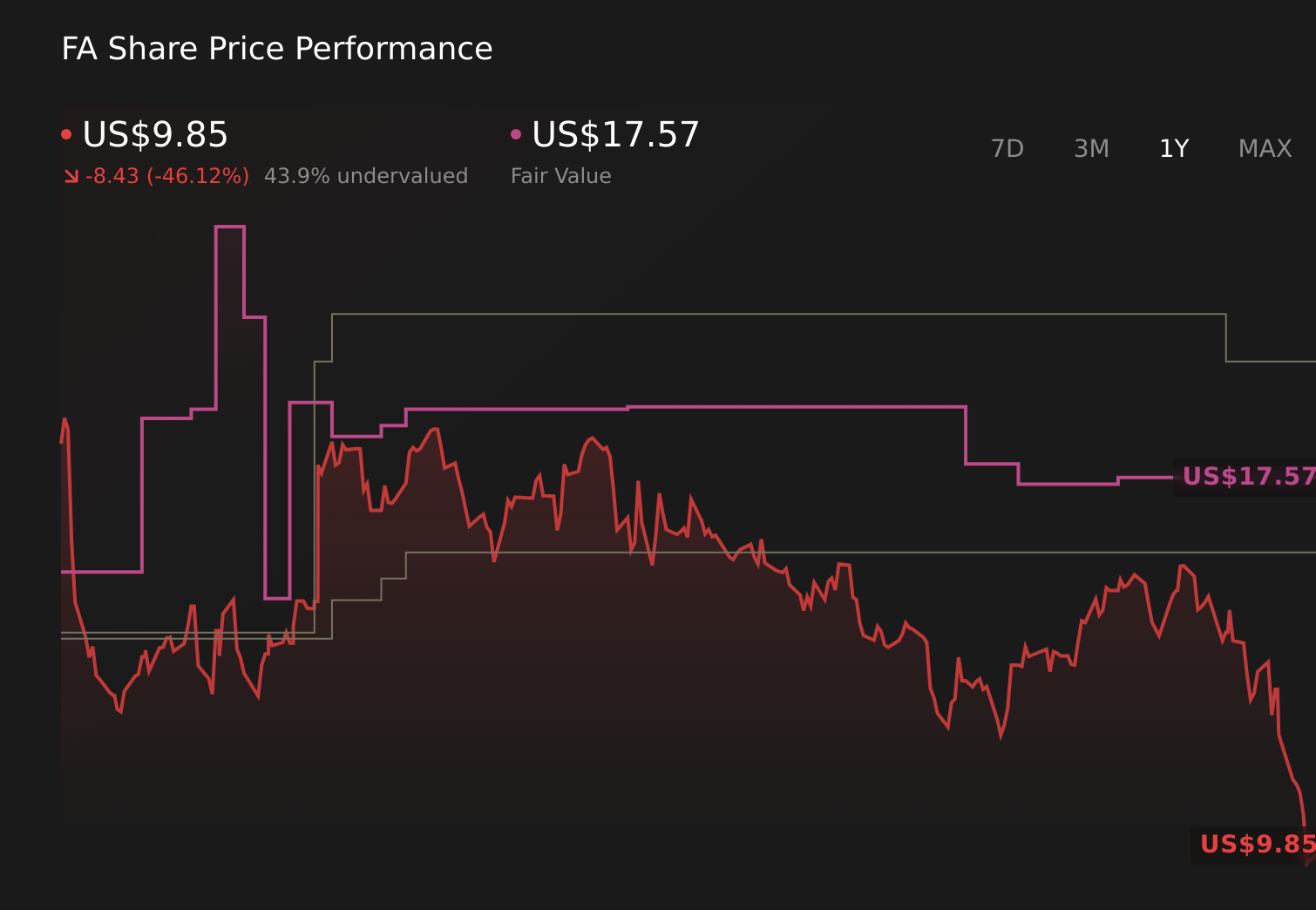

ارتفعت أسهم شركة فيرست أدفانتج (FA) بنسبة 26.7% بعد تحقيقها أرباحًا في الربع الأول وتأكيد توقعاتها لعام 2026

First Advantage Corp. FA | 0.00 |

- أعلنت شركة First Advantage Corporation عن نتائج الربع الأول من عام 2026 بإيرادات بلغت 385.2 مليون دولار أمريكي، محولة بذلك خسارة العام الماضي البالغة 41.19 مليون دولار أمريكي إلى ربح صافٍ قدره 2.17 مليون دولار أمريكي، ومحققة أرباحًا أعلى بقليل من نقطة التعادل.

- كما أكدت الشركة توقعاتها لإيرادات عام 2026 والتي تتراوح بين 1.63 مليار دولار أمريكي و1.70 مليار دولار أمريكي، مع التركيز على الاحتفاظ بالعملاء بشكل كبير، والتوسع الدولي، وعمليات إعادة شراء الأسهم المستمرة وخفض الديون.

- بعد ذلك، سندرس كيف تؤثر التوجيهات المؤكدة لعام 2026 وتحسين الربحية على سردية الاستثمار الحالية لشركة First Advantage وتوقعاتها المستقبلية.

هذه التقنية قد تحل محل أجهزة الكمبيوتر: اكتشف 26 شركة تعمل على جعل الحوسبة الكمومية حقيقة واقعة .

