Extended Credit Facility And New CFO Might Change The Case For Investing In Credit Acceptance (CACC)

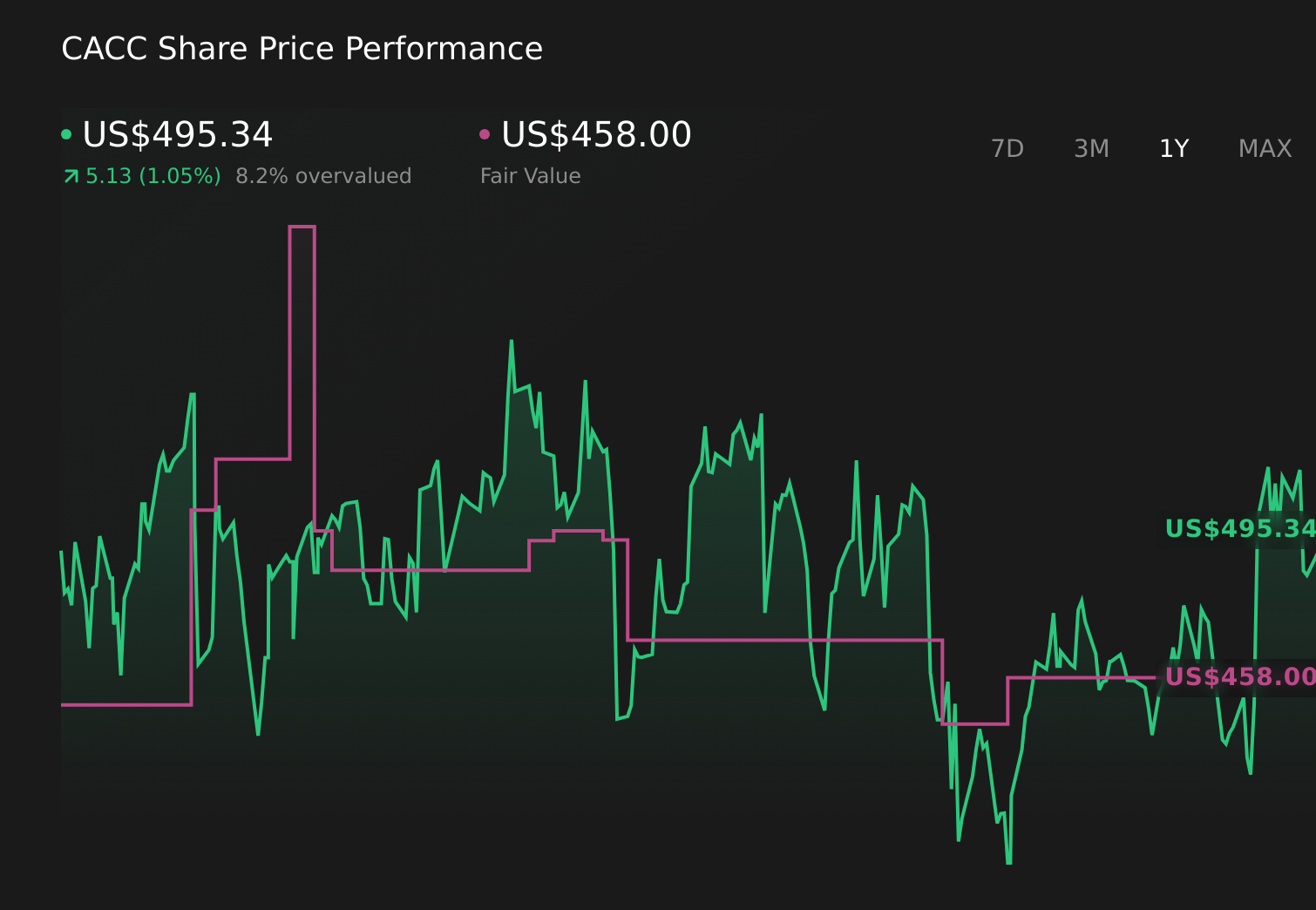

Credit Acceptance Corporation CACC | 0.00 |

- Credit Acceptance recently amended its revolving secured credit facility with Fifth Third Bank and other lenders, extending the facility’s revolving period to June 22, 2029 and lowering the interest rate from SOFR plus 197.5 basis points to SOFR plus 175.0 basis points on the US$270.5 million currently outstanding.

- The company also announced a CFO transition, with long-serving finance chief Jay D. Martin retiring and experienced corporate finance leader Joseph Billante stepping in, potentially influencing how Credit Acceptance manages funding, risk, and communication with investors.

- Next, we’ll examine how the extended, lower-cost credit facility may influence Credit Acceptance’s investment narrative and long-term funding profile.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Credit Acceptance Investment Narrative Recap

To own Credit Acceptance, you need to believe the company can price risk accurately in subprime auto, keep funding costs under control, and protect returns despite competitive pressure and uneven loan performance. The extended, slightly cheaper Fifth Third facility modestly supports that funding story, but does not materially change the key near term catalyst of stabilizing loan performance or the central risk of further credit deterioration.

The interest rate cut on the US$270.5 million revolving facility matters most in the context of Credit Acceptance’s tight spread between return on capital and cost of capital. Lower funding costs can provide a little more room for error if 2022 to 2024 loan vintages continue to strain margins, but the core questions around volumes, competition, and credit quality still sit at the center of the thesis...

Credit Acceptance's narrative projects $3.6 billion revenue and $671.0 million earnings by 2029.

Uncover how Credit Acceptance's forecasts yield a $536.67 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates span roughly US$345 to US$537 per share, highlighting how differently private investors can size Credit Acceptance. You should weigh those views against the risk that weaker 2022 to 2024 loan vintages keep pressuring credit performance and, in turn, the company’s ability to sustain attractive economics over time.

Explore 2 other fair value estimates on Credit Acceptance - why the stock might be worth as much as $536.67!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Credit Acceptance research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Credit Acceptance research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Credit Acceptance's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.