Has McDonald's (MCD) Share Price Run Ahead Of Its Long Term Value?

McDonald's Corporation MCD | 0.00 |

- If you are wondering whether McDonald's current share price reflects its true worth, you are not alone. This article focuses squarely on what you are paying versus what you may be getting.

- The stock last closed at US$306.26, with returns of 1.4% over 1 year and 47.7% over 5 years. The recent 6.2% decline over 30 days and 0.2% slip over 7 days suggest sentiment has cooled a little in the short term.

- Recent coverage has highlighted how investors are reassessing large, established consumer brands, with attention on whether current prices still make sense after several years of gains across the sector. This backdrop matters for McDonald's because it shapes how the market interprets even modest price moves in a mature, globally recognised business.

- Simply Wall St's valuation checks give McDonald's a 2 out of 6 score for being undervalued. The next sections will walk through what traditional valuation methods say about that score, before finishing with a more comprehensive way to think about valuation that pulls everything together.

McDonald's scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

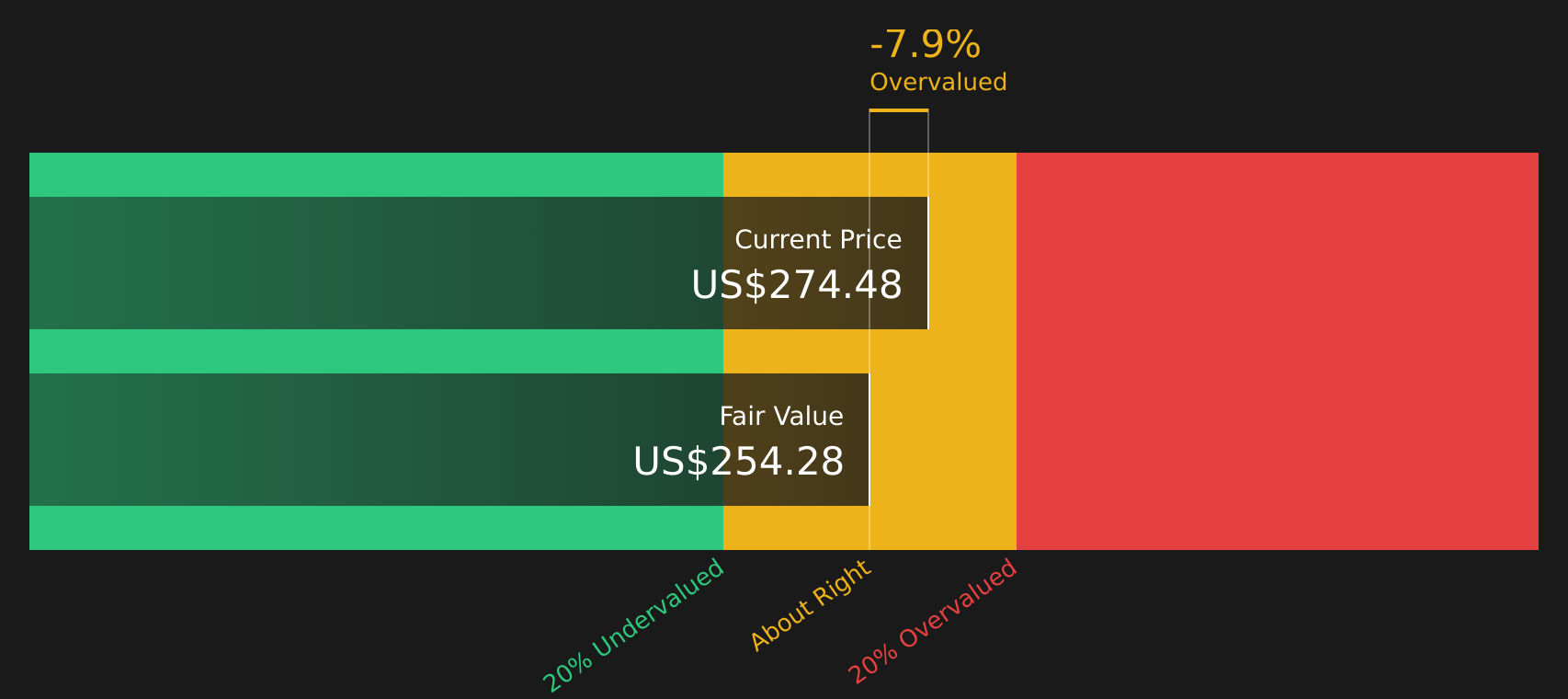

Approach 1: McDonald's Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of the cash a business may generate in the future, then discounts those cash flows back to today to arrive at an estimated present value per share.

