Evaluating Dominion Energy (D) After Offshore Wind Cost Increase And 2027 Completion Delay

Dominion Energy Inc D | 62.77 | +1.16% |

Dominion Energy (D) is in focus after revising the budget and timeline for its Coastal Virginia Offshore Wind project. The project is now estimated at US$11.5b, with full completion targeted for early 2027.

Those offshore wind revisions come as Dominion Energy’s recent news flow has also included a fresh quarterly dividend declaration and a new environmental stewardship agreement along the W&OD Park. The 1-year total shareholder return of 19.27% and 3-year total shareholder return of 15.84% contrast with more muted recent share price returns, hinting that momentum has cooled but longer term holders have still seen gains.

If you are weighing Dominion Energy alongside other utilities and income ideas, it may also be worth scanning healthcare stocks for different defensively positioned businesses with their own catalysts.

With Dominion Energy shares up 19.27% over 1 year and trading only about 3% below a US$63.50 analyst target, the key question is whether current projects justify further upside or whether the market is already fully reflecting future growth in the price.

Most Popular Narrative: 3.2% Undervalued

Dominion Energy closed at $61.43 versus a widely followed fair value estimate of about $63.44. This frames the current pricing as only slightly below that narrative view.

Large-scale investments in regulated renewables, especially the Coastal Virginia Offshore Wind (CVOW) project, position Dominion to benefit from the accelerating energy transition, earning stable regulated returns and expanding rate base, with a positive impact on long-term earnings.

Curious what sits behind that fair value? Revenue growth, rising margins and a recalibrated future earnings multiple all play a part, but the exact mix may surprise you.

Result: Fair Value of $63.44 (UNDERVALUED)

However, those assumptions can break if CVOW costs climb without full regulatory recovery, or if future rate decisions reduce allowed returns and earnings visibility.

Another Take On Valuation

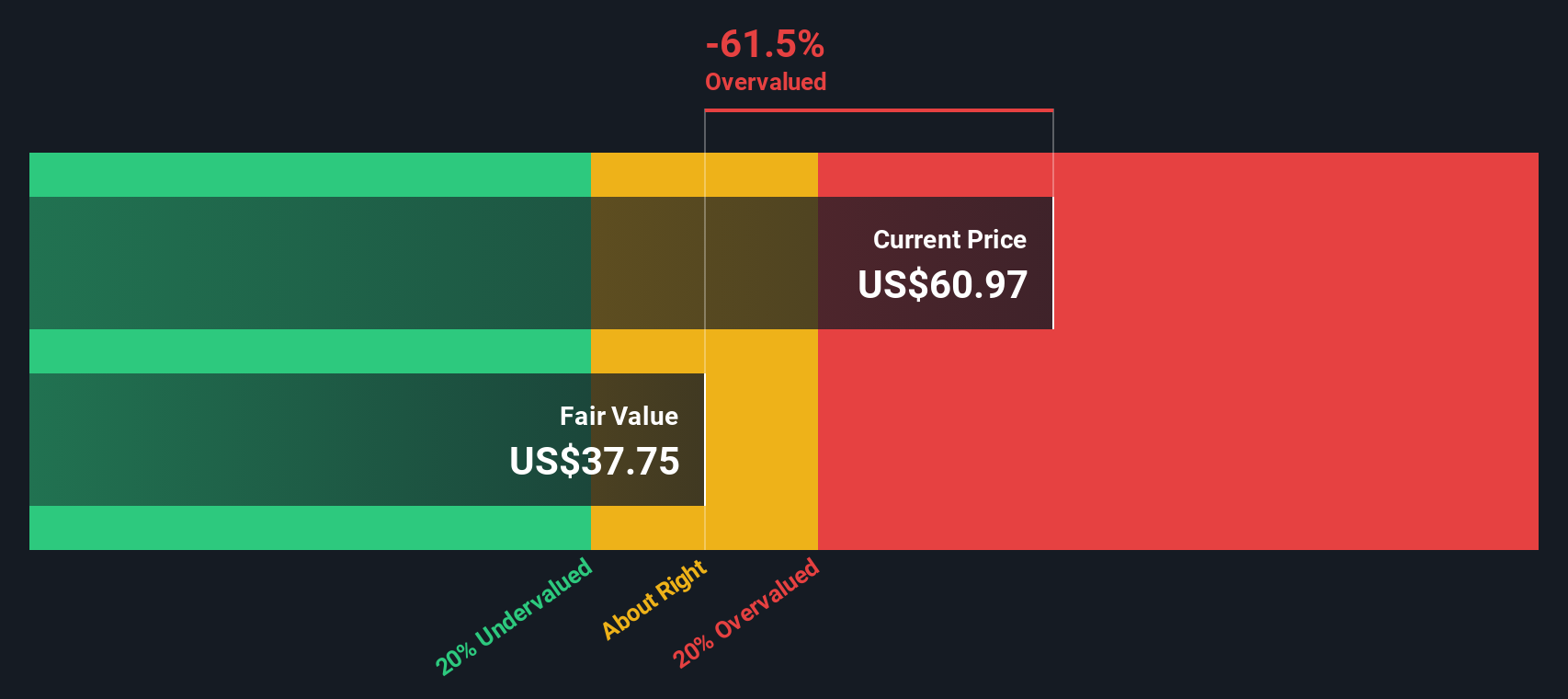

Our DCF model offers a very different perspective compared with the earnings-based fair value. From this standpoint, Dominion Energy at $61.43 is trading well above an estimated future cash flow value of about $36.91, which appears expensive rather than slightly undervalued. That gap raises a simple question: which measure do you consider more informative, earnings or cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dominion Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 873 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Dominion Energy Narrative

If this narrative does not quite match how you see Dominion Energy, you can review the same data yourself and create a custom view in under three minutes: Do it your way.

A great starting point for your Dominion Energy research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Dominion Energy is on your radar, do not stop there. Put a few minutes into scanning other ideas so you are not leaving potential opportunities on the table.

- Spot potential value with these 873 undervalued stocks based on cash flows that highlight companies priced below what their cash flows might suggest.

- Tap into rapidly evolving tech trends by checking out these 25 AI penny stocks that focus on businesses tied to artificial intelligence themes.

- Strengthen your income watchlist by reviewing these 13 dividend stocks with yields > 3% that focus on companies offering dividend yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.