FedEx (FDX) Stock May Be A Bargain On Its $1.4B Asset Sale

FedEx Corporation FDX | 0.00 |

FedEx stock has delivered a strong 65.8% return over the past year, and with both the Discounted Cash Flow (DCF) intrinsic value estimate and earnings multiples pointing to undervaluation, the key tension is whether the current price already reflects the benefits of its recent logistics moves and business refocus.

- Over the last 12 months, FedEx has returned 65.8%, which puts fresh attention on whether that share price strength still leaves a margin between market price and estimated intrinsic value.

- The planned US$1.4b sale of FedEx Supply Chain to CMA CGM can support a tighter focus on core express and ground operations. However, execution risks around multi year commercial agreements and reshaping the logistics footprint may affect how reliably cash flows develop.

- FedEx screens as undervalued on both intrinsic value and market multiples, but its valuation checks are mixed, with 4 of 6 tests pointing to the stock as cheaper than its fundamentals might suggest.

The issue now is whether FedEx's recent run up still leaves enough upside in the intrinsic value estimate to justify the current price.

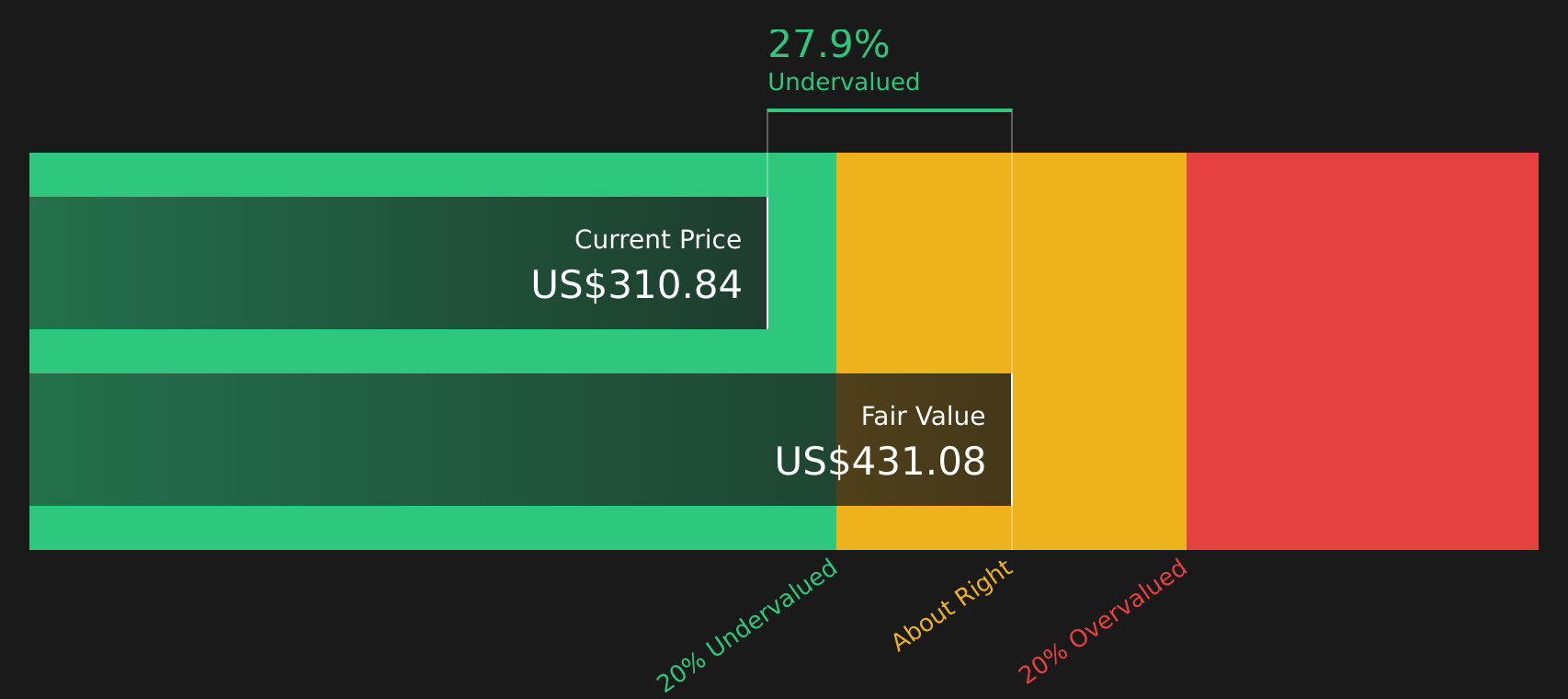

Is FedEx a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) model estimates what FedEx might be worth based on projected future cash generation. For FedEx, the latest twelve month free cash flow sits at about $4.4b, and the model assumes those cash flows continue growing rather than shrinking. On that basis, the 2 Stage Free Cash Flow to Equity approach points to an intrinsic value of about $431 per share.

Compared with the current share price, that DCF estimate implies the stock trades at roughly a 28.2% discount, so the market price sits well below what the cash flow projections support. Because the planned $1.4b sale of FedEx Supply Chain to CMA CGM refocuses FedEx on its core express and ground operations, the current discount suggests investors may not be fully pricing in the cash flows associated with that tighter core footprint.

On this cash flow view, FedEx stock currently appears undervalued relative to its estimated intrinsic worth.

Our Discounted Cash Flow (DCF) analysis suggests FedEx is undervalued by 28.2%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Does FedEx Look Undervalued on Earnings?

P/E is a useful check for FedEx because earnings are a core driver for how investors typically compare large, established logistics companies. FedEx currently trades on a P/E of about 16.7x, which sits slightly above the logistics industry average of 15.3x but below the peer group average of 23.5x for larger cargo and transport companies.

Based on a tailored fair P/E of 23.0x, which reflects FedEx's size, margins, industry and risk profile, the current 16.7x suggests the stock trades at a discount to where this framework would place it. That gap indicates the market is valuing FedEx more cautiously than similar peers with comparable fundamentals, even after the recent refocus on core express and ground operations.

On earnings, FedEx stock appears undervalued, with its current P/E sitting well below the level implied by its fair multiple.

The FedEx Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for FedEx pick up from that valuation gap and spell out which assumptions about FedEx's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price. These Narratives are available on Simply Wall St's Community page. Each Narrative treats its fair value as a thesis you can track over time, framing it as something that can either be supported or challenged as FedEx's business develops.

FedEx investors are weighing two very different storylines, with community views split between a cost driven margin rebuild and a tougher long term parcel outlook.

Bull case: 23% undervalued

"FedEx's DRIVE initiative is achieving significant cost savings, with a target of $2.2 billion for FY '25 and a total of $4 billion compared to the FY '23 baseline..."

Bear case: 40% overvalued

"Structural declines in parcel volumes, rising labor and environmental costs, and intensifying price competition threaten long-term revenue growth and margin sustainability..."

Do you think there's more to the story for FedEx? Head over to our Community to see what others are saying!

The Bottom Line

FedEx looks undervalued on both the Discounted Cash Flow (DCF) intrinsic value estimate and its P/E multiple, although broader valuation checks are mixed rather than overwhelmingly strong. The key question is whether that discount reflects genuine underappreciation of its refocused express and ground operations or a fair cushion for execution and parcel demand risks. For investors, the crux is whether FedEx can sustain and convert its cost and efficiency efforts into reliable cash flows and margins, which would be needed for today’s apparent discount to close rather than turn into a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.