General Motors Stock Faces Fresh Pressure As Oil And Inflation Squeeze Demand

Delta Air Lines, Inc. DAL | 0.00 |

US inflation at 4.2%, oil at about US$85 a barrel, and a squeezed consumer are a tough mix for companies that rely heavily on fuel, raw materials, or discretionary spending. This High Inflation and Energy Price Pressure Stocks screener focuses on businesses that are closely exposed to this news, from higher transport and production costs to weaker household demand. In this article, you will see 3 stocks that appear more vulnerable to the current backdrop, which may help you decide which stories might warrant extra caution, closer monitoring, or a fresh look at your risk exposure.

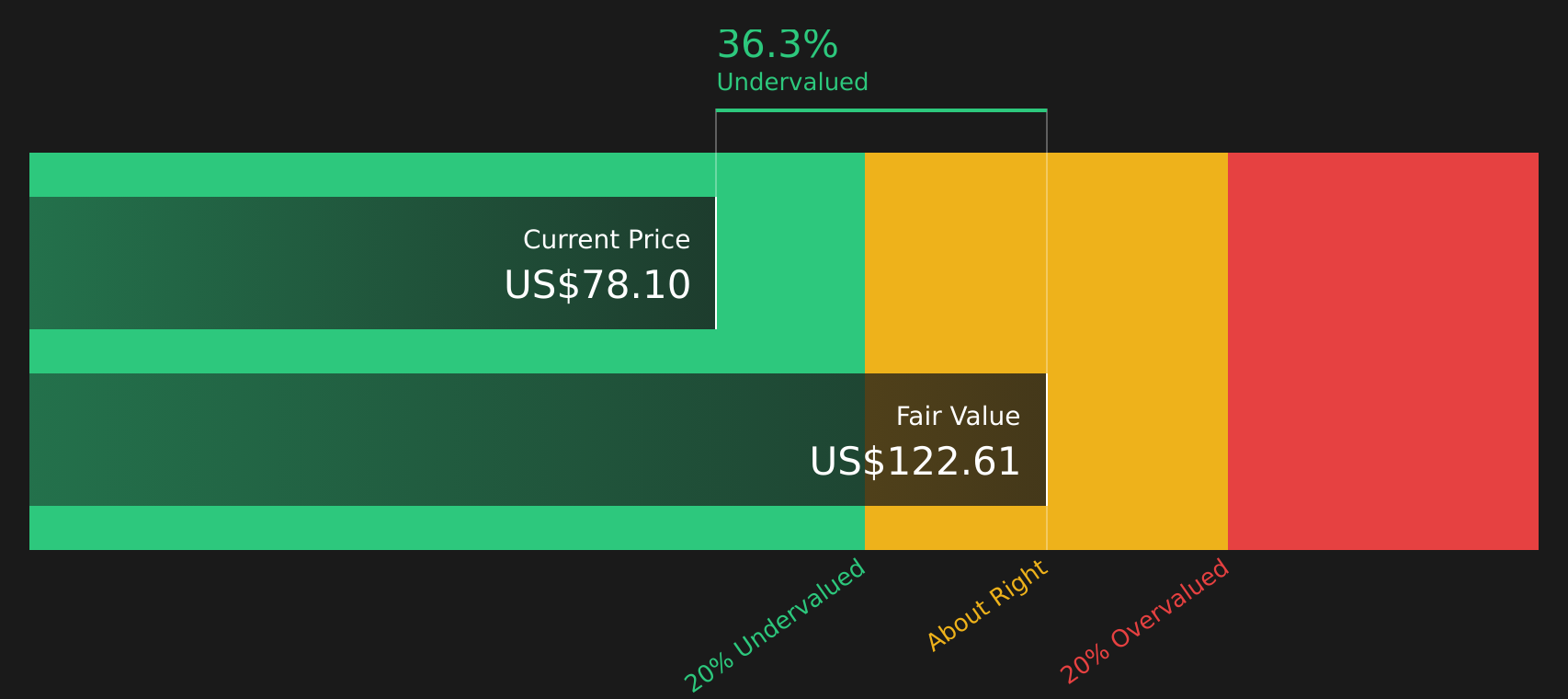

General Motors (GM)

Overview: General Motors is a Detroit based automaker that designs, builds, and sells trucks, crossovers, cars, and parts worldwide under brands such as Chevrolet, GMC, Cadillac, and Buick, and also provides financing, software enabled services, and subscription offerings through GM Financial.

