Garmin (GRMN) Valuation Check After Q1 Earnings Beat And Steady Full Year Guidance

Garmin Ltd. GRMN | 0.00 |

Garmin (GRMN) is back in focus after first quarter revenue of US$1.75b and net income of US$405.08m modestly surpassed analyst expectations, while the company maintained full year 2026 revenue guidance of about US$7.9b.

The share price has eased in the past week, with a 7 day share price return of a 3.68% decline, but momentum over longer horizons remains strong, with a 90 day share price return of 19.56% and a 3 year total shareholder return of about 14.7x.

If Garmin’s mix of consumer electronics, aviation and audio products has you thinking more broadly about opportunities, this could be a good moment to check out 18 top founder-led companies

With Garmin stock up about 19.6% over 90 days and trading roughly 8% below one major analyst target while its own intrinsic estimate implies a small premium, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

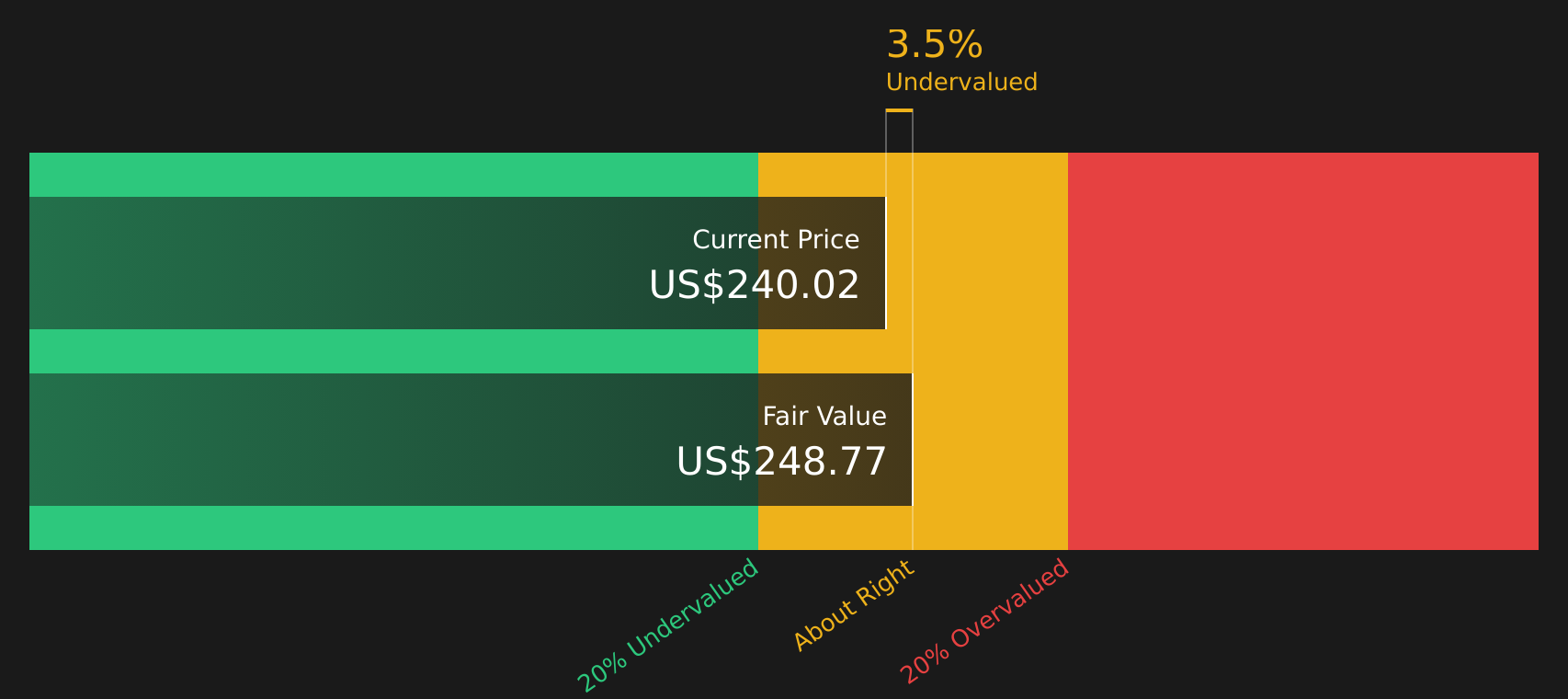

Most Popular Narrative: 7.1% Undervalued

Garmin’s most followed narrative puts fair value at $260.25 compared with the last close of $241.90, which suggests the model still sees some upside from here.

The launch of the Garmin Connect+ premium service, which offers AI-based health and fitness insights, is likely to boost subscription-based revenue growth and improve overall margins through higher-margin services. The new vívoactive 6 smartwatch release, with advanced features like an AMOLED display and enhanced sports apps, suggests potential revenue growth in the Fitness segment, supported by strong demand for advanced wearables.

Want to see what kind of revenue path and profit margins are baked into that fair value, and how rich a future P/E the narrative leans on? The full story connects fitness momentum, premium services and long term earnings power in a way that is not obvious from the headline numbers alone.

Result: Fair Value of $260.25 (UNDERVALUED)

However, you still need to weigh risks such as rising operating expenses and softer Marine demand, which could pressure margins if revenue momentum does not keep up.

Another Angle on Valuation

The narrative fair value of $260.25 suggests Garmin is 7.1% undervalued, but the current price of $241.90 sits above the SWS DCF estimate of $228.49, which points to the stock being overvalued on future cash flows. So which lens do you trust more: story driven fair value or cash flow math?

Next Steps

With mixed signals on value and sentiment running both hot and cold, now is a good time to look through the data yourself and decide what really matters for you. To see the balance of potential upside against the issues investors are worried about, check out the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Garmin has sharpened your interest, do not stop here. Use the tools at your fingertips now so you are not looking back wishing you had.

- Spot potential high yield opportunities before others by scanning companies that qualify as 12 dividend fortresses.

- Zero in on quality at a discount by reviewing the 51 high quality undervalued stocks that pass strict fundamental checks.

- Get ahead of the crowd by filtering for a screener containing 23 high quality undiscovered gems that most investors are not watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.