Globe Life’s Bigger Credit Facility: What Does It Reveal About GL’s Evolving Capital Allocation Strategy?

GLOBE LIFE INC GL | 0.00 |

- In June 2026, Globe Life Inc. amended and restated its primary credit and term loan agreements, shifting administrative roles to Wells Fargo Bank, National Association, extending maturities to June 26, 2029 and June 26, 2031, and increasing its term loan capacity from US$250,000,000 to US$450,000,000.

- By lengthening debt maturities and expanding borrowing capacity while maintaining relationships with multiple banking partners, Globe Life has reinforced its financial flexibility to support ongoing operational and capital allocation plans.

- We will now examine how Globe Life’s extended debt maturities and increased term loan capacity may influence its existing investment narrative.

We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Globe Life Investment Narrative Recap

To own Globe Life, you need to be comfortable with an agent-centric life and health insurer that leans on steady underwriting, investment income, and disciplined capital returns. The recent extension of its credit and term loan maturities, along with higher borrowing capacity, modestly supports this by adding liquidity for operations and capital deployment, but it does not fundamentally change the main short term catalyst around earnings delivery or the ongoing risk from distribution and regulatory pressures.

The most relevant prior development here is Globe Life’s raised 2026 earnings guidance to US$15.40 to US$15.90 per diluted share, alongside continued buybacks. Together with the expanded term loan and longer-dated credit facilities, that guidance frames how additional financial flexibility could intersect with management’s capital allocation priorities, while still leaving execution on digital expansion, agent productivity, and regulatory risk as key factors to watch.

Yet beneath this seemingly stronger balance sheet, investors should still be aware of the ongoing DOJ and SEC investigations and the potential for...

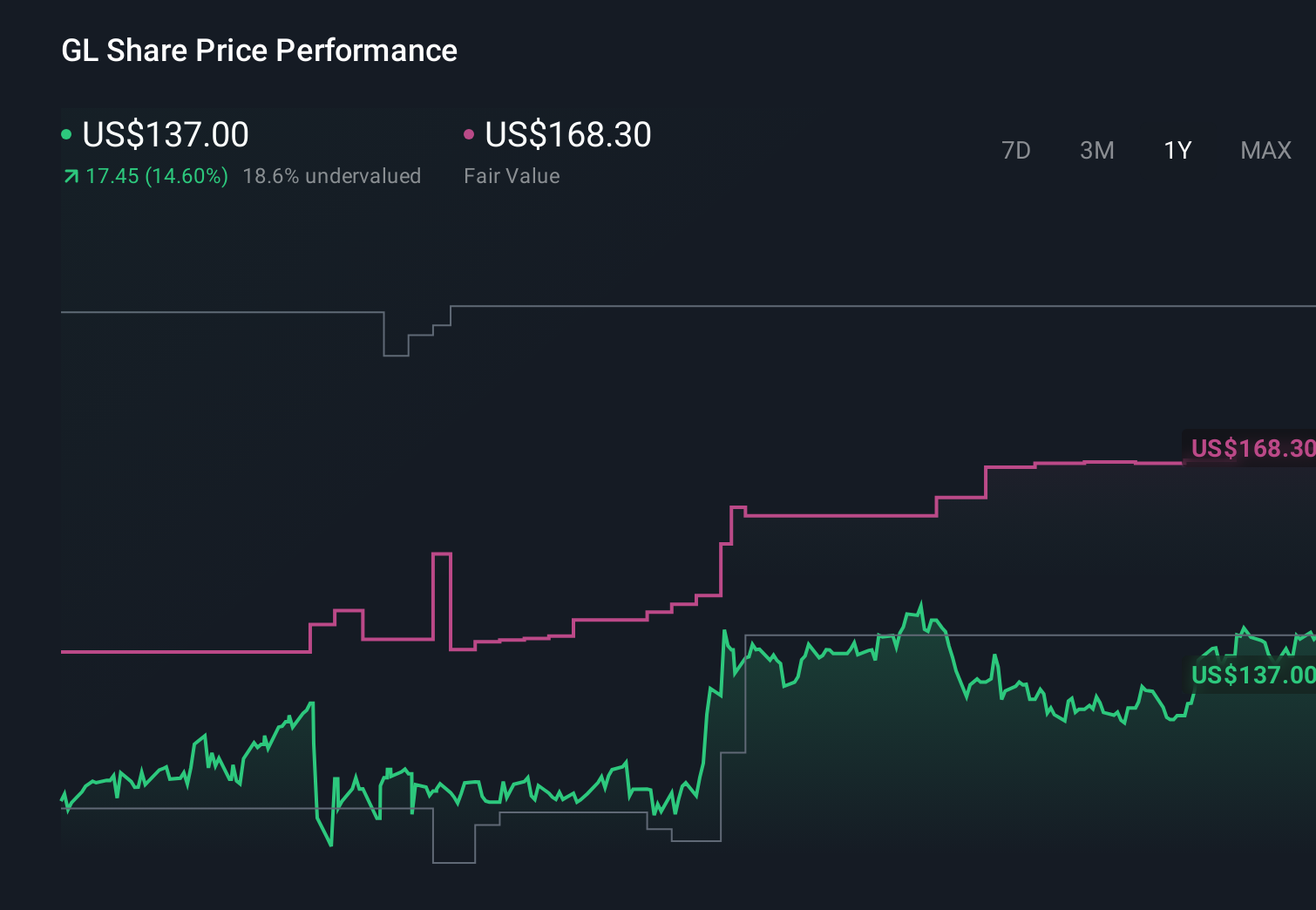

Globe Life’s narrative projects $6.8 billion revenue and $1.3 billion earnings by 2028. This requires 5.1% yearly revenue growth and about a $0.2 billion earnings increase from $1.1 billion today.

Uncover how Globe Life's forecasts yield a $172.10 fair value, a 5% downside to its current price.

Exploring Other Perspectives

More optimistic analysts already expected Globe Life to grow revenue to about US$7.6 billion and earnings to roughly US$1.4 billion by 2029, so if you agree that higher health claims and regulatory scrutiny could pressure those targets, this new financing could either support that upbeat view or prompt you to rethink just how much risk you are willing to accept.

Explore 3 other fair value estimates on Globe Life - why the stock might be worth just $172.10!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Globe Life research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Globe Life research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Globe Life's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.