Operations: General Motors generates most of its revenue from Automotive, with GM North America contributing about US$153.3b, alongside GM Financial at roughly US$17.2b and smaller corporate and segment items.

Market Cap: US$70.4b

General Motors sits in the firing line of higher oil prices and weak consumer confidence, with fuel intensive trucks and SUVs facing both rising input and logistics costs and pressure on household budgets. The company is investing heavily in EVs, batteries, and grid services. However, current net margins are thin at 1.3%, recent earnings were hit by a US$9.0b one off loss, and debt is not well covered by operating cash flow. Forecast earnings growth and an apparent discount to estimated fair value might tempt some investors. At the same time, significant insider selling, elevated external borrowing, and uncertainty around how prolonged inflation and the Iran conflict will feed into demand mean the risk side of the ledger may warrant closer attention.

Thin 1.3% margins, a recent US$9.0b loss, and rising borrowing costs could mean the real stress test for General Motors is still ahead. It is therefore worth reading the 2 key rewards and 4 important warning signs (1 is major!)

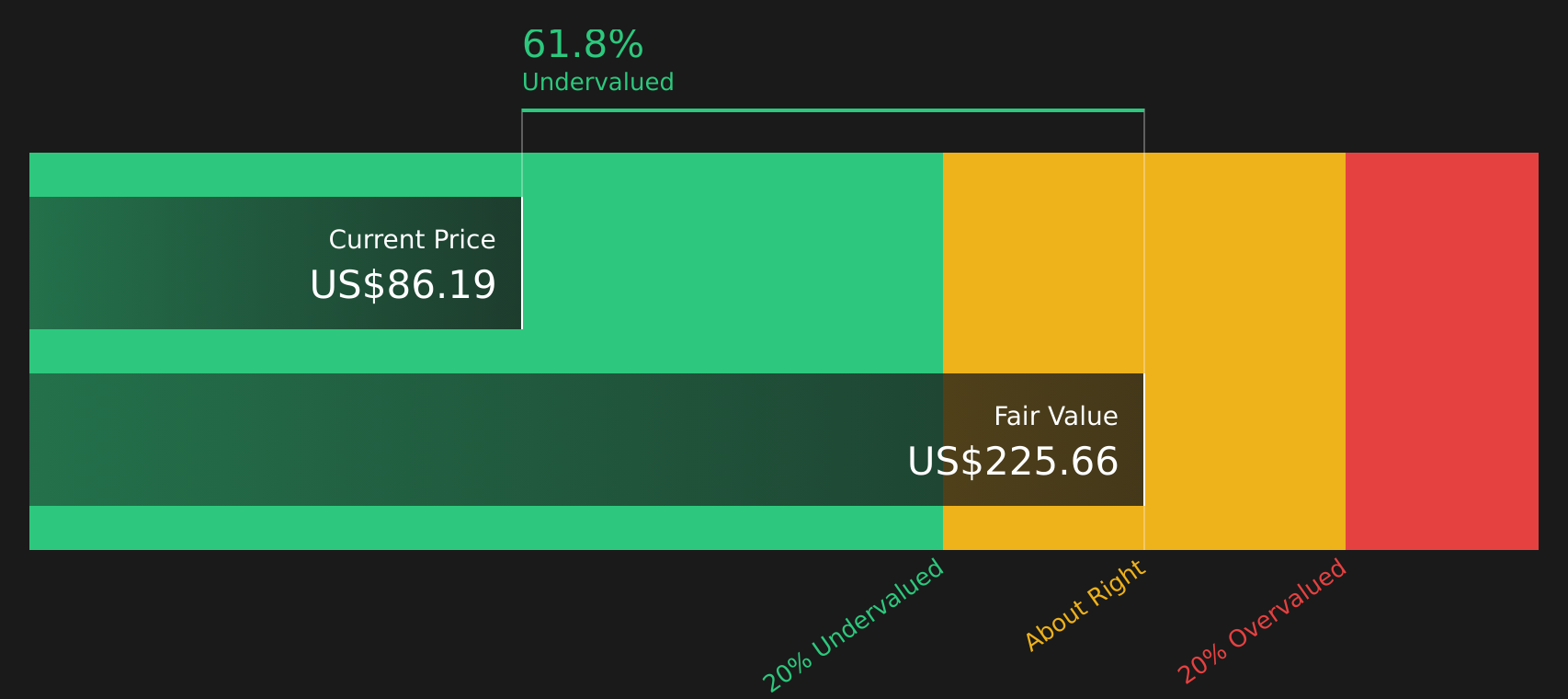

Delta Air Lines (DAL)

Overview: Delta Air Lines is a major US airline that flies passengers and cargo across an extensive domestic network and long haul routes in Europe, Latin America, the Pacific, and other international markets, and also sells vacation packages and maintenance services using a fleet of roughly 1,314 aircraft.

Operations: Delta Air Lines generates most of its revenue from the Airline segment at about US$59.5b, with the Refinery segment contributing roughly US$7.3b and intersegment sales reducing the total by about US$1.6b.

Market Cap: US$60.5b

Delta Air Lines sits at the center of the latest inflation shock, with jet fuel tied closely to oil at US$85 a barrel and management already talking about cutting capacity and recapturing higher fuel costs through fares. Premium and loyalty revenue, high quality earnings, and strong profitability metrics paint an appealing picture. However, a debt heavy balance sheet, significant insider selling, and the risk that higher airfares eventually reduce demand all point to a tougher road if inflation and energy prices stay elevated. With management also warning that high fuel prices tend to separate stronger airlines from weaker ones, Delta’s current valuation and analyst optimism may warrant a cautious second look before assuming this stock can continue to withstand economic pressure.