For McDonald's, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $7.6b, and Simply Wall St uses analyst estimates through 2028 plus its own extrapolations out to 2035. For example, projected free cash flow for 2028 is $10.0b, with discounted values for the 2026 to 2035 period ranging from roughly $6.0b to $7.7b each year.

Adding these discounted cash flows and adjusting for the share count produces an estimated intrinsic value of about $254.77 per share. Compared to the recent share price of US$306.26, the DCF output implies McDonald's trades at roughly a 20.2% premium to this cash flow based estimate, which indicates the stock screens as expensive on this method alone.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests McDonald's may be overvalued by 20.2%. Discover 60 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: McDonald's Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. Investors usually accept a higher P/E if they expect stronger growth or see the earnings as relatively reliable, and look for a lower P/E when growth is modest or perceived risk is higher.

McDonald's currently trades on a P/E of 25.42x. That sits above the Hospitality industry average P/E of 21.58x, but below the broader peer group average of 56.01x. Simply Wall St also calculates a proprietary “Fair Ratio” of 31.14x for McDonald's, which is the P/E level that would typically line up with its earnings growth profile, industry, profit margins, market value and risk factors.

This Fair Ratio is more tailored than a simple comparison with peers or the industry because it blends company specific characteristics with its sector and size. Set against the current P/E of 25.42x, the 31.14x Fair Ratio suggests McDonald's shares are trading below the level implied by those fundamentals.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your McDonald's Narrative

Earlier sections walked through DCF and P/E in isolation, but Narratives give you a cleaner way to connect everything by tying McDonald's business story to a set of financial forecasts and then to a fair value that you can compare with the current price.

A Narrative is simply your story for the company written in numbers, covering what you think is reasonable for future revenue, earnings, margins and an appropriate P/E, then translating that into a fair value per share.

On Simply Wall St's Community page, Narratives are built into the platform so you can quickly adjust assumptions instead of building spreadsheets, see a calculated fair value, and compare that with the live price to help decide whether you see McDonald's as expensive, fair or cheap for your own purposes.

Narratives are also updated when new information appears, such as earnings, changes to analyst estimates or news on value menus and technology spending. This helps your story and fair value stay aligned with fresh data rather than going stale.

For McDonald's, one Narrative currently anchors on a fair value of about US$239 per share, while another uses analyst style assumptions to reach about US$345. This shows how two investors can look at the same company, plug in different expectations for growth, margins and required return, and end up with very different yet clearly framed views of what the stock is worth to them.

For McDonald's however we will make it really easy for you with previews of two leading McDonald's Narratives:

These are not predictions. They are structured views from different contributors that apply specific assumptions about growth, margins and valuation multiples, then translate those into a fair value per share that you can compare with the current US$306.26 price.

Fair value: US$344.85 per share

Implied discount to this fair value: about 11.2% compared with the recent US$306.26 share price

Revenue growth used in the model: 5.87% a year

- Focuses on expansion in emerging markets, value positioning and menu changes as drivers for brand relevance and international revenue growth.

- Leans on growing digital and technology investment, such as loyalty programs and store automation, to support margins and free cash flow.

- Anchors on analyst consensus assumptions for earnings, margins and P/E, while highlighting risks around input costs, traffic from lower income customers and execution of new technology and store openings.

Fair value: US$238.97 per share

Implied premium to this fair value: about 28.2% compared with the recent US$306.26 share price

Revenue growth used in the model: 4.86% a year

- Highlights a mature business with high returns on invested capital and strong margins, but with more modest projected revenue and EPS growth.

- Uses several valuation approaches, including DCF, earnings growth scenarios, historic P/E, EV/EBITDA, P/S and dividend models, many of which cluster below the current share price.

- Flags that under these assumptions, Monte Carlo simulations often place the current price above the upper range of fair value estimates. This suggests limited room for error in execution or growth.

Taken together, these two Narratives bracket a fair value range from about US$239 to US$345 and show how different assumptions around growth, margins and multiples can lead to very different views on whether McDonald's looks expensive or reasonable at around US$306.

If you want to go beyond the previews and see how the full community and analyst work ties earnings, risks and valuation together, have a look at the wider set of Narratives and context for McDonald's, then decide which story lines up best with your own expectations.To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for McDonald's on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for McDonald's? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.