Hasbro (HAS) Valuation Check As Rhode Island Responds To Mr. Potato Head Plate Dispute

Hasbro, Inc. HAS | 90.16 | +0.87% |

Rhode Island lawmakers are moving to halt new Mr. Potato Head license plates in response to Hasbro (HAS) shifting its headquarters to Boston, a symbolic reaction that has drawn fresh attention to the stock.

The headlines around Rhode Island’s response to Hasbro’s move to Boston come as the shares trade at US$86.20, with a 90 day share price return of 15.26% and a one year total shareholder return of 56.33%. This suggests recent momentum has been building after a quieter start to the year.

If corporate moves like Hasbro’s have you rethinking where growth might come from next, it could be worth scanning fast growing stocks with high insider ownership as a way to spot other ideas on your radar.

With Hasbro trading at US$86.20, sitting at a reported 41% discount to one intrinsic value estimate and roughly 8% below analyst targets, investors may ask whether there is still upside potential or if the market is already pricing in future growth.

Most Popular Narrative: 6.8% Undervalued

Compared to Hasbro’s last close at US$86.20, the most followed narrative pegs fair value a little higher at about US$92.46, framing the stock as modestly undervalued on its cash flow potential.

Heightened demand for nostalgia and collectibles among Millennials/Gen Z and the durability of key franchises (Magic: The Gathering, D&D, Transformers, etc.) are leading to high engagement, strong long-tail sales, and higher average transaction values, supporting ongoing margin expansion and predictable future cash flows.

Curious what kind of revenue path and margin shift would justify that fair value gap, and which future profit multiple underpins it? The full narrative lays out a detailed earnings roadmap, including how higher return on equity, expanding margins and modest revenue growth are combined to support that cash flow view.

Result: Fair Value of $92.46 (UNDERVALUED)

However, this depends on key risks, including any slowdown in core franchises like Magic: The Gathering or setbacks in the digital pivot that could unsettle earnings expectations.

Another View: Multiples Paint A Richer Picture

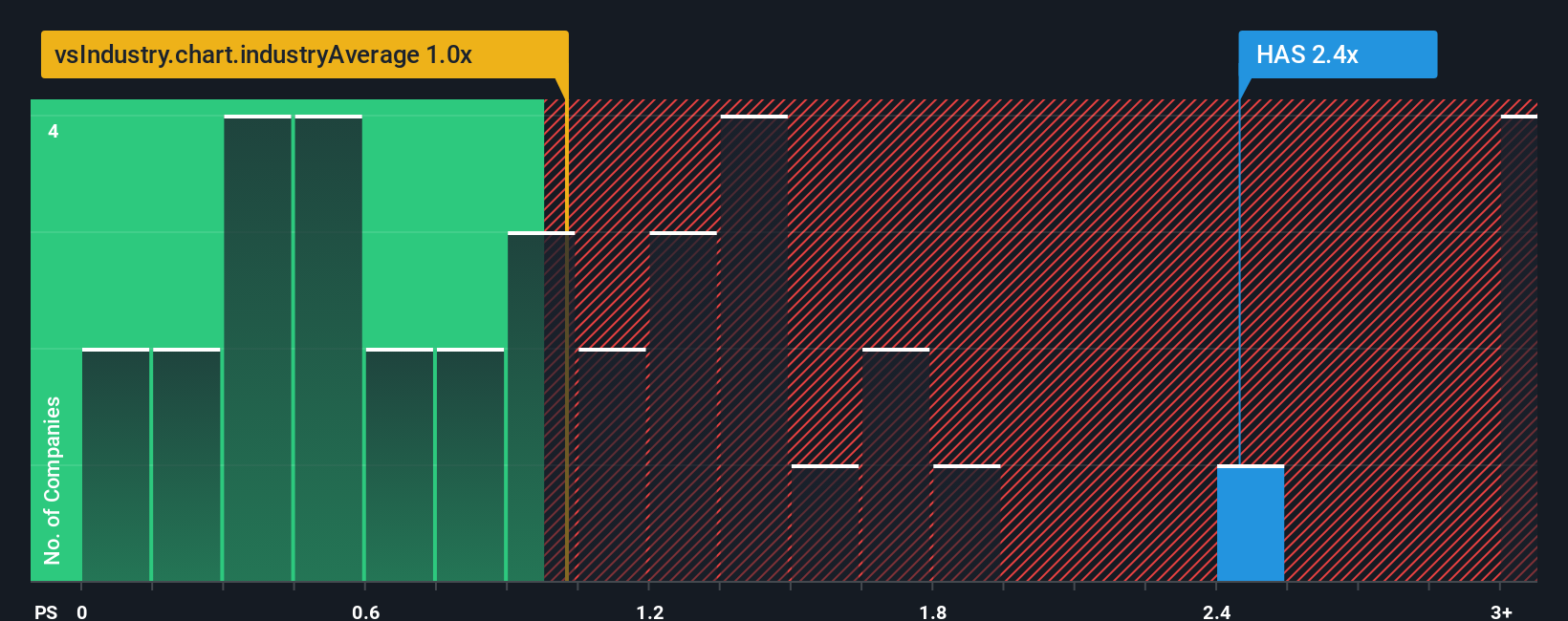

While the SWS DCF model points to Hasbro trading at a 41.3% discount to its fair value, the P/S ratio of 2.8x tells a different story. That level sits well above the US Leisure industry at 1x, the peer average at 1.3x, and even the estimated fair ratio of 2.2x, which hints at valuation risk if sentiment cools. Which lens do you trust more for your own thesis: cash flows or sales based markers?

Build Your Own Hasbro Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a complete Hasbro view yourself in just a few minutes: Do it your way.

A great starting point for your Hasbro research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Hasbro has sharpened your interest, do not stop here. Widen your watchlist with focused stock sets that match different return and risk preferences.

- Target potential value by scanning these 873 undervalued stocks based on cash flows that flag companies trading below what their cash flows might justify.

- Ride powerful tech themes by reviewing these 24 AI penny stocks that bring artificial intelligence into real world products and services.

- Boost your income focus with these 12 dividend stocks with yields > 3% that highlight businesses sharing more than 3% of their value each year in cash payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.