GoDaddy’s Pricing Misstep and Insider Sales Might Change The Case For Investing In GDDY

GoDaddy, Inc. Class A GDDY | 0.00 |

- In recent weeks, GoDaddy disclosed that a fourth-quarter promotional price for dotcom domains reduced upfront bookings and near-term revenue more than expected, prompting a securities investigation by Kaplan Fox & Kilsheimer LLP into potential violations related to that pricing strategy.

- At the same time, insiders have sold about US$2.20 million of stock over three months without any offsetting insider purchases, adding another layer of concern around the company’s near-term outlook.

- We’ll now examine how the promotional pricing hit to near-term revenue and ensuing securities investigation could reshape GoDaddy’s investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

GoDaddy Investment Narrative Recap

To own GoDaddy, you need to believe its large small business customer base and expanding AI and web tools ecosystem can support durable earnings, even as competition and technology evolve. The recent promotional pricing misstep and related securities investigation appear focused on near term revenue timing, but they do increase headline and governance risk at a moment when the stock has already lagged the market and short term sentiment is fragile.

Against that backdrop, GoDaddy’s ongoing share repurchase program is an important counterpoint. The company has already bought back more than US$1.1 billion of stock under its current authorization, even as the share price has fallen. For investors watching the current investigation and the impact of discounted domains, that ongoing capital return raises fair questions about how management balances near term financial optics with longer term value creation.

Yet at the same time, the combination of pricing missteps, insider selling and a fresh securities investigation is information investors should be aware of as they consider...

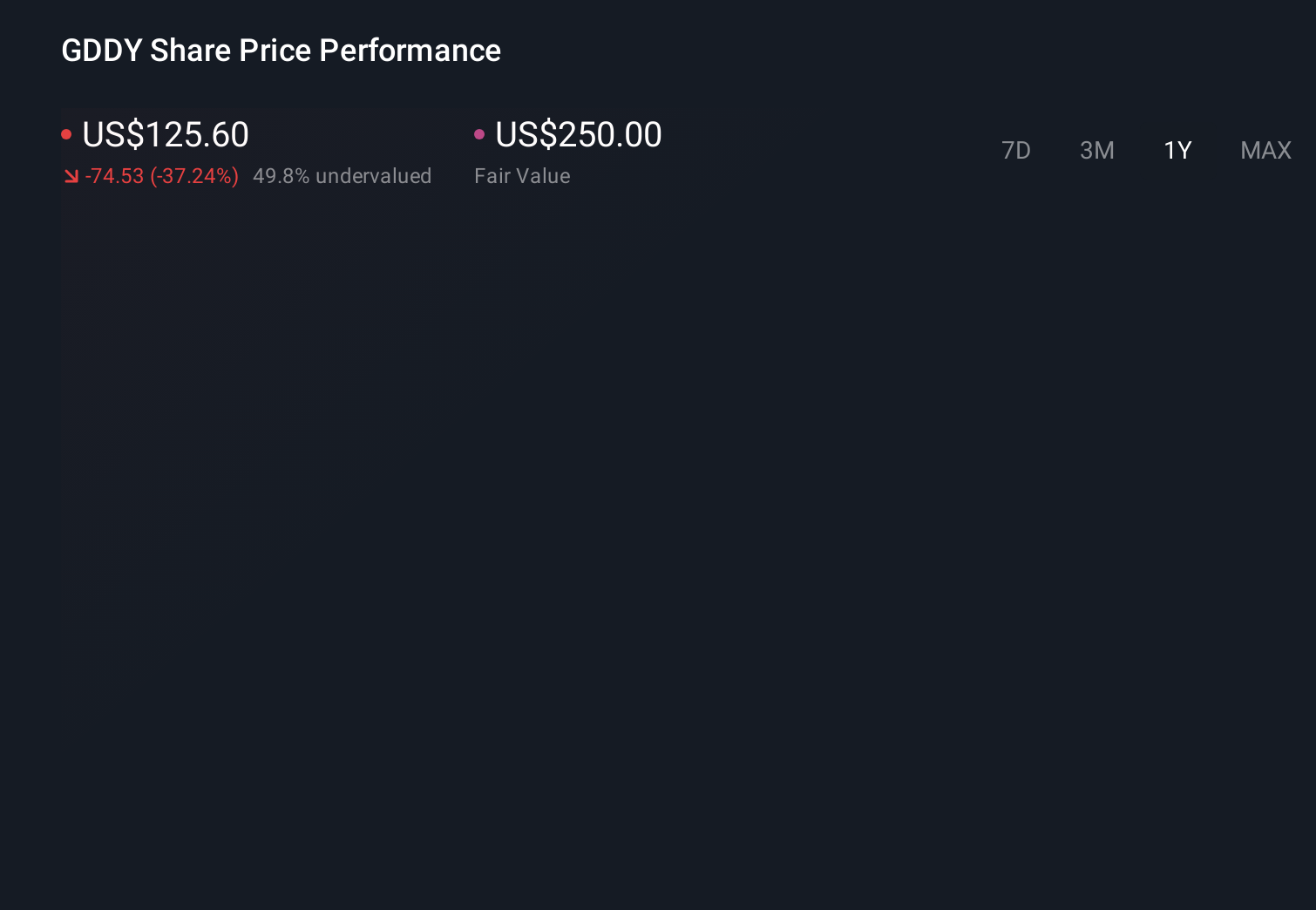

GoDaddy’s narrative projects $5.9 billion revenue and $1.3 billion earnings by 2029. This requires 5.7% yearly revenue growth and an earnings increase of about $0.4 billion from $870.1 million today.

Uncover how GoDaddy's forecasts yield a $114.29 fair value, a 48% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue of about US$5.8 billion and earnings near US$1.3 billion by 2029, and this new pricing controversy could either reinforce or challenge that more pessimistic view.

Explore 6 other fair value estimates on GoDaddy - why the stock might be worth over 3x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your GoDaddy research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free GoDaddy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GoDaddy's overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- This technology could replace computers: discover 31 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.