Glacier Bancorp (GBCI) Could Be 11% Undervalued As Record Q1 Profit Lifts The Case

Glacier Bancorp, Inc. GBCI | 0.00 |

Glacier Bancorp (GBCI) kicked off 2026 with Q1 results that included record net income and a wider net interest margin, while revenue met analyst expectations and net interest income came in slightly below estimates.

Glacier Bancorp's share price is US$50.26 after a recent pullback, with a 1 day share price return down 3.29% and a 7 day share price return down 4.72%. The year to date share price return of 12.59% and 1 year total shareholder return of 11.92% point to momentum that has softened in the short term but remains positive over longer periods.

If the Q1 update has you reviewing your watchlist, this can be a good moment to broaden your search and check out 19 top founder-led companies

After a strong quarter and a recent pullback, Glacier Bancorp now trades at a price that sits between a modest discount to analyst targets and a wider gap to some intrinsic value estimates, so where does fair value really lie?

Most Popular Narrative: 11.2% Undervalued

On the latest numbers, Glacier Bancorp's most followed narrative pegs fair value at about $56.58, compared with the current share price of $50.26. This frames the recent pullback against a higher long term earnings story.

The continued migration and population growth in Glacier Bancorp's core markets of the Mountain West and Pacific Northwest are driving robust loan and deposit growth, positioning the bank for sustainable revenue and earnings expansion as these regions urbanize and develop. Investments in digital platforms, such as the new commercial loan system and enhanced treasury solutions, are improving operational efficiency, lowering cost to income ratios, and attracting younger, tech savvy customers, all of which support higher net margins and potential for future margin expansion.

Want to see what kind of revenue curve and margin profile would support that fair value gap for Glacier Bancorp? The narrative leans on compounded growth, rising profitability and a future earnings multiple that has to be justified by execution. The exact mix of revenue, profit and valuation assumptions may surprise you.

Result: Fair Value of $56.58 (UNDERVALUED)

However, the Glacier Bancorp story also hinges on successful acquisition integration and careful management of commercial real estate exposure. Setbacks in these areas could quickly challenge that fair value narrative.

Another View on Glacier Bancorp’s Valuation

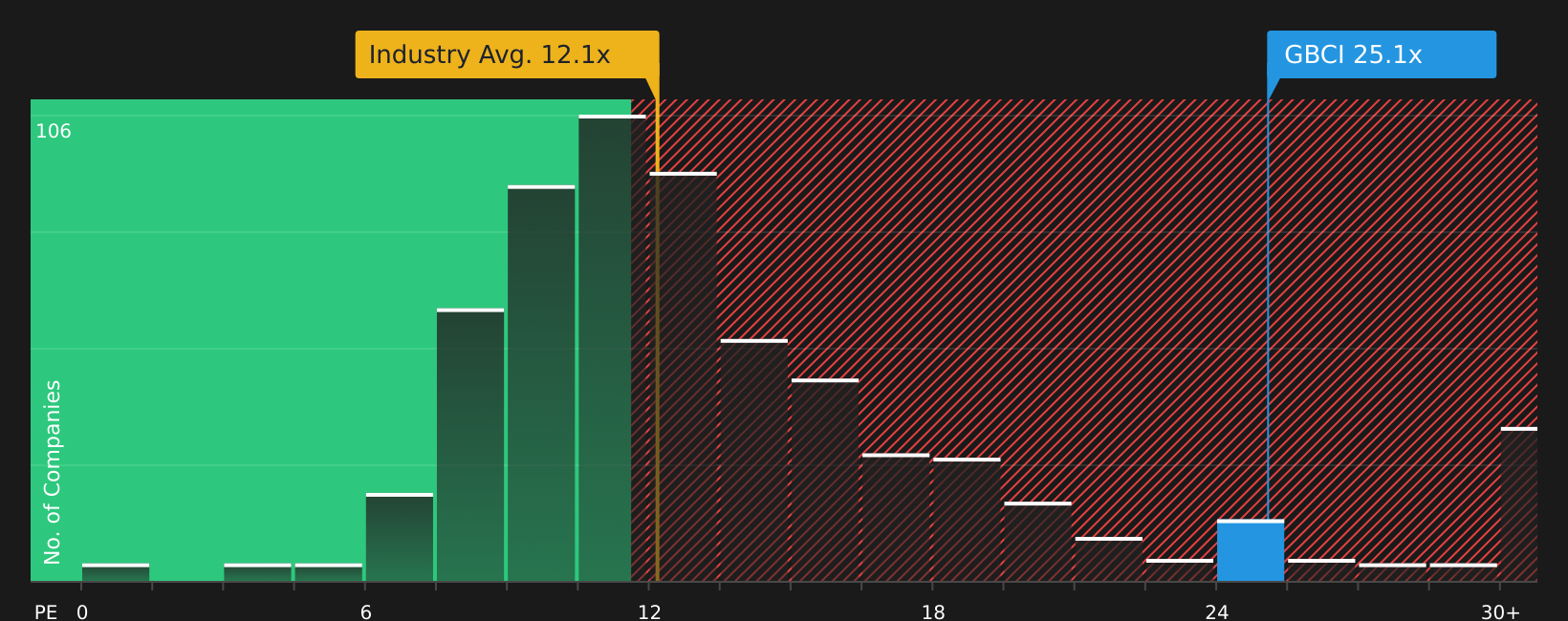

While the analyst narrative and fair value estimate of $56.58 frame Glacier Bancorp as undervalued, the market is also paying a rich price based on earnings. The current P/E of about 24.5x sits well above the US Banks industry at 12.2x and above an estimated fair ratio of 19.4x. This points to meaningful valuation risk if expectations cool.

Next Steps

With mixed signals on valuation and sentiment, do you want to rely on one story or weigh the trade off yourself? Move quickly, review both sides of the debate and see the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Glacier Bancorp?

If Glacier Bancorp has sharpened your focus, do not stop here. Use the Simply Wall St Screener to spot fresh ideas before others catch on.

- Target steady income potential by reviewing companies in the 9 dividend fortresses that currently offer higher yields with detailed payout and consistency checks.

- Hunt for quality at a sensible price by scanning the 44 high quality undervalued stocks that filters for strong fundamentals and attractive valuations in one place.

- Prioritize resilience by checking the 72 resilient stocks with low risk scores that highlights stocks with lower risk scores and more robust financial profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.