هل أدى ارتفاع أسهم مجموعة Helix Energy Solutions Group (HLX) إلى محدودية فرص الربح للمستثمرين؟

Helix Energy Solutions Group, Inc. HLX | 0.00 |

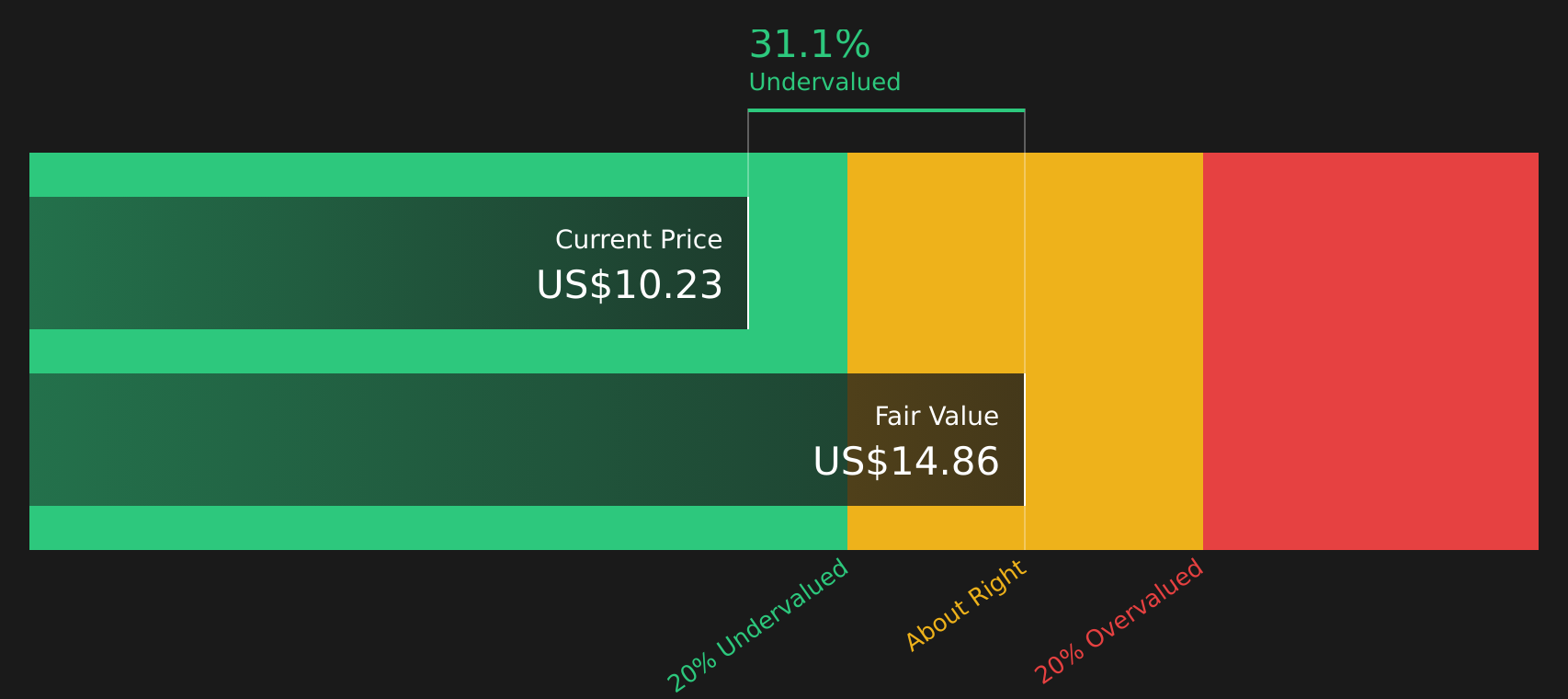

- إن تقييم ما إذا كانت شركة Helix Energy Solutions Group بسعر حوالي 10.14 دولار أمريكي تقدم قيمة جيدة، أو ما إذا كانت المكاسب السهلة قد ولت، يبدأ بفهم كيف يتوافق السعر الحالي مع أساسياتها.

- حقق السهم عائدًا بنسبة 2.9% خلال الأسبوع الماضي، و3.6% خلال الشهر الماضي، و58.4% منذ بداية العام وحتى الآن، و50.9% خلال العام الماضي، مما يثير بطبيعة الحال تساؤلات حول مدى انعكاس القصة بالفعل في سعر السهم.