Delta’s debt heavy balance sheet and fuel exposure could be masking the real pressure point here, so it is worth reading the 3 key rewards and 2 important warning signs to see where the story could unexpectedly turn next.

Walmart (WMT)

Overview: Walmart is a global retailer that runs supermarkets, warehouse clubs, and ecommerce platforms, offering groceries, household essentials, general merchandise, health services, and financial products to consumers across the U.S. and international markets.

Operations: Walmart generates most of its revenue from Walmart U.S. at about US$490.9b, with Sam's Club contributing roughly US$97.0b, Walmart International around US$137.4b, and Corporate and Support about US$72m.

Market Cap: US$920.7b

Walmart looks like a defensive giant at a difficult moment for consumers, yet the story is less comfortable than it first appears. Inflation at 4.2% and higher fuel costs are already pushing shoppers toward smaller fuel fill ups and more cautious baskets, while stubborn grocery and consumables inflation risks squeezing discretionary categories that tend to carry better margins. At the same time, the stock trades on a rich P/E multiple, carries a high level of debt, and has seen significant insider selling. International ecommerce and rapid delivery services also continue to pressure profitability. For investors, the key question is whether AI, advertising and memberships can really offset these headwinds before stretched household budgets start to bite harder.

Walmart’s relatively high P/E, elevated debt, and insider selling suggest the story may be more fragile than it appears, so it is worth reading the 2 key rewards and 2 important warning signs

Take Control of Your Investment Journey

If Delta Air Lines or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh stock ideas do not stay under the radar for long, and early momentum can fly once the crowd catches up, so review these curated lists now and act early.

- Target resilient income by reviewing the curated 8 dividend fortresses that aim to keep cash flows coming even when markets feel unsettled and sentiment is dropping fast.

- Spot potential future infrastructure leaders by scanning the hand picked 35 power grid technology and infrastructure stocks positioned around grid upgrades, electrification momentum, and capital cycles that matter before the crowd fully pays attention.

- Get ahead of the next computing shift by assessing the curated 30 quantum computing stocks while the opportunity set is still forming and entry points remain fresh for patient investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.