Figs Stock And Two Apparel Plays For A Bangladesh Tariff Shift

FIGS, Inc. Class A FIGS | 0.00 |

The proposed 10% U.S. tariff on Bangladeshi garment imports is more than a trade headline; it is a potential reshuffle of where margins are squeezed or protected across U.S. apparel and retail stocks. For investors watching supply chains and sourcing costs, this kind of policy shock can quickly separate potential winners from those facing pressure. This article highlights 3 U.S. apparel and retail stocks from our screener that appear positively exposed to this news, helping you think through where resilience, pricing power, or reduced reliance on Bangladesh could matter most as the tariff debate unfolds.

J.Jill (JILL)

Overview: J.Jill is a U.S. womenswear retailer focused on customers aged 40+, selling apparel, footwear and accessories under the J.Jill, Pure Jill, Wearever and Fit brands through its stores, catalog and ecommerce platform.

Operations: J.Jill generates about US$587.4 million in revenue from its Retail and Direct Channels, all from the United States.

Market Cap: US$221.1 million

J.Jill stands out in this tariff story because it is already leaning into omnichannel retail and a tightly defined U.S. customer base, while working to cut exposure to higher risk sourcing countries and use vendor negotiations, on order adjustments and selective price increases to offset higher duties. Earnings took a step back in 2025 and Q1 2026, and guidance points to softer sales and some margin pressure, so this is not a straight-line growth story. For investors watching how apparel companies handle supply chain stress, J.Jill offers a mix of tariff risk, mitigation efforts and the possibility of a re-rating if execution holds up.

J.Jill’s tariff playbook, from vendor talks to selective pricing moves, could be masking a much bigger story about its earnings power under stress. Get the full picture in the analysis report for J.Jill

FIGS (FIGS)

Overview: FIGS is a healthcare apparel company that designs and sells premium scrubs and related clothing, footwear and accessories for medical professionals through its direct-to-consumer website, app, B2B channel and a growing retail presence in the U.S. and abroad.

Operations: FIGS generates about US$666.1 million in revenue from online retail, with roughly US$553.0 million from the United States and US$113.1 million from the rest of the world.

Market Cap: US$2.0b

FIGS sits in a niche that could become more interesting as the U.S. looks harder at low cost garment imports, because it is a direct-to-consumer healthcare brand with a focus on quality, fit and style rather than being a volume importer fighting on price. Earnings have recently improved and margins are supported by its e-commerce model and premium positioning, yet a high P/E of 50.5x and reliance on external funding keep expectations and balance sheet risk elevated. If tariffs lift costs for rivals more exposed to Bangladesh and other sourcing hubs, FIGS’ brand strength, TEAMS program and international expansion could become more significant, but the valuation leaves less room for disappointment.

FIGS’ premium scrubs story is all about whether a 50.5x P/E, strong brand and tariff tailwinds still leave upside on the table, and the analyst forecasts for FIGS quietly hints at where expectations might be wrong.

Zumiez (ZUMZ)

Overview: Zumiez is a youth focused specialty retailer selling apparel, footwear, accessories and action sports hardgoods like skateboards and snowboards through its Zumiez, Blue Tomato and Fast Times banners across North America, Europe, Australia and online.

Operations: Zumiez generates about US$938.1 million in revenue primarily from apparel retail, with roughly US$713.1 million from the United States and the balance from Canada, Europe and Australia.

