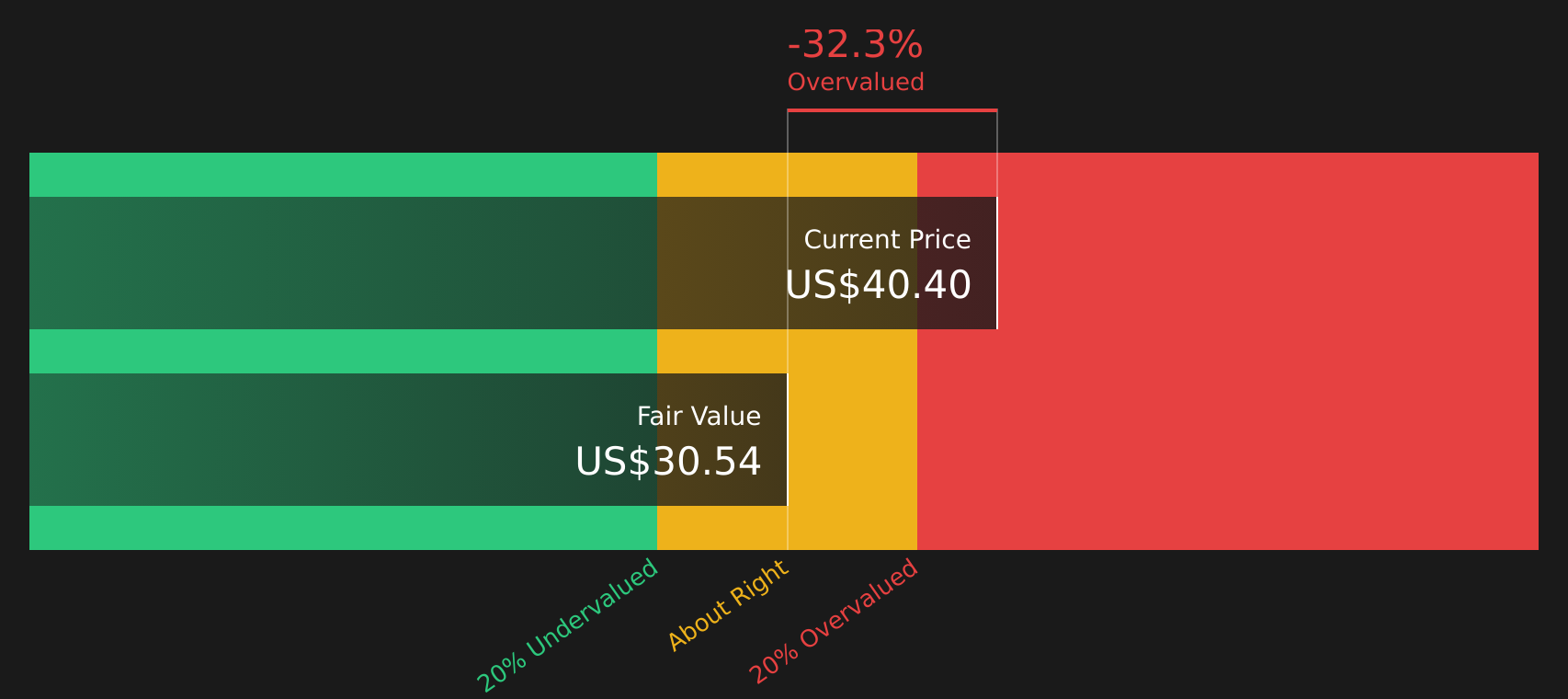

Has eToro Group Run Too Far on Excess Returns?

The Excess Returns model compares what eToro Group earns on its equity with the cost of that equity and then projects how long that gap can persist. For eToro Group, the inputs indicate a relatively rich profitability profile, with an average return on equity of 14.59% applied to a stable book value base of $16.36 per share and a stable EPS estimate of $2.39 per share, both drawn from five-year medians.

Against this, the model uses a cost of equity of $1.55 per share, implying an excess return of $0.84 per share on a stable book value of $16.36 per share. When those excess returns are rolled forward, the intrinsic value indication comes out at $30.53 per share, which is below the current share price and therefore indicates a 29.3% premium. On this framework, the market is currently paying a premium for eToro Group relative to what its excess returns on equity support.

On these Excess Returns assumptions, the stock screens as overvalued relative to its estimated intrinsic value.

Our Excess Returns analysis suggests eToro Group may be overvalued by 29.3%. Discover 43 high quality undervalued stocks or create your own screener to find better value opportunities.

Is eToro Group a Bargain on Earnings?

The P/E ratio is a useful way to see what you are paying for each dollar of eToro Group earnings today. eToro Group trades on a P/E of 13.2x, which is well below the Capital Markets industry average of 39.9x and also below the peer group average of 4.6x implied by Simply Wall St's screening set.

On Simply Wall St's modelled "fair" P/E of 15.7x for eToro Group, the current 13.2x multiple sits at a discount to what would typically be expected given its profile. That suggests the market is applying a modestly cautious earnings multiple even though the stock does not stand out as expensive on sector comparisons.

On the P/E lens, eToro Group appears undervalued relative to the earnings multiple that the fair ratio model indicates.

The eToro Group Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for eToro Group pick up where this valuation puzzle leaves off by spelling out what would need to happen to eToro Group's growth, margins and earnings for the stock to be worth materially more or less than today's price, and they sit on the company’s Community page. Rather than relying on a single multiple or model output, each Narrative lays out its own assumptions for fair value so you can compare them with actual results over time.

If you have a number driven view on where eToro Group's growth, margins and execution go from here, consider adding your own Narrative to the Simply Wall St community and setting out the case behind your outlook.

This is a chance to put your valuation thinking on record, compare it with others' views on eToro Group and see how your thesis holds up as new results arrive.

Do you think there's more to the story for eToro Group? Head over to our Community to see what others are saying!

The Bottom Line

For eToro Group, the Excess Returns intrinsic value estimate points to an overvalued stock, while the earnings multiple view still screens as undervalued. That split mainly reflects different bets on cash flow durability and capital needs on one side, and on how the market prices growth and sentiment on the other. The broader valuation checks are weak, so the supportive P/E signal sits against a more cautious backdrop. The real hinge from here is whether eToro Group can consistently turn its trading activity into resilient earnings and cash flows that justify paying up, rather than the discount simply closing because the multiple re-rates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.