ملخص سرد استثمار فيرست أدفانتج

لامتلاك أسهم شركة First Advantage، يجب أن تؤمن بأن ارتفاع معدل الاحتفاظ بالعملاء، وتزايد الطلب على خدمات الفحص، ومنصتها المتكاملة، كلها عوامل تُسهم في تحقيق ربحية أكثر استقرارًا على المدى الطويل. ويتمثل العامل الرئيسي المحفز على المدى القريب في قدرة الإدارة على تحويل نمو الإيرادات الأخير إلى أرباح ثابتة، بينما يبقى التحدي الأكبر هو الضغط على حجم التوظيف والتسعير في سوق مجزأة. ويؤكد الربع الأخير تحسن الربحية، ولكنه لا يُغير جوهريًا من تلك العوامل أو المخاطر الأساسية.

في هذا السياق، تكتسب التوقعات المؤكدة لإيرادات عام 2026، والتي تتراوح بين 1.63 مليار دولار أمريكي و1.70 مليار دولار أمريكي، أهمية خاصة. فهي ترتبط ارتباطًا مباشرًا بالعامل المحفز الرئيسي المتمثل في تحويل التوسع الدولي والعلاقات المؤسسية القوية إلى أداء مالي مستقر يمكن التنبؤ به، في حين أن عمليات إعادة شراء الأسهم المستمرة وخفض الديون تُبرز تركيز الإدارة على إدارة رأس المال بكفاءة في ظل سعيها للتغلب على ضغوط التكامل والهوامش الربحية.

ومع ذلك، حتى مع بقاء التوجيهات سارية، ينبغي على المستثمرين مراقبة كيف يمكن أن تؤدي الأسعار التنافسية وأحجام التوظيف إلى الضغط فجأة على هوامش الربح والتدفق النقدي...

تتوقع شركة First Advantage تحقيق إيرادات بقيمة 1.9 مليار دولار وأرباح بقيمة 168.3 مليون دولار بحلول عام 2029. ويتطلب ذلك نموًا سنويًا في الإيرادات بنسبة 7.1٪ وزيادة في الأرباح بمقدار 203.1 مليون دولار من -34.8 مليون دولار اليوم.

اكتشف كيف أن توقعات شركة First Advantage تؤدي إلى قيمة عادلة قدرها 15.00 دولارًا ، أي بانخفاض قدره 6٪ عن سعرها الحالي.

استكشاف وجهات نظر أخرى

افترض بعض المحللين ذوي التصنيف الأدنى إيرادات تبلغ حوالي ملياري دولار أمريكي وأرباحًا تبلغ 169.8 مليون دولار أمريكي بحلول عام 2029، وهو تقدير أكثر تحفظًا بكثير من التوقعات السائدة. عند مقارنة هذه التوقعات مع أرباح الربع الأخير المتواضعة والتوقعات المؤكدة، يتضح مدى اختلاف تقييم المخاطر، مثل انخفاض هوامش الربح في أعمال الجنيه الإسترليني، مقابل الفوائد المحتملة لخفض التكاليف وتحسينات التكنولوجيا، ولماذا قد يكون من المفيد دراسة وجهات نظر متعددة قبل اتخاذ القرار.

استكشف تقديرًا آخر للقيمة العادلة لشركة First Advantage - لماذا قد تكون قيمة السهم أقل بنسبة 6٪ من السعر الحالي!

القرار لك

هل تخالف الروايات السائدة؟ نادراً ما تأتي عوائد الاستثمار الاستثنائية من اتباع القطيع، لذا اتبع حدسك.

- تُعد تحليلاتنا التي تسلط الضوء على 3 مكافآت رئيسية و3 علامات تحذيرية مهمة قد تؤثر على قرارك الاستثماري نقطة انطلاق رائعة لأبحاثك حول First Advantage.

- يقدم تقريرنا البحثي المجاني لشركة First Advantage تحليلاً أساسياً شاملاً مُلخصاً في شكل مرئي واحد - ندفة الثلج - مما يسهل تقييم الصحة المالية العامة لشركة First Advantage بنظرة سريعة.

هل تفكر في استراتيجيات أخرى؟

تكشف عمليات المسح اليومية لدينا عن أسهم ذات إمكانات نمو هائلة. لا تفوّت هذه الفرصة:

- استغل دورة البنية التحتية للذكاء الاصطناعي الفائقة من خلال اختيارنا لأفضل 38 "خيارًا وأداة" في طفرة الذكاء الاصطناعي التي تحول الطلب القياسي إلى تدفق نقدي هائل.

- استثمر في النهضة النووية من خلال قائمتنا التي تضم 91 مشروعاً رائداً في مجال البنية التحتية للطاقة النووية، والتي تدعم ثورة الذكاء الاصطناعي العالمية.

- تُعدّ المعادن الأرضية النادرة عنصرًا أساسيًا في معظم الأجهزة عالية التقنية، والأنظمة العسكرية والدفاعية، والمركبات الكهربائية. ويتنافس العالم بشدة لتأمين إمدادات هذه المعادن الحيوية. اكتشف أفضل 33 شركة في مجال المعادن الأرضية النادرة، من بين الشركات القليلة التي تستخرج هذا المورد الاستراتيجي المهم.

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.