FirstSun Capital Bancorp (FSUN) Stock Could Be 21.3% Undervalued After Stronger Results

FirstSun Capital Bancorp FSUN | 0.00 |

Recent commentary on FirstSun Capital Bancorp (FSUN) has focused on stronger year-over-year revenue and net profit figures, along with generally supportive analyst sentiment. This has prompted fresh attention on how the stock reflects these fundamentals.

At a share price of $36.19, FirstSun Capital Bancorp has seen its 1 year total shareholder return of 8.55% and 3 year total shareholder return of 44.76% contrast with a year to date share price decline of 4.28%, suggesting longer term holders have fared better than more recent buyers.

If you are weighing FirstSun Capital Bancorp alongside other opportunities in financials and beyond, this could be a good moment to broaden your search and uncover 20 top founder-led companies

So with FirstSun Capital Bancorp trading at $36.19 and analyst targets closer to $43, is the stock offering you a margin of safety today, or is the market already pricing in all of its future growth potential?

Most Popular Narrative: 21.3% Undervalued

On the most followed narrative, FirstSun Capital Bancorp’s fair value of $46 sits clearly above the current $36.19 share price, putting the spotlight on how growth, margins and risk assumptions fit together in that gap.

The bank's commitment to a relationship-driven business model and ongoing enhancement of fee-based service offerings (with fee income now exceeding 25% of total revenues) enables FirstSun to leverage rising demand among younger demographics for innovative, convenient banking solutions, supporting higher non-interest income and improved net margins.

Want to see what sits behind that fair value? Revenue projections, margin expansion and future earnings multiples are all baked into this story, but the exact mix may surprise you.

In this narrative, analysts tie a higher present-day value to a specific path for revenue growth, profitability and future earnings, all discounted back using a 6.978% rate to arrive at a fair value of $46. They then compare that to the current price around $36 to argue there is a gap that only closes if those revenue, margin and valuation multiple assumptions hold over time.

Result: Fair Value of $46 (UNDERVALUED)

However, this FirstSun Capital Bancorp narrative can be challenged if recent deposit inflows reverse, or if elevated commercial loan charge offs persist and pressure margins.

Another View: How FirstSun Capital Bancorp Looks On Earnings Multiples

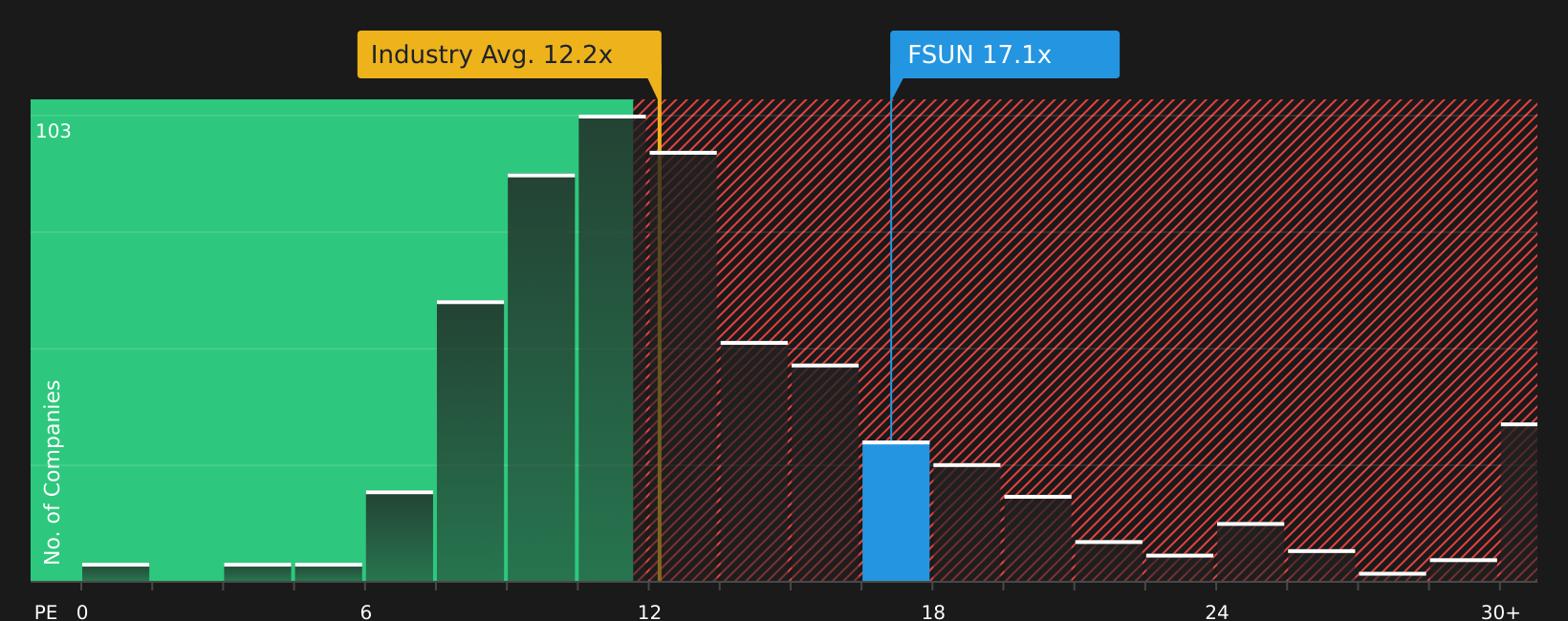

The SWS DCF model presents FirstSun Capital Bancorp as deeply undervalued, with a fair value estimate of $87.85 versus the current $36.19 price. Yet on a simple P/E basis, the stock appears expensive at 17.6x earnings compared with 14.6x for peers and 11.9x for the wider US banks industry. The fair ratio of 25.4x indicates a level the market might reach if sentiment and fundamentals align. With such a wide spread between cash flow value and earnings multiples, which signal should be treated as more important?

To see how these earnings based signals compare with other checks, review the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly mixed around FirstSun Capital Bancorp, use this as a prompt to move fast, review the details for yourself, and weigh 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond FirstSun Capital Bancorp?

Do not stop with FirstSun Capital Bancorp. Broaden your watchlist now with fresh ideas picked using the Simply Wall St Screener and avoid missing opportunities entirely.

- Target companies with strong income potential by reviewing the 8 dividend fortresses, which may appeal if you prioritize regular cash returns over pure price growth.

- Focus on value opportunities and compare FirstSun Capital Bancorp with the screener containing 19 high quality undiscovered gems, which may not yet be widely followed by the market.

- Prioritize resilience by weighing FirstSun Capital Bancorp against the 65 resilient stocks with low risk scores if capital protection sits high on your list.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.