Globe Life (GL) Stock Could Be 2% Overvalued After Strong Quarterly Growth

GLOBE LIFE INC GL | 0.00 |

Globe Life (GL) is back in focus after reporting year over year growth in quarterly revenue and net profit, paired with strong operating efficiency, technical buy signals, and rising institutional ownership.

Globe Life’s recent quarterly beat comes on top of a strong share price run, with a 30 day share price return of 12.35% and 90 day share price return of 27.69%. The 1 year total shareholder return of 44.07% points to momentum that has extended beyond short term trading.

If Globe Life’s move has you looking for other ideas with solid trends, it could be worth scanning through a curated list of 20 top founder-led companies

With Globe Life now carrying a recent 1 year total shareholder return of 44.07%, a financial health score of 8.07, and a P/E of 11.64, the key question is whether there is still an opportunity for investors to consider here or if the market is already fully reflecting these metrics in its current pricing.

Most Popular Narrative: 2% Overvalued

Globe Life's most followed valuation narrative places fair value at $172.10, slightly below the last close of $175.58, which frames a modest premium in the current price.

The planned establishment of a Bermuda reinsurance affiliate is expected to significantly increase parent company free cash flow and financial flexibility by 2027 and beyond, providing greater capacity for share repurchases and/or strategic investments, positively impacting earnings per share.

Read the complete narrative. Read the complete narrative.

Want to see what sits behind that small premium to fair value? The narrative leans heavily on steady revenue expansion, firmer margins, and a tighter share count to justify its view.

Result: Fair Value of $172.10 (OVERVALUED)

However, the Globe Life narrative also rests on cleaner regulatory outcomes and resilient working and middle income customers, and setbacks on either front could quickly challenge it.

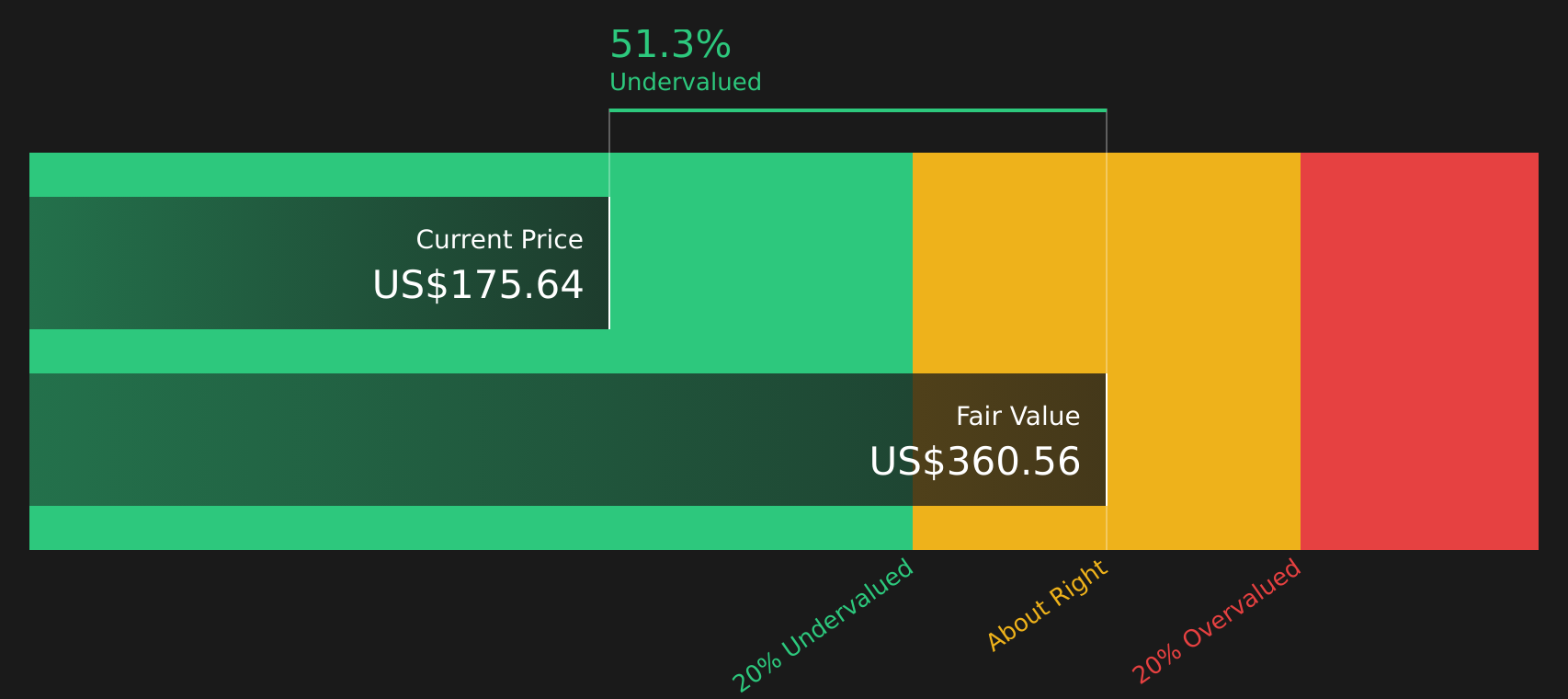

Another View: SWS DCF Versus Globe Life’s Premium

The narrative around Globe Life leans on a modest 2% premium to an estimated fair value of $172.10, yet the SWS DCF model points to a future cash flow value of $360.56, suggesting the current $175.58 price sits far below that cash flow based estimate.

For readers weighing which yardstick to trust, it helps to understand how the cash flow approach was built and why it diverges so sharply from price based multiples, before deciding which set of assumptions feels more realistic for Globe Life’s future cash generation. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Globe Life for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With Globe Life showing both supportive data points and open questions, it may be helpful to review the full picture yourself, including the 3 key rewards and 1 important warning sign

Looking for more Globe Life style investment ideas?

If Globe Life has sharpened your focus, do not stop here; use the Simply Wall St Screener to uncover fresh opportunities that could fit your approach just as well.

- Target resilient income by reviewing companies in the 7 dividend fortresses that may offer higher yields supported by solid underlying businesses.

- Hunt for potential bargains with the 44 high quality undervalued stocks that highlights companies combining quality metrics with pricing that some investors may consider attractive.

- Prioritize stability first and check the 67 resilient stocks with low risk scores which focuses on companies assessed to have more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.