Market Cap: US$292.1 million

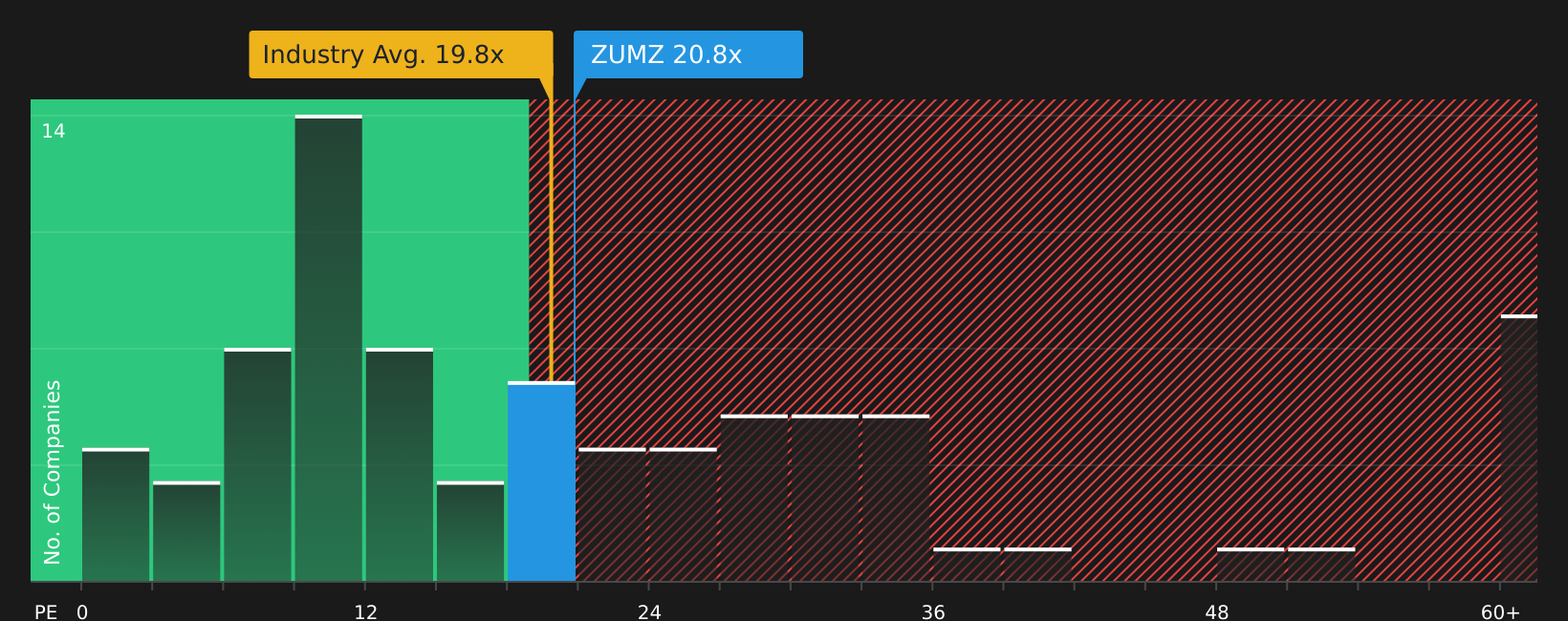

Zumiez sits at an interesting crossroads for this tariff story because it already leans on North American sourcing and brand led assortments for young consumers. As a result, a 10% U.S. tariff on Bangladeshi garments could squeeze some competitors harder than a retailer that is actively diversifying production and spreading risk across suppliers. At the same time, Zumiez is still working through losses, modest 1.5% margins and soft international performance, while the stock trades on a P/E above both its estimated fair multiple and the sector average. For investors, the mix of fast growing private label, digital engagement and supply chain recalibration under tariff pressure is where the real opportunity and risk in Zumiez start to show.

Zumiez’s fast growing private label and youth focused brand story could be masking how tariffs and its above sector P/E really interact, and the analyst forecasts for Zumiez may reveal what the market is still missing

The three apparel and retail stocks covered here are only a starting point. Our full U.S. Domestic Apparel and Retail Stocks screener highlights 24 more companies that carry equally compelling stories around sourcing, margins and industry positioning through the U.S. Domestic Apparel and Retail Stocks screener. Use Simply Wall St to analyze that wider group, filter for the catalysts and narratives that matter most to you, and identify the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If FIGS or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Apparel?

New stock ideas can move from quiet to breakout before most investors even notice. Scan fresh opportunities while they are still under the radar for now and consider them carefully.

- Spot potential trendsetters early by reviewing the curated 20 high quality undiscovered gems before momentum builds and the most attractive entry points may no longer be available.

- Target cash generative opportunities with the hand picked 48 high quality undervalued stocks before stronger earnings and sentiment are fully reflected in the share price.

- Focus on durability first by checking the carefully filtered list of solid balance sheet and fundamentals (48 results) while these financially steady companies are still priced as if they are ordinary.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.