Harrow (HROW) Is Up 6.8% After Reaffirming 2026 Revenue Outlook Despite Wider Q1 Losses - What's Changed

Harrow, Inc. HROW | 0.00 |

- In May 2026, Harrow, Inc. reported first-quarter 2026 results showing revenue of US$44.2 million versus US$47.83 million a year earlier, with net loss widening to US$27.6 million and basic loss per share from continuing operations rising to US$0.74 from US$0.50.

- Despite weaker quarterly performance, Harrow set second-quarter 2026 revenue guidance of US$71 million to US$81 million and reaffirmed full-year 2026 revenue guidance of US$350 million to US$365 million, highlighting management’s confidence in the company’s product portfolio and commercial trajectory.

- Next, we will examine how reaffirmed full-year revenue guidance, despite softer first-quarter results, affects Harrow’s existing growth-focused investment narrative.

The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Harrow Investment Narrative Recap

To own Harrow, you need to believe its core ophthalmic brands and late‑stage assets can eventually outgrow current losses and justify the company’s ambitious revenue targets. The key near term catalyst remains execution on 2026 guidance, particularly management’s reaffirmed full year revenue range, while the biggest risk is that weaker pricing or slower uptake in flagship products keeps revenue below those targets; this quarter’s miss makes that risk feel more immediate.

Against that backdrop, the most relevant recent announcement is Harrow’s decision to reaffirm its 2026 revenue guidance at US$350 million to US$365 million despite a softer first quarter. This effectively raises the execution bar for the rest of the year, keeping investor focus squarely on whether products like VEVYE, IHEEZO and TRIESENCE can support the implied step up in revenue while net losses remain elevated.

Yet even if guidance holds, investors should be aware of how rising losses and concentrated product exposure could quickly change if...

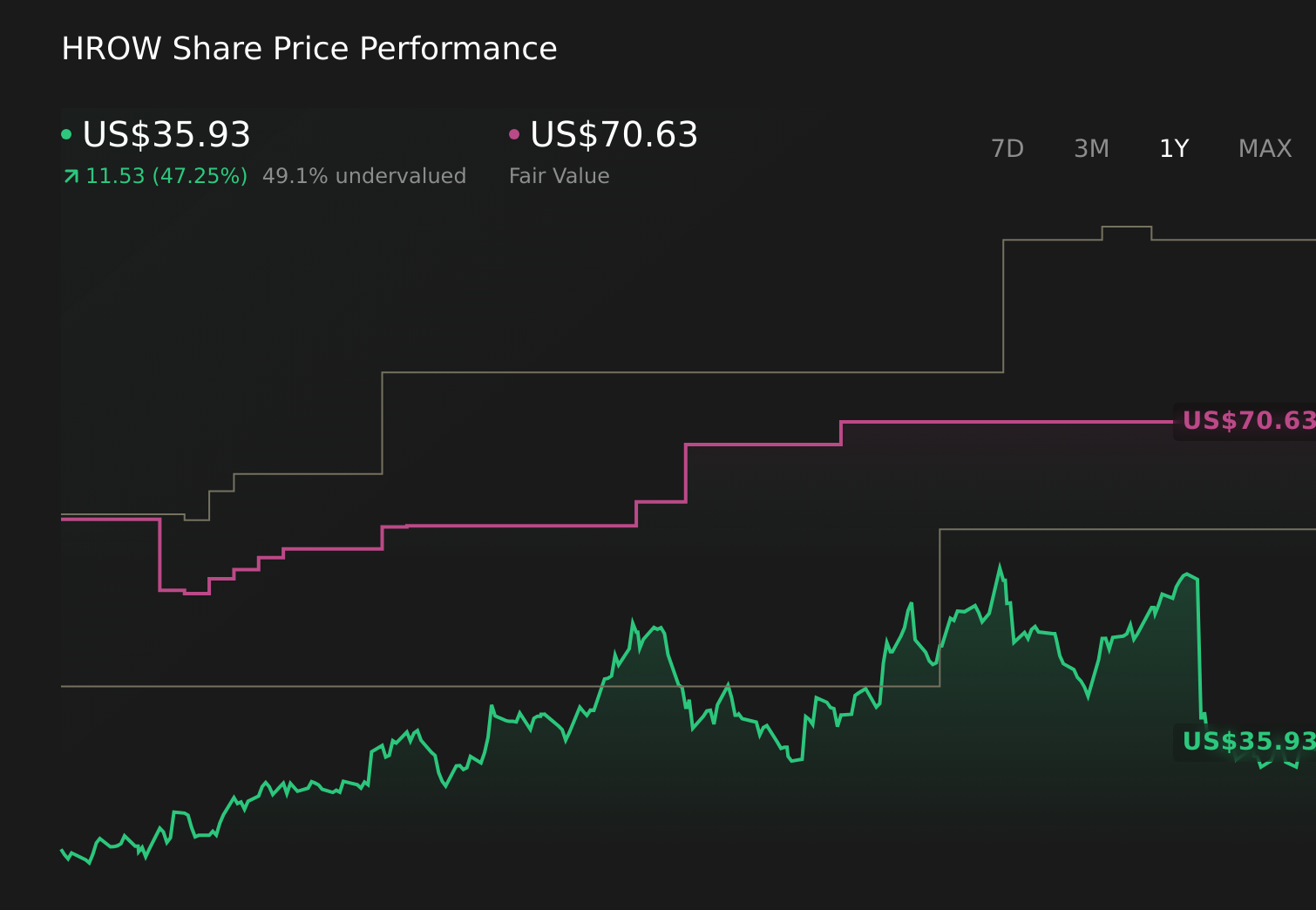

Harrow's narrative projects $784.8 million revenue and $246.0 million earnings by 2029.

Uncover how Harrow's forecasts yield a $68.38 fair value, a 107% upside to its current price.

Exploring Other Perspectives

Before this earnings miss, the most optimistic analysts were assuming Harrow could reach about US$831.4 million of revenue and US$262.0 million of earnings by 2029, so if you are weighing that upside against the risk that heavier spending and product concentration strain margins, this quarter’s setback is a reminder that different viewpoints can be valid and that both the bullish and cautious narratives may need updating as new data arrives.

Explore 3 other fair value estimates on Harrow - why the stock might be worth over 9x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Harrow research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Harrow research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Harrow's overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.