FTAI Aviation (FTAI) Is Up 9.2% After Raising Dividend And Expanding Credit Facility - What's Changed

FTAI Aviation Ltd. FTAI | 0.00 |

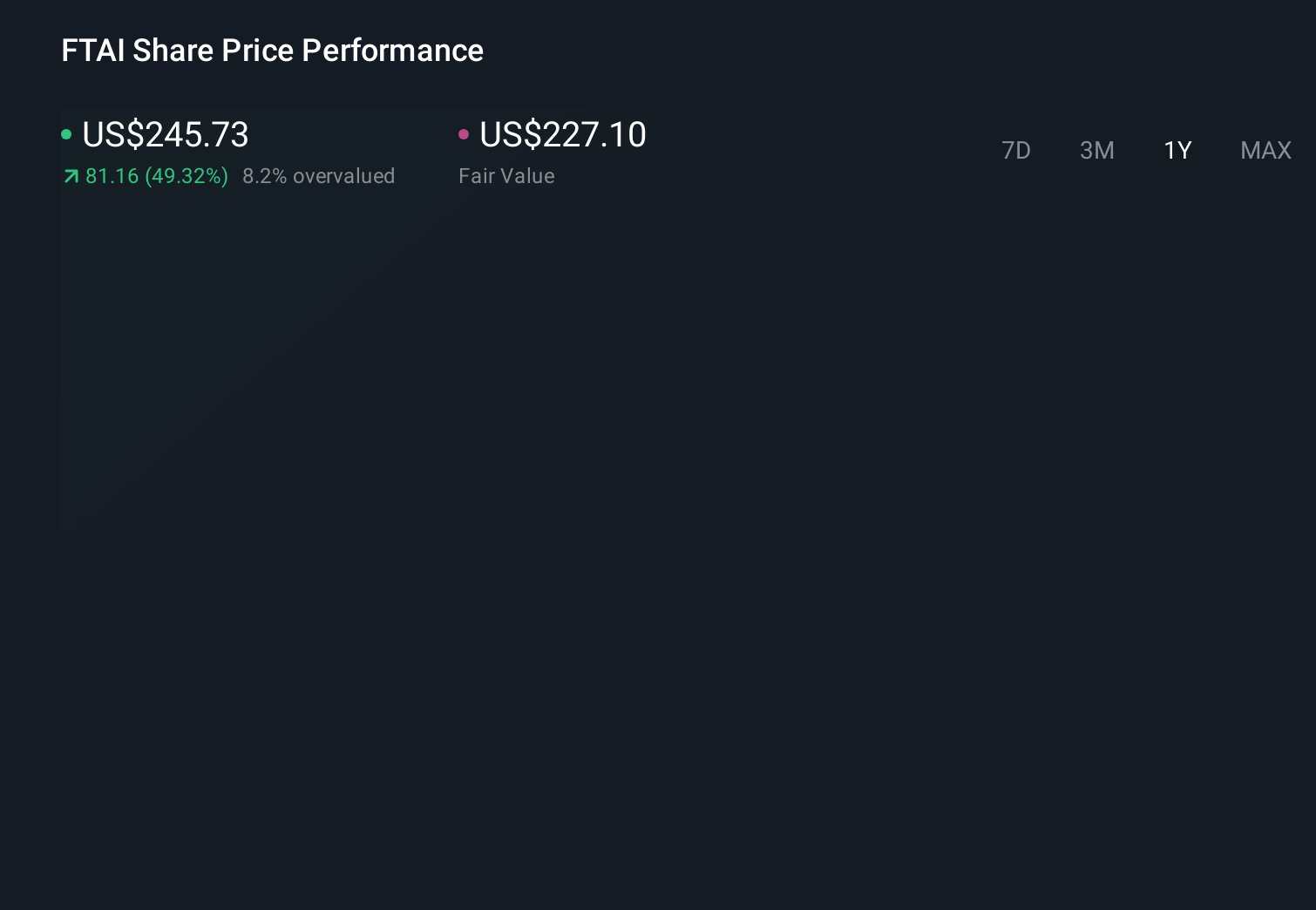

- In late April 2026, FTAI Aviation Ltd. reported first-quarter results showing revenue of US$830.70 million and net income of US$137.90 million, alongside an increased quarterly ordinary dividend of US$0.45 per share and an expanded revolving credit facility with total commitments of US$2.03 billion.

- By pairing stronger quarterly profitability with higher common and preferred dividends and substantially greater lending capacity, FTAI signaled confidence in its balance sheet flexibility and its ability to fund future aviation engine maintenance and leasing opportunities.

- We will now examine how the expanded revolving credit facility reshapes FTAI Aviation's existing investment narrative and risk-reward trade-off.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

FTAI Aviation Investment Narrative Recap

To own FTAI Aviation, you have to believe the mid life engine aftermarket for platforms like the CFM56 and V2500 will stay busy enough to support its asset light, capital hungry model. Right now, the most important near term catalyst is continued uptake of its Maintenance, Repair and Exchange programs, while the biggest risk is concentration in a few legacy engine families. The larger credit facility and higher dividend do not materially change those fundamentals in the short term.

The most relevant recent announcement is the expanded revolving credit facility to US$2.03 billion in commitments. That extra lending capacity, together with improved borrowing terms, directly supports FTAI’s ability to pre fund engine purchases, modules and parts for its MRE and SCI platforms, which sit at the heart of the current growth story and are central to whether the bullish revenue and earnings forecasts can be reached.

Yet even with this stronger balance sheet, investors should still be aware of how exposed FTAI is if demand for legacy engines...

FTAI Aviation's narrative projects $6.4 billion revenue and $1.7 billion earnings by 2029. This requires 31.2% yearly revenue growth and about a $1.2 billion earnings increase from $521.7 million today.

Uncover how FTAI Aviation's forecasts yield a $338.90 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were already penciling in US$4.3 billion of revenue and US$1.3 billion of earnings by 2028, which is far more bullish than the consensus view on risks around legacy engine dependence and OEM competition. With the facility now at US$2.03 billion, you need to decide whether those higher expectations feel more realistic or stretched and consider how your own outlook might differ from both narratives.

Explore 5 other fair value estimates on FTAI Aviation - why the stock might be worth as much as 30% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your FTAI Aviation research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free FTAI Aviation research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FTAI Aviation's overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are the new gold rush. Find out which 33 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.