Following Russell 2000 Removal, Is Myers Industries (MYE) Now Fully Valued?

Myers Industries, Inc. MYE | 0.00 |

Myers Industries (MYE) was recently removed from the Russell 2000 Dynamic Index. This index change can affect trading flows as passive funds adjust their holdings to match the new composition.

At a share price of $31.54, Myers Industries has seen a sharp 1-day share price decline of 7.45% around the index removal. However, its 1-year total shareholder return of 108.69% and 69.48% year-to-date share price return indicate momentum that has been strong over the longer stretch.

If index changes have you looking beyond a single stock, this is a good moment to broaden your search with 20 top founder-led companies

So with Myers Industries still showing a large implied discount to one valuation estimate and trading below an analyst price target, is the recent pullback a chance to buy, or is the market already pricing in future growth?

Most Popular Narrative: 21.3% Overvalued

At a last close of $31.54 versus a narrative fair value of $26.00 based on a 7.19% discount rate, Myers Industries is framed as pricing in more than this most followed model supports.

The simplification of the business portfolio through the strategic review and potential divestiture of the Myers Tire Supply (MTS) business will allow Myers to focus resources and capital on its core segments that are better positioned to benefit from the long-term expansion of reusable industrial packaging and infrastructure solutions, underpinning accelerated revenue growth and enhanced operating margin.

Curious what this focused portfolio needs to deliver to justify that fair value? The narrative leans heavily on earnings power, richer margins, and a lower future earnings multiple than many peers.

Result: Fair Value of $26 (OVERVALUED)

However, Myers Industries still faces softer demand in key end markets and pressure on margins in its Distribution segment, which could limit the earnings improvement this narrative assumes.

Another View: Myers Industries Through a Cash Flow Lens

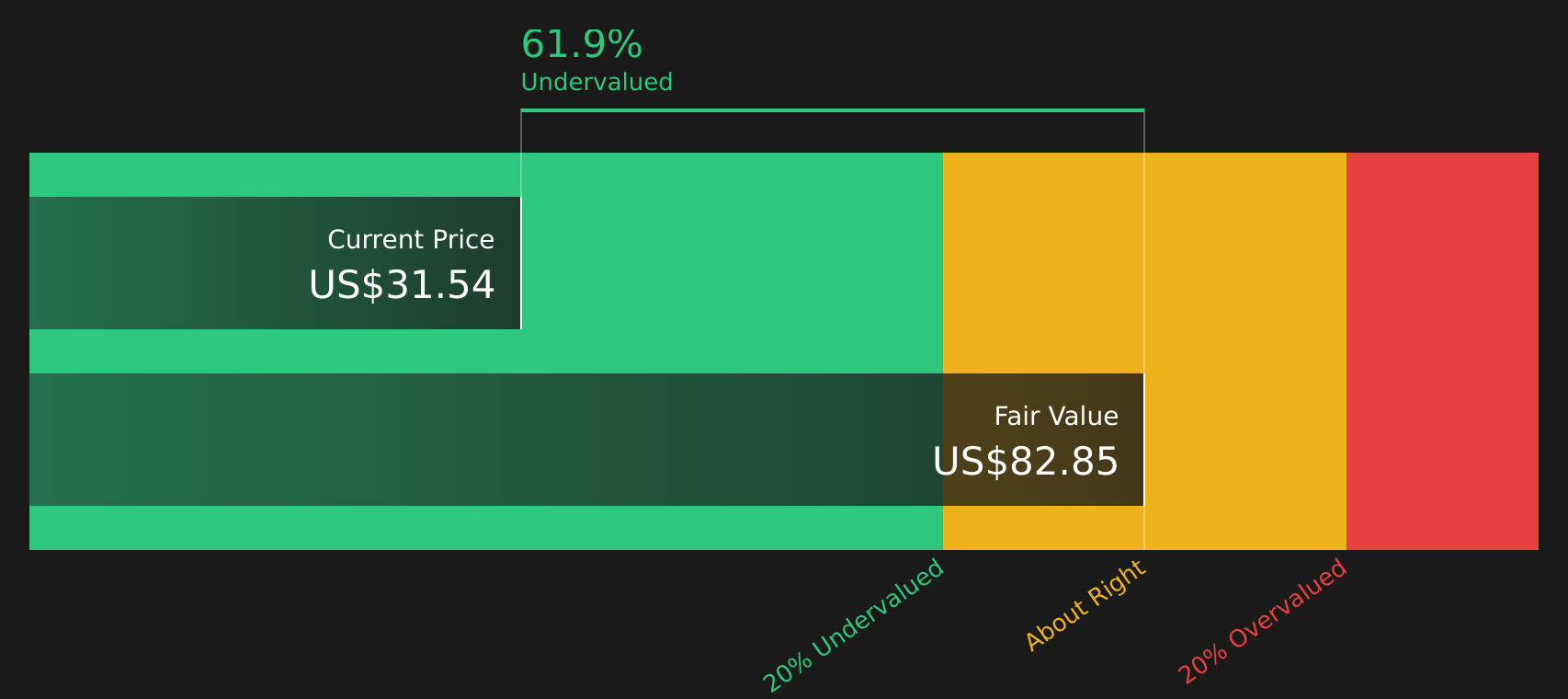

While the most followed narrative frames Myers Industries as 21.3% overvalued at $31.54 versus a $26.00 fair value, our DCF model presents a different perspective. On this approach, the stock trades at a 61.9% discount to an $82.85 future cash flow value, raising the question of which story deserves more weight.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Myers Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around Myers Industries and its valuation, it helps to move quickly, examine the data first hand, and compare the potential upside with the concerns captured in 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond Myers Industries?

If Myers Industries has sharpened your focus on valuation and risk, do not stop here, broaden your watchlist now and keep your options wide open.

Use these tailored Simply Wall St screeners to uncover stocks that match what you are really looking for before the next opportunity moves without you:

- Target potential bargains by scanning companies that combine quality metrics with attractive pricing through the 44 high quality undervalued stocks.

- Prioritise resilience by checking out the 74 resilient stocks with low risk scores to find stocks with lower risk scores that may better fit a cautious approach.

- Spot early-stage potential by reviewing the 20 elite penny stocks with strong financials that pair smaller market caps with stronger financial traits than many peers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.