Green Plains (GPRE) Is Down 5.3% After Profitable Quarter On Lower Production And Revenue - Has The Bull Case Changed?

Green Plains Inc. GPRE | 0.00 |

- In the first quarter ended March 31, 2026, Green Plains Inc. reported US$445.8 million in sales, US$32.94 million in net income and lower year-on-year production across ethanol, distillers grains, ultra-high protein and renewable corn oil.

- The return to profitability despite reduced volumes and revenue highlights how cost control and mix improvements can influence Green Plains’ earnings profile.

- Next, we’ll examine how Green Plains’ return to profitability on reduced production and revenue interacts with its existing investment narrative and assumptions.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Green Plains Investment Narrative Recap

To own Green Plains, you need to believe its shift toward low carbon fuels and higher value coproducts can translate into steadier, more profitable earnings, even when volumes or sales soften. The latest quarter’s profitability on lower production and revenue supports that thesis, but also puts a spotlight on execution risk around cost control, product mix and policy support for carbon credits as key near term drivers. At this stage, the earnings beat does not materially change the biggest risks.

The Q1 2026 earnings release, showing US$445.8 million in sales and US$32.94 million in net income after a year of losses, is the clearest link to this story. It underscores how margin improvements and cost discipline can offset weaker volumes in ethanol and high protein output, tying directly into the catalyst that Green Plains can improve profitability through efficiency and mix, while still leaving open questions about how durable those gains are if protein markets stay soft.

Yet against this improving profit picture, the risk that large carbon credit exposure and shifting policy support could alter the payoff profile for current shareholders is something investors should be aware of...

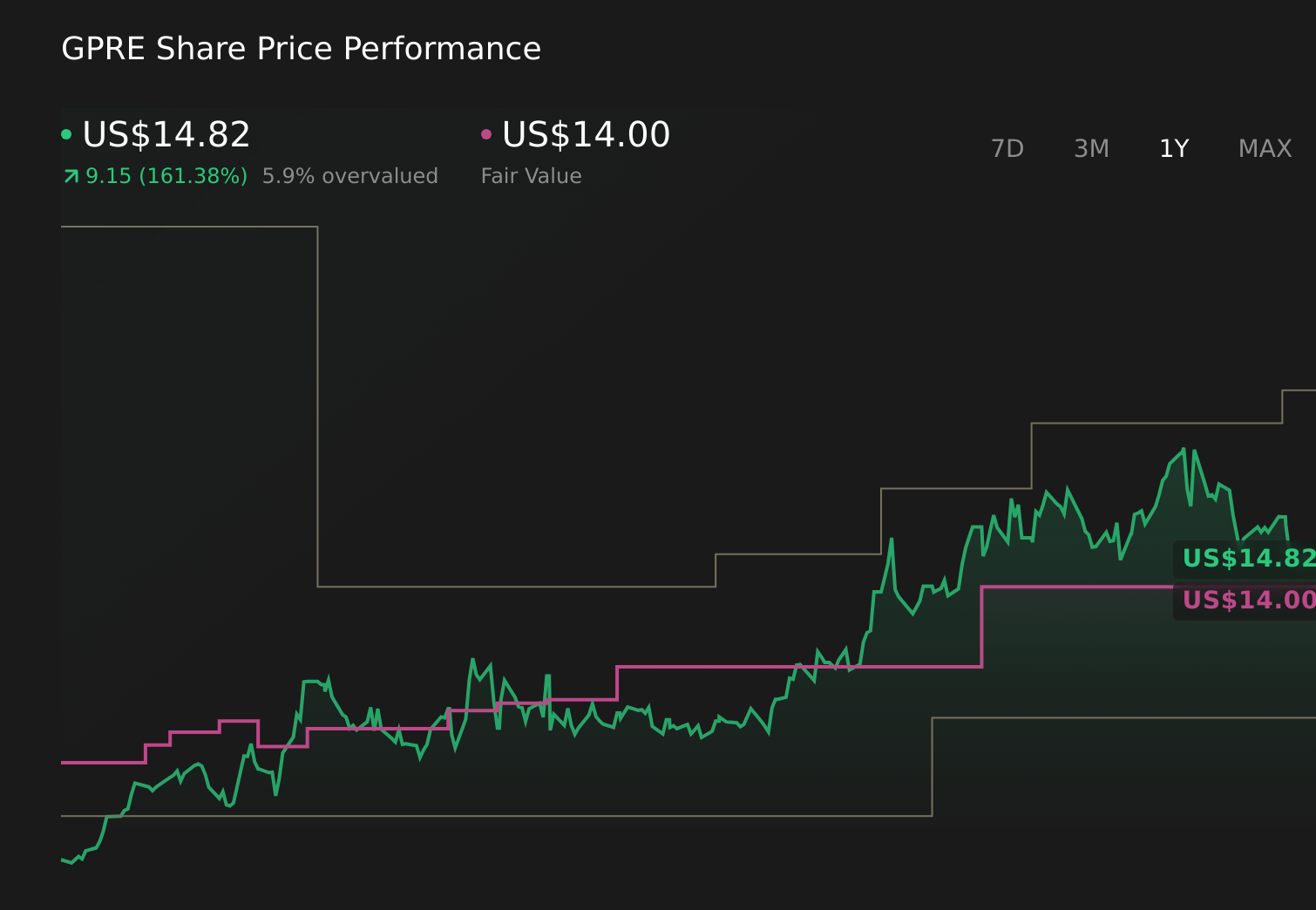

Green Plains' narrative projects $3.4 billion revenue and $116.3 million earnings by 2028.

Uncover how Green Plains' forecasts yield a $14.00 fair value, a 15% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting revenue to reach about US$3.7 billion and earnings of US$174 million, and Q1’s profit on lower volumes may either reinforce or challenge that much rosier outlook depending on how you view the same policy and project execution risks that still hang over Green Plains’ long term story.

Explore 3 other fair value estimates on Green Plains - why the stock might be worth 15% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Green Plains research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Green Plains research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Green Plains' overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.