First Advantage (FA) Beats On Earnings And Joins S&P SmallCap 600, Is The Upside Priced In?

First Advantage Corp. FA | 0.00 |

First Advantage (FA) drew fresh attention after reporting Q1 2026 earnings that surpassed analyst expectations, along with confirmation it will join the S&P SmallCap 600 index, a combination that put recent share gains into focus.

Over the past year, First Advantage has seen strong momentum, with the share price delivering a 68.25% 90 day return and a 32.60% year to date share price return, while the 1 year total shareholder return stands at 11.41%.

If you are looking beyond First Advantage and want more ideas, this could be a good moment to see which companies feature in our 20 top founder-led companies

After a 52 week high, strong recent returns and a fresh index inclusion, First Advantage looks very different to where it sat a year ago. So is the stock still undervalued, or is the market already pricing in its future growth?

Most Popular Narrative: 4.1% Overvalued

The most followed narrative on First Advantage currently points to a fair value of $18.14, which sits slightly below the latest close at $18.90. This places recent gains and the S&P SmallCap 600 inclusion side by side with more measured expectations.

Ongoing investments in proprietary AI enabled technology, automation, and integrated platforms (particularly following the Sterling acquisition) are unlocking operational efficiencies and enabling more high margin value added services, creating potential for margin expansion and higher net earnings.

Want to see what sits behind that margin story? The core of this narrative is a detailed blend of revenue growth, rising profitability, and a tighter earnings multiple that together justify the current fair value path without relying on blue sky assumptions.

Result: Fair Value of $18.14 (OVERVALUED)

However, First Advantage still faces pressure from hiring slowdowns and intense competition. Either factor could weigh on revenue stability and profit margins if conditions worsen.

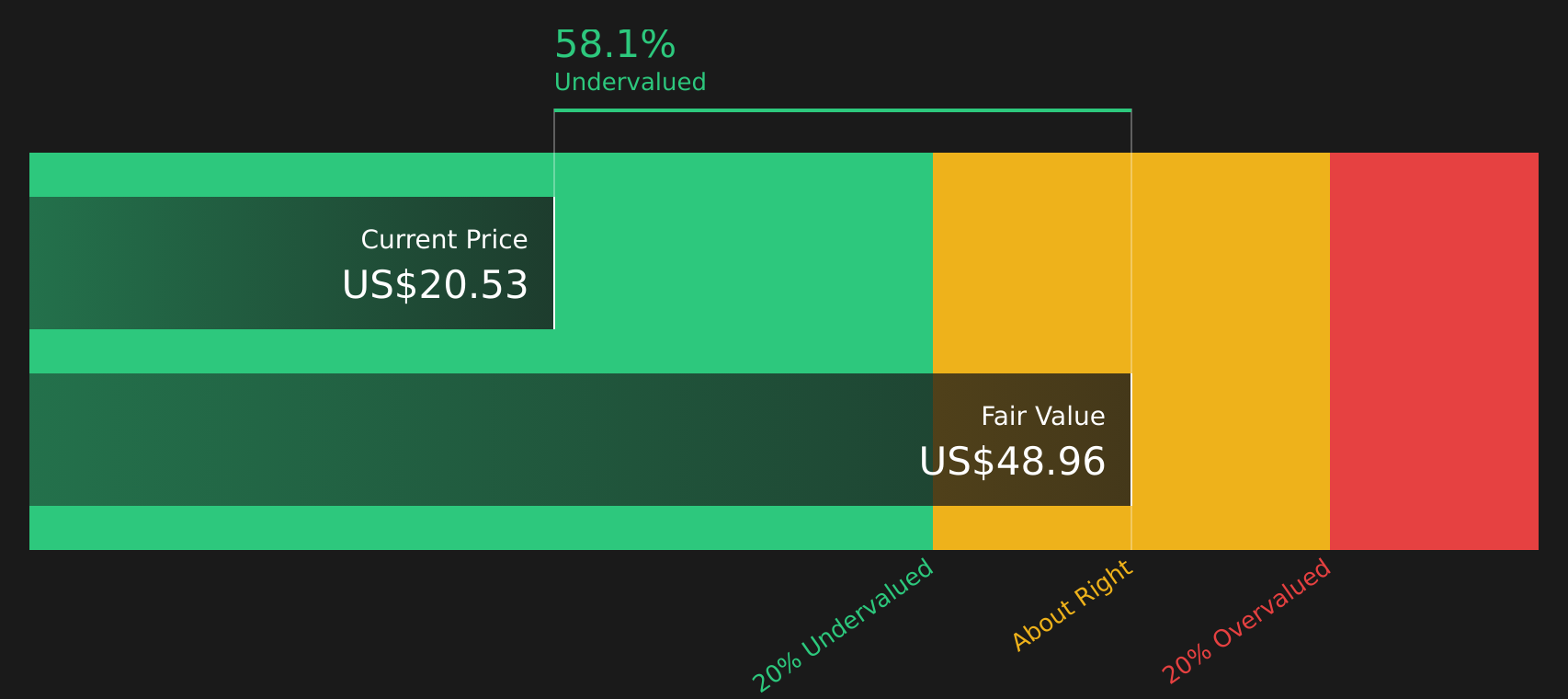

Another View: First Advantage Through The DCF Lens

While analysts see First Advantage as about 4.1% overvalued relative to their $18.14 fair value estimate, the Simply Wall St DCF model paints a very different picture, with a fair value of $48.02. At a last close of $18.90, the stock trades about 60.7% below that DCF estimate, which raises a clear question: which set of assumptions do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out First Advantage for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals, with both risks and rewards on the table for First Advantage, make this a moment to look at the underlying data yourself, weigh the upside and downside, and see whether the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond First Advantage?

If you are weighing First Advantage, this is also a moment to widen your watchlist with other stocks that share strong fundamentals, resilient balance sheets, or compelling income profiles.

- Spot potential bargains with resilient earnings and healthy cash flows by checking companies in the 41 high quality undervalued stocks

- Prioritise sleep at night holdings by reviewing stocks highlighted in the 73 resilient stocks with low risk scores

- Strengthen your income stream by scanning for companies in the 8 dividend fortresses

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.