- ركزت التغطية الإعلامية الأخيرة على مجموعة "هيليكس إنرجي سوليوشنز" كشركة خدمات طاقة بحرية، ترتبط ارتباطًا وثيقًا بمستويات النشاط في عمليات صيانة آبار النفط والغاز تحت سطح البحر والخدمات ذات الصلة. وهذا يفسر سبب اهتمام المستثمرين بتغيرات التوجهات السائدة حول العمل في المجال البحري. توفر هذه الأخبار سياقًا مفيدًا لأداء سعر السهم مؤخرًا، لأنها تُبرز كيف يمكن للتوقعات بشأن مشاريع المستقبل والفوز بالعقود أن تؤثر على ما يرغب المستثمرون في دفعه اليوم.

- يمنح موقع Simply Wall St حاليًا شركة Helix Energy Solutions Group تقييمًا قدره 2 من 6 ، استنادًا إلى مدى تكرار ظهور السهم بأقل من قيمته الحقيقية في مختلف عمليات التقييم. سيتناول الجزء المتبقي من هذه المقالة أساليب التقييم هذه، ويختتم بنظرة أشمل على ما قد يكون السوق قد سعّره بالفعل.

حصلت مجموعة Helix Energy Solutions على تقييم 2/6 فقط في عمليات التحقق من التقييم. اطلع على المؤشرات السلبية الأخرى التي رصدناها في تحليل التقييم الكامل .

النهج الأول: تحليل التدفقات النقدية المخصومة (DCF) لمجموعة حلول الطاقة هيليكس

يُقدّر نموذج التدفقات النقدية المخصومة (DCF) القيمة المحتملة للسهم من خلال توقع التدفقات النقدية المستقبلية للشركة وخصمها إلى قيمتها الحالية. ويركز هذا النموذج على النقد الذي قد يكون متاحًا للمساهمين في نهاية المطاف، بدلاً من الأرباح المعلنة.

بالنسبة لمجموعة Helix Energy Solutions، يُستخدم نموذجٌ يعتمد على مرحلتين لتحويل التدفق النقدي الحر إلى حقوق الملكية. ويبلغ التدفق النقدي الحر للشركة خلال الاثني عشر شهرًا الماضية حوالي 164 مليون دولار. ويُقدّم المحللون توقعاتٍ صريحةً للتدفق النقدي الحر للسنوات القليلة القادمة، ثمّ تُقدّم Simply Wall St استقراءً أبعد من ذلك، مع توقعاتٍ بتدفق نقدي حر يبلغ 124 مليون دولار في عام 2030، وسلسلةٍ من التقديرات حتى عام 2035، جميعها بالدولار الأمريكي.

عند خصم التدفقات النقدية المتوقعة إلى قيمتها الحالية باستخدام هذا النموذج، تُقدّر القيمة الجوهرية للسهم بحوالي 14.85 دولارًا أمريكيًا. وبالمقارنة مع سعر السهم الحالي البالغ حوالي 10.14 دولارًا أمريكيًا، يُشير هذا إلى أن السهم يُتداول بخصم يُقدّر بنحو 31.7%، مما يُشير إلى فجوة تقييم جذابة محتملة إذا تحققت افتراضات التدفقات النقدية.

النتيجة: مُقَيَّم بأقل من قيمته الحقيقية

تشير تحليلاتنا للتدفقات النقدية المخصومة (DCF) إلى أن أسهم مجموعة Helix Energy Solutions Group مقومة بأقل من قيمتها الحقيقية بنسبة 31.7%. تابع هذا السهم في قائمة مراقبتك أو محفظتك الاستثمارية ، أو اكتشف 46 سهماً آخر عالي الجودة مقوم بأقل من قيمته الحقيقية .

