F5 (FFIV) Could Be 13% Undervalued As Equinix Tie Up Tests Valuation

F5, Inc. FFIV | 0.00 |

F5 (FFIV) stock is in focus after the company and Equinix announced a collaboration that combines F5’s AI Guardrails with the Equinix Distributed AI Hub to manage distributed AI across hybrid and multicloud environments.

The F5 share price has climbed 36.87% over the past 90 days and 62.53% year to date, contributing to a 37.93% one year total shareholder return. This reflects strong momentum around its AI security and multicloud story.

If the F5 and Equinix collaboration has your attention, it could be worth seeing what else is moving in AI infrastructure by checking out the 52 AI infrastructure stocks.

After such a sharp run and a fresh AI spotlight on F5, the balance between upside potential and downside risk looks less clear cut. Does the current valuation still leave enough cushion for new buyers?

Most Popular Narrative: 2% Overvalued

F5 last closed at $417.11, slightly above the most followed fair value estimate of $409, so the current price sits just ahead of that narrative.

The ongoing shift to high-margin, recurring software and SaaS subscription revenue, along with strong renewal and expand activity from existing customers, is improving revenue visibility and predictability while supporting operating margin and EPS growth. Effective operational discipline, evident in robust cash flow, continued cost management, and targeted share repurchases, enhances the company's ability to drive EPS growth, maximize shareholder returns, and weather industry cyclicality.

Curious what kind of revenue mix, margin profile, and earnings path need to line up for F5 to justify that fair value and beyond? The full narrative walks through the growth run-rate, profitability assumptions, and future earnings multiple that underpin the $409 figure, and connects them directly to AI security and hybrid multicloud demand.

Result: Fair Value of $409 (OVERVALUED)

However, F5’s story could still be challenged if hardware driven demand fades faster than expected or if competition from hyperscalers and security peers pressures margins.

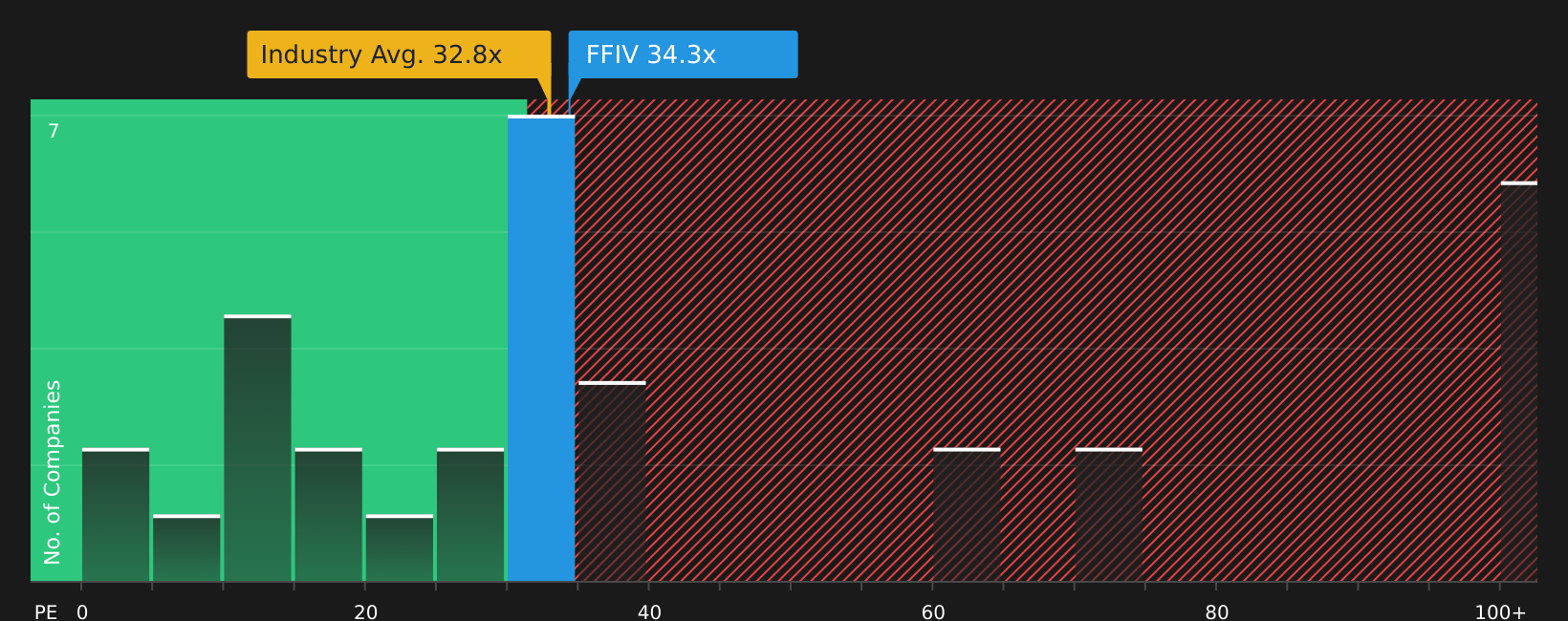

Another View: What F5’s P/E Says About Valuation Risk

The DCF view suggests F5 is trading at a 13% discount to an estimated fair value of $479.57. However, the current P/E of 33.2x sits slightly above the US Communications industry average of 32.4x and above a fair ratio of 28.5x. Is the market already paying up for the AI and multicloud story?

For a closer look at how that earnings multiple compares with peers, and where the fair ratio suggests the market could shift over time, it is worth walking through the detailed valuation breakdown in the See what the numbers say about this price — find out in our valuation breakdown..

Next Steps

If the mixed signals in the F5 story leave you on the fence, it helps to move quickly and test the numbers yourself, then weigh both sides using the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond F5?

F5 may be front of mind today, but some of the best opportunities often sit just outside the spotlight, so do not miss the chance to widen your watchlist.

- Spot potential mispriced opportunities early by scanning companies on the 45 high quality undervalued stocks.

- Prioritise resilience and capital protection by reviewing companies in the 74 resilient stocks with low risk scores.

- Hunt for under-followed potential future leaders using the screener containing 18 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.