Genesis Energy (GEL) Looks Cheap After A Weak Year But Losses Cloud The Picture

Genesis Energy, L.P. GEL | 0.00 |

Recent trading performance and business mix

Genesis Energy (GEL) has seen its unit price move within a mixed range recently, with the stock up 0.6% over the past day but down over the past week, month and past 3 months.

Over the past year, the total return has declined 15.3%, while longer windows show gains, including a 3 year total return that is more than 7x and a 5 year total return above 50%.

At a last close of $14.11, Genesis Energy sits in the mid cap range, with a market value of about $1.7b and operations focused on midstream crude oil and natural gas services in the United States.

The business is diversified across three primary segments, each contributing meaningfully to revenue and exposing investors to different parts of the energy infrastructure chain.

- Offshore Pipeline Transportation generated $570.3 million in revenue and centers on offshore crude oil and natural gas pipeline systems, platforms and related infrastructure.

- Onshore Transportation and Services contributed $789.5 million, tied to crude oil transportation, storage, blending, marketing and related processing activities, including sodium hydrosulfide by products.

- Marine Transportation delivered $318.9 million, supported by inland and offshore fleets that handle crude oil, refined products and asphalt, along with the M/T American Phoenix tanker.

Total reported revenue stands at $1.68b, while the company reported a net loss of $22.7 million and modest annual revenue growth of 0.4%. This highlights a business that is generating substantial sales but not currently delivering positive net income.

For investors, Genesis Energy’s mix of offshore pipelines, marine assets and onshore logistics provides different revenue streams across the U.S. energy infrastructure. This can be important when comparing it with other midstream partnerships or income focused energy stocks.

Genesis Energy’s recent 1 day share price gain sits against a series of weaker short term moves, while the 1 year total shareholder return is down and the 3 and 5 year total shareholder returns remain positive, suggesting long term momentum has been stronger than the latest pullback.

If you are comparing Genesis Energy with other income and infrastructure ideas, it can be useful to widen the lens and review 35 power grid technology and infrastructure stocks

With Genesis Energy units down over the past year but trading at a sizeable discount to some analyst value estimates, should you see the recent weakness as a chance to buy, or assume the market is already pricing in future growth?

Preferred Price-to-Sales Ratio of 1x: Is it justified?

At a last close of $14.11, Genesis Energy is being valued at about 1x its $1.68b in revenue, which screens as cheaper than many Oil and Gas peers yet roughly in line with the fair P/S level suggested by the data.

The P/S multiple compares the company’s market value of about $1.7b with its total sales and is often used when earnings are weak or volatile. For Genesis Energy, this is relevant because the partnership is currently loss making, with a reported net loss of $22.7 million, so profit based measures such as P/E are less informative.

On one hand, the stock is described as good value when its 1x P/S is compared to the peer average of 3.1x and the broader US Oil and Gas industry average of 1.8x. This suggests the market is applying a lower revenue multiple than many comparable companies. On the other hand, the same analysis flags Genesis Energy as expensive versus its estimated fair P/S ratio of 1x. This implies the current multiple is already close to where the SWS model suggests it could settle over time.

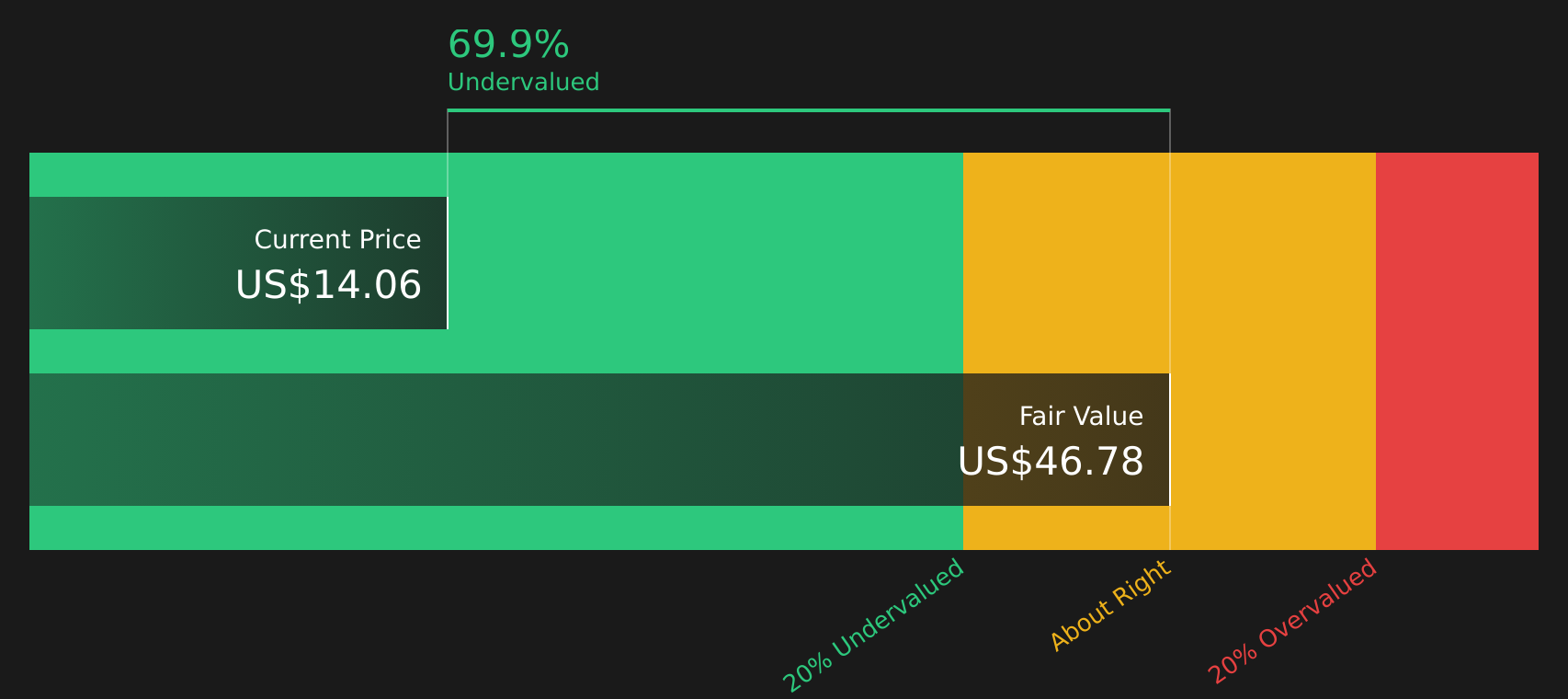

For investors, the tension between a discount to peers and a P/S ratio that sits near the estimated fair level comes on top of other valuation markers such as trading 69.8% below an internal fair value estimate and a sizeable 37% gap to the average analyst price target. This mix points to a stock that the models do not treat as obviously mispriced on revenues alone, even if other valuation approaches are more optimistic about upside.

Result: Preferred multiple of Price-to-Sales of 1x (ABOUT RIGHT)

However, Genesis Energy’s recent net loss and weaker 1 year total return raise questions about how resilient the current valuation case is.

Another view on Genesis Energy’s value

The earlier P/S check suggested Genesis Energy does not look obviously cheap or expensive on revenue alone. In contrast, the SWS DCF model points to a fair value of about $46.77 per unit versus the current $14.11, implying the units trade at a wide discount. Which signal do you treat as more important?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Genesis Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around Genesis Energy’s value and outlook, are you comfortable relying only on headline metrics, or do you want to push deeper into the details yourself? To weigh the concerns against the potential upside, it can help to review the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Genesis Energy?

If Genesis Energy has you thinking about where to look next, use this moment to broaden your watchlist and compare other opportunities side by side.

- Target quality at a discount by scanning companies that look attractively priced on fundamentals using the 44 high quality undervalued stocks.

- Strengthen your income potential by reviewing resilient payers featured in the 8 dividend fortresses.

- Spot tomorrow’s potential standouts early by checking the screener containing 19 high quality undiscovered gems before they are widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.