النهج الثاني: مقارنة سعر سهم مجموعة هيليكس لحلول الطاقة مع أرباحها

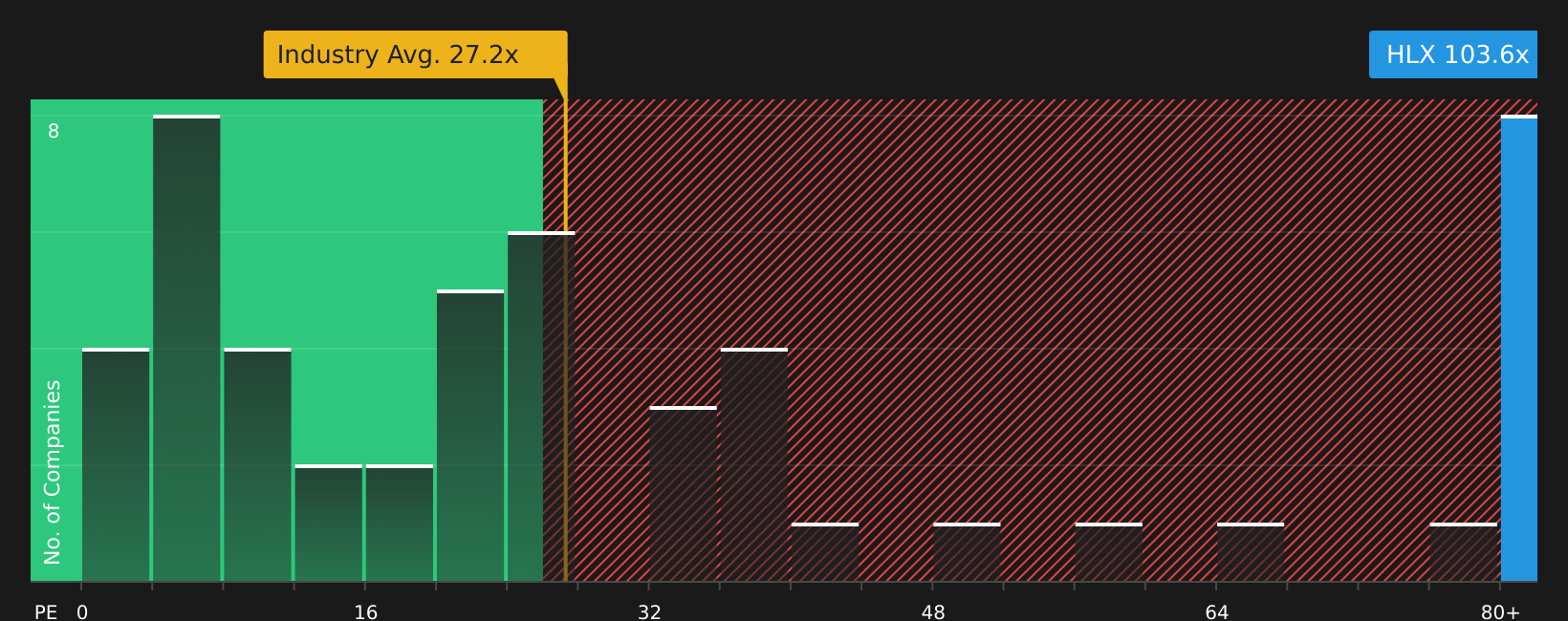

بالنسبة للشركات المربحة، يُعدّ مُضاعف الربحية (P/E) أداةً مفيدةً لتقييم القيمة، لأنه يُقارن سعر السهم الواحد بالأرباح التي تُحققها الشركة حاليًا. فهو يُبيّن فعليًا عدد سنوات الأرباح الحالية التي يرغب السوق في دفع ثمنها.

يعتمد تعريف نسبة السعر إلى الأرباح "الطبيعية" على نظرة المستثمرين إلى إمكانات النمو والمخاطر. فارتفاع معدل النمو المتوقع أو انخفاض المخاطر المتصورة قد يدعم نسبة أعلى، بينما يميل تباطؤ النمو أو ارتفاع المخاطر إلى تبرير نسبة أقل.

تُتداول أسهم شركة Helix Energy Solutions Group حاليًا بنسبة سعر إلى ربحية تبلغ حوالي 104.23 ضعفًا. وهذا أعلى من متوسط قطاع خدمات الطاقة البالغ حوالي 35.68 ضعفًا، وأعلى أيضًا من متوسط الشركات المنافسة البالغ حوالي 76.55 ضعفًا. وتُشير تقديرات Simply Wall St للنسبة العادلة للسهم إلى 19.97 ضعفًا، وهي تقدير خاص بنسبة السعر إلى الربحية بناءً على عوامل مثل نمو الأرباح، وهوامش الربح، والقطاع، والقيمة السوقية، والمخاطر الخاصة بالشركة.

يمكن تخصيص هذه النسبة العادلة بشكل أدق من مجرد المقارنة مع الشركات المنافسة أو مع القطاع ككل، لأنها تأخذ في الحسبان بشكل واضح أساسيات الشركة ومستوى المخاطر. وبالمقارنة مع نسبة السعر إلى الأرباح الحالية البالغة 104.23 ضعفًا، تشير النسبة العادلة البالغة 19.97 ضعفًا إلى أن سعر السهم يتداول أعلى بكثير من هذا المستوى العادل الضمني.

النتيجة: مبالغ في تقييمها

نسبة السعر إلى الأرباح لا تعكس الصورة كاملة، ولكن ماذا لو كانت الفرصة الحقيقية تكمن في مكان آخر؟ ابدأ بالاستثمار في الشركات العريقة، لا في المديرين التنفيذيين. اكتشف أفضل 20 شركة يقودها مؤسسوها .

حسّن عملية اتخاذ قراراتك: اختر سرد مجموعة حلول الطاقة من هيليكس

سبق أن ذكرنا وجود طريقة أفضل لفهم التقييم. هنا، نقدم لكم "السرديات" كقصة بسيطة تُروى عن مجموعة "هيليكس إنرجي سوليوشنز"، حيث تحوّلون رؤيتكم لإيراداتها وأرباحها وهوامشها المستقبلية إلى توقعات مالية مرتبطة بالقيمة العادلة. يمكنكم بعد ذلك مقارنة هذه التوقعات بسعر السهم الحالي لتحديد ما إذا كان السهم جذابًا أم مبالغًا في سعره، كل ذلك من خلال أداة سهلة الاستخدام على صفحة مجتمع "سيمبلي وول ستريت" تُحدّث تلقائيًا عند ورود أخبار أو تقارير أرباح جديدة. تستطيع هذه الأداة استيعاب وجهات نظر مختلفة تمامًا، كأن يُحدد أحد المستثمرين القيمة العادلة بناءً على سيناريو أكثر تفاؤلًا بقيمة 14 دولارًا أمريكيًا، بينما يميل آخر إلى وجهة نظر أكثر حذرًا بقيمة 8 دولارات أمريكية، وذلك بحسب الافتراضات التي تبدو أكثر واقعية بالنسبة لكم.

أما بالنسبة لمجموعة Helix Energy Solutions Group، فسنجعل الأمر سهلاً للغاية بالنسبة لكم من خلال معاينات لاثنين من أبرز روايات مجموعة Helix Energy Solutions Group:

لنبدأ بالحالة المتفائلة، والتي تميل أكثر إلى الأهداف الأعلى للمحللين وتفترض أن السوق لا يزال يقلل من تقدير إمكانات التدفق النقدي لشركة Helix ووضوح العقود.

القيمة العادلة في هذه الرواية: 14.00 دولارًا أمريكيًا للسهم الواحد.

القيمة المنخفضة الضمنية مقارنة بسعر السهم الأخير البالغ 10.14 دولارًا أمريكيًا: حوالي 27.6٪ أقل من مرجع القيمة العادلة.

افتراض نمو الإيرادات: 3.50% سنوياً.

- تعتبر العقود متعددة السنوات وأعمال إيقاف التشغيل وتوجيهات عام 2026 بمثابة دعم لتدفق نقدي حر أكثر موثوقية وقاعدة أرباح طويلة الأجل أعلى.

- تشهد أعمال الروبوتات والطاقة المتجددة، بما في ذلك أعمال الحفر ونشاط طاقة الرياح البحرية، زيادة مطردة في حصة الإيرادات القادمة من الأعمال المتكررة ذات الهامش الربحي الأعلى المحتمل.

- يقبل المخاطر الحقيقية المتعلقة بالطلب على الوقود الأحفوري، واللوائح التنظيمية، وتركيز العملاء، وكثافة رأس المال، وتكاليف العمالة، ولكنه يتعامل مع هذه المخاطر على أنها قابلة للإدارة في إطار توقعات إيجابية للتدفق النقدي على المدى الطويل.

والآن قارن ذلك بموقف أكثر حذرًا، والذي يتخذ وجهة النظر القائلة بأن مجموعة Helix Energy Solutions Group أقرب إلى السعر العادل أو حتى متقدمة على نفسها بناءً على التوقعات الحالية.

القيمة العادلة في هذا السياق: 9.75 دولار أمريكي للسهم الواحد.

المبالغة الضمنية في التقييم مقابل سعر السهم الأخير البالغ 10.14 دولارًا أمريكيًا: حوالي 4.0% أعلى من نقطة القيمة العادلة المرجعية.

افتراض نمو الإيرادات: 3.06% سنوياً.

- يعتبر السعر المستهدف المتفق عليه والقيمة العادلة البالغة 9.75 دولارًا أمريكيًا بمثابة أرضية وسطى معقولة، مع مجال محدود للارتفاع إذا لم ترقَ منح العقود أو أعمال إيقاف التشغيل أو استخدام الروبوتات إلى مستوى التوقعات.

- يؤكد على مخاطر التنفيذ والتوقيت، بما في ذلك تأجيل المشاريع، والتعرض لأسواق السوق الفورية، وارتفاع تكاليف التشغيل، وتأثير دورات الصيانة والأحواض الجافة على التدفق النقدي الحر.

- يسلط الضوء على أنه حتى مع نمو الإيرادات المتواضع وارتفاع هوامش الربح، فإن عوائد المساهمين تعتمد بشكل كبير على مدى اتساق شركة Helix في تحويل تراكم أعمالها إلى أرباح، ومدى انضباط الإنفاق الرأسمالي وعمليات إعادة شراء الأسهم في المستقبل.

هل تعتقد أن هناك المزيد من التفاصيل حول مجموعة Helix Energy Solutions؟ تفضل بزيارة مجتمعنا للاطلاع على آراء الآخرين!

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.