General Dynamics (GD) Stock Could Be 13% Undervalued As Raised Guidance Lands

General Dynamics Corporation GD | 0.00 |

General Dynamics stock has delivered a 120.5% total return over the past 5 years, and the current valuation checks suggest the shares may still trade below an intrinsic value estimate rather than at an outright premium.

- A 120.5% return over 5 years indicates investors have already priced in a meaningful amount of success, so any further upside case rests on how durable that performance proves to be.

- Recent orders in areas like C5ISR and expectations for ongoing earnings growth can support the intrinsic value, while any slowdown in defense spending or delays to large contracts may weigh on what investors are willing to pay.

- The stock screens as undervalued on both a Discounted Cash Flow (DCF) intrinsic value estimate and on earnings multiples, yet the broader checks form a mixed picture, with General Dynamics scoring 4 out of 6 on valuation rather than looking unambiguously cheap.

The issue now is whether that combination of strong long term returns and an apparent valuation gap still leaves enough margin of safety for investors considering General Dynamics today.

Is General Dynamics Still Cheap on Cash Flow?

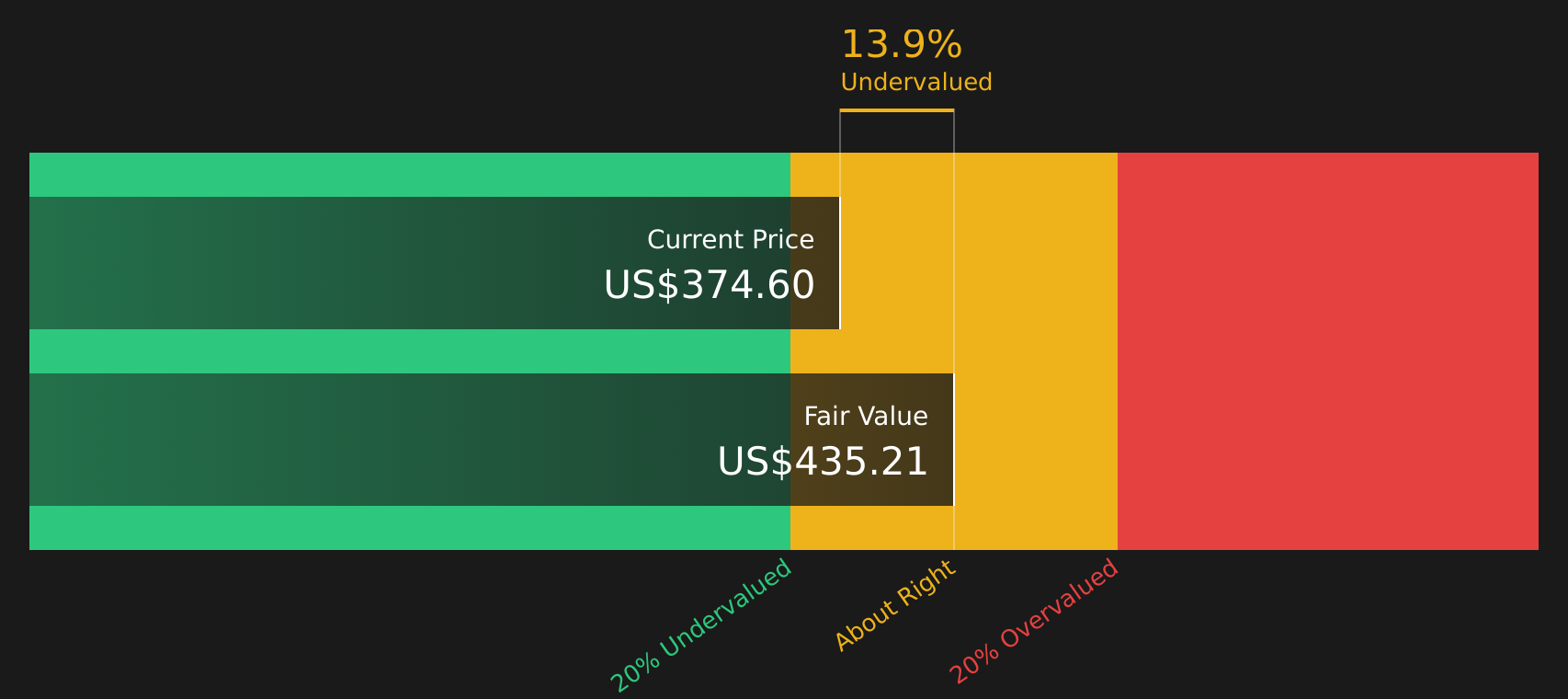

The Discounted Cash Flow (DCF) model values General Dynamics by projecting its future cash flows and discounting them back to today. On this basis, the company is modeled on growing cash flows rather than a shrinking business, with latest twelve month free cash flow of about $6.3b helping anchor the projections. Using a 2 Stage Free Cash Flow to Equity approach, this stream of cash flows points to an estimated intrinsic value of about $431 per share.

Compared with the current share price around $354, that intrinsic value implies General Dynamics screens as roughly 13.2% undervalued. Because the recent surge in General Dynamics shares followed raised earnings guidance and a larger order backlog, the gap suggests the market is recognizing the reported outlook but still values the stock below what the cash flow model supports.

On this DCF view, General Dynamics stock currently appears undervalued relative to its estimated intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests General Dynamics is undervalued by 13.2%. Track this in your watchlist or portfolio, or discover 45 more high quality undervalued stocks.

Is General Dynamics a Bargain on Earnings?

The P/E ratio is a straightforward way to see what you are paying today for each dollar of General Dynamics earnings. At about 23.3x, General Dynamics trades below both the Aerospace & Defense industry average P/E of 41.4x and a peer group average of 36.5x. This suggests the stock is not priced at the richer end of its sector.

A fair P/E ratio for General Dynamics, based on its size, margins, industry and risk profile, is estimated at 30.3x. That is meaningfully higher than the current 23.3x multiple. This implies the market is valuing the company at a discount to where this framework would place it, even after the recent share price strength.

On this P/E lens, General Dynamics stock appears undervalued relative to the earnings multiple a benchmark model would suggest.

The General Dynamics Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for General Dynamics link the valuation puzzle to clear, testable assumptions about the company’s future growth, margins and earnings, so you can see what would need to happen for the stock to be worth materially more or less than today’s price. Instead of stopping at a single number from a ratio or model, they set out the future that number relies on, so you can watch how closely reality tracks it on the Community page.

Add your own narrative on General Dynamics to present a number-driven view on whether its earnings outlook, backlog and recent C5ISR developments support today's price.

Share how you are weighing those drivers, be one of the first voices in the Simply Wall St community to put a clear case on General Dynamics and track how it holds up as new results and contract updates arrive.

Do you think there's more to the story for General Dynamics? Head over to our Community to see what others are saying!

The Bottom Line

General Dynamics screens as undervalued on both the Discounted Cash Flow (DCF) intrinsic value estimate and on its P/E multiple, and those two views broadly point in the same direction. The broader checks are mixed rather than emphatically cheap, so the current discount looks more like a measured valuation gap than a glaring mispricing. What matters from here is whether General Dynamics can translate its order backlog and programs into sustained cash generation and earnings, because that is what would either close the gap or confirm that the market is already pricing the risks correctly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.