Gentherm (THRM) Could Be 24% Below Fair Value As It Secures New Credit Facility

Gentherm Incorporated THRM | 0.00 |

Gentherm’s New Credit Facility and What It Means for Investors

Gentherm (THRM) has entered into a Third Amended and Restated Credit Agreement that provides a secured five year revolving credit facility of up to US$550 million, a material financing step for the company.

The new facility includes a US$50 million swing line sublimit and a US$30 million letter of credit sublimit. This gives Gentherm additional tools to manage working capital, potential acquisitions, or other corporate uses as conditions change.

Gentherm’s share price has recently dipped, with a 1 day share price return of a 0.86% decline and a 30 day share price return down 4.88%. However, the 90 day share price return of 18.77% and 1 year total shareholder return of 13.98% indicate improving momentum against a weak 3 year and 5 year total shareholder return record.

If Gentherm’s new credit facility has you thinking about where capital might flow next in the auto and comfort technology supply chain, it can be useful to see which other businesses are positioning for long term trends in areas like vehicle electrification, advanced materials or complex manufacturing. To broaden that view beyond a single stock, now could be a good time to check out a screener of 19 top founder-led companies

With Gentherm stock trading at US$34.48 against an average analyst target of US$40.57 and an indicated intrinsic value gap of about 46%, the key issue now is where fair value realistically sits within that range.

Most Popular Gentherm Narrative: 24.4% Undervalued

Against Gentherm’s last close of $34.48, the most followed narrative points to a fair value of $45.60, which implies a meaningful valuation gap that rests on specific growth, margin and discount rate assumptions rather than short term sentiment.

Expanding adoption of advanced comfort features and proprietary technologies positions Gentherm for robust, stable growth and greater pricing power across global automotive markets. Diversification into adjacent industries and deepening ties with Chinese OEMs enhance earnings stability, reduce cyclicality, and open new revenue avenues.

Curious what sits behind that fair value for Gentherm? The narrative leans heavily on rising earnings power, improving margins and a future earnings multiple that marks a clear shift from today’s pricing.

Result: Fair Value of $45.60 (UNDERVALUED)

However, Gentherm’s story could look very different if margin pressure persists, or if its underrepresentation in key Asian markets limits the impact of those comfort and medical growth drivers.

Another View on Gentherm’s Valuation

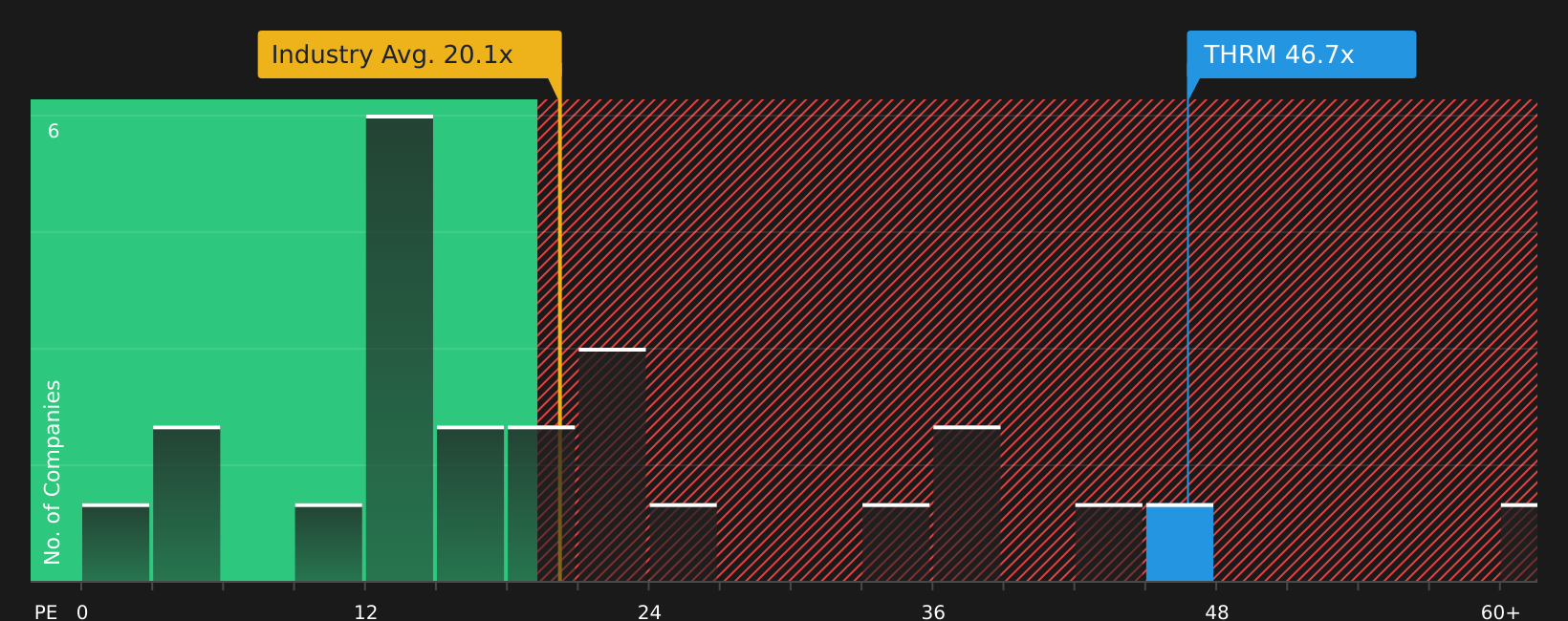

So far, Gentherm looks undervalued on fair value estimates, yet the market is pricing the stock at a P/E of 46.7x. That is more than double the US Auto Components industry at 20.8x and well above a fair ratio of 29.9x, which points to meaningful valuation risk if sentiment cools.

For investors, that spread raises a simple question: is the current price already baking in a good part of the optimism that other models treat as upside?

Next Steps

Given the mixed signals around Gentherm’s valuation and outlook, it can be useful to review the underlying data yourself using the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Gentherm?

If Gentherm has sharpened your focus on valuation and risk, do not stop here, the next opportunities you research today could shape your returns over the coming years.

- Target reliable compounding potential by reviewing companies that screen well on balance sheet strength and fundamentals through the solid balance sheet and fundamentals stocks screener (47 results).

- Spot potential mispriced opportunities early by scanning the screener containing 18 high quality undiscovered gems for high quality businesses that many investors may be overlooking.

- Prioritize resilience in tougher markets by focusing on companies flagged in the 74 resilient stocks with low risk scores that pair lower risk scores with more